One of my favorite pairings is looking for passive income What you want in the stock market is to find companies that are safe, well-run, and whose dividend yields are close to the highest of the past 10 years. Although this combination is not very common, chocolatier hershey company (New York Stock Exchange: HSY) and quick service food franchisors MTY Food Group (OTC: MTYF.F) We currently meet these requirements.

With Hershey and MTY down 12% and 20% from their 52-week highs and 33% and 39% off their all-time highs, investors would be wise to consider these two great dividend stocks at a discount. Dew.

That's why Hershey and MTY's 2.9% and 2.3% dividend yields, near 10-year highs, make acquiring Hershey and MTY an attractive investment proposition.

Hershey: Chocolate and Snack Safety and Stability

Perhaps the most compelling reason to consider acquiring The Hershey Company is its stability. Hershey operates in the recession-proof industry of chocolate and sweet and salty snacks, and is definitely stable, as evidenced by its 5-year beta of 0.37.

Beta measures a stock's volatility in comparison to the overall market, and a beta of less than 1 means the stock is less likely to fall during a bear market. I consider stocks with low betas like Hershey to be “foundation” type holdings that can be used as the basis of a portfolio. That's why. One of my daughter's nine core portfolio positions.

That said, the company's current drawdown from all-time highs is 33%, the third-largest in the past 30 years, but down from the 50% and 40% during the 2008 and 2000 crashes. Only less than the decline.

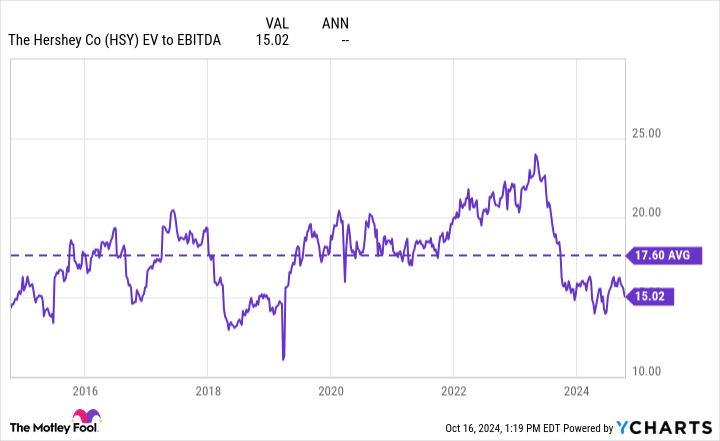

So does this decline indicate that Hershey is damaged goods when the overall market is still rising?

There aren't that many. First, before this decline, the company's enterprise value (EV) to earnings before interest, taxes, depreciation, and amortization (EBITDA) ratio was at an all-time high of 24. For reference, Hershey's current EV/EBITDA ratio is: The historical average as a listed stock is 15, which shows how high the company's valuation has been.

Additionally, the company faces a series of short-term headwinds, ranging from the introduction of new enterprise resource planning systems, cocoa prices that briefly quadrupled in less than two years, and cost-conscious consumers. Masu. But ultimately, when investors look back on these challenges 10 years from now, I have confidence that they will prove to be temporary and that Hershey's market-leading brand will hold up. I'm doing it.

The company, backed by three of America's most famous chocolate brands (Hershey, Kit Kat, and Reese's), remains a niche market leader, according to Statista. In addition to being the top banana in the chocolate world, Hershey's recent acquisitions of SkinnyPop Popcorn and Dot's Homestyle Pretzels have been an immediate success, with the new unit increasing sales by 13% annually since 2019. and increased by 65%.

And when it comes to dividends, Hershey has increased its dividend twice in three quarters, a massive 32% increase despite its challenges since the beginning of 2023. Even after this significant increase, dividends still use only 55% of Hershey's net income, leaving plenty of room to continue raising the dividend, which is already at a 10-year high.

Don't get me wrong, Hershey's isn't going to be a multibagger anytime soon. But its 2.9% yield, leadership position, recent acquisition success, and solid performance in the face of numerous short-term issues make it a decades-long buy. It's a wonderful bedrock.

Diversification of MTY Food Group regardless of season or variety

While Hershey's safety derives from its focus on the chewy chocolate and snack niche market, MTY Food Group's stability is due to its broad diversification. MTY's portfolio of approximately 90 quick service food brands is incredibly diversified throughout all seasons and across nearly every cuisine imaginable.

Significantly oversimplifying a balanced portfolio, MTY's array of frozen treats and smoothie brands lead the way in the summer, while brands like Wetzel's Pretzels and Papa Murphy's do more heavy lifting in the colder months. I do a lot.

In addition to this diversification, MTY's focus on being a franchisor, with all but about 200 of its approximately 7,000 stores operated by franchisees, makes MTY unique. There is no safe investment proposition. Offloading the majority of risk and capital requirements to franchisees, MTY is an asset-light operator with stable free cash flow (FCF) margins.

Even in the midst of the pandemic, MTY maintained a 20% FCF margin, which is actually higher than the current 15% mark. MTY's FCF growth over the past decade has been an art, although declining consumer confidence continues to put some pressure on the company's FCF margins.

With 27 acquisitions in the last 10 years alone and a value of over $1.7 billion, MTY is redeploying its growing total FCF into new businesses that do even more: create a beautiful flywheel effect. He has proven himself to be skilled.

However, MTY does not spend all of its FCF on mergers and acquisitions. The company's dividend yield is currently 2.3%, the highest level in the past 10 years, excluding the 2020 crash. What makes this yield even more attractive is that it uses only 14% of MTY's FCF. This means the company could triple its yield to 7% and still have cash left over.

However, the stock trades at just 10x EV/FCF, and management is leaning toward buying back its own shares at a deep discount to the market. Management has shown an appetite for share buybacks after sales over the past five years, and with MTY currently down 39% from its all-time high, it will continue to do so.

Since 2019, MTY has reduced its share count by 1.2% each year, which is a welcome addition to the cash returned to shareholders as dividends.

Overall, MTY's stable FCF generation and continuous acquisition method combine to create a powerful compounding machine that will continue to generate dividend growth for investors for decades to come.

Don't miss out on this potentially lucrative second chance

Have you ever felt like you missed out on buying the most successful stocks? Then you'll want to hear this.

In rare cases, our team of expert analysts “Double Down” stock Recommendations for companies that are likely to take off. If you're already worried that you're missing out on an investment opportunity, now is the best time to buy before it's too late. And the numbers speak for themselves.

-

Amazon: If you invested $1,000 when it doubled in 2010; you have $21,285!*

-

apple: If you invested $1,000 when it doubled in 2008; That's $44,456!*

-

Netflix: If you invested $1,000 when it doubled in 2004; you have $411,959!*

We currently have “double down” alerts on three great companies, and we may not see an opportunity like this again anytime soon.

*Stock Advisor will return as of October 14, 2024

Josh Cohn-Lindquist Positions available at Hershey and MTY Food Group. The Motley Fool has a position in and recommends Hershey and MTY Food Group. The Motley Fool has Disclosure policy.

Two high-dividend stocks are down 33% and 39%, with dividend yields near 10-year highs, but you should buy them now Originally published by The Motley Fool