Torsten Asmus

A booming market is approaching a downturn.

It’s easy to get caught up in the frenzy when the market is at all-time highs and rising daily. But with patience, you may get higher profits later. There will be a backlash.of The only question is when.

Why is the stock market growing so fast?

Many stocks rose parabolically in 2024, surpassing their 2021 highs and pushing valuation metrics out of the norm. There are many reasons, but here are two.

First, the economy is in better shape than many thought. The promised recession has not yet materialized. I had thought that personal consumption would soften soon, but there are almost no signs of that happening. But I never bought into the theory that there would be up to six rate cuts this year.

It is fashionable to criticize The Fed and Jerome Powell. However, it’s set up nicely. The economy is growing even when interest rates are above 5%. If the economy slows, each percentage point is like the Fed’s arrow. Don’t expect to give up easily.

People are also returning to work, easing labor shortages and inflation. I recently spoke with a “small” ($70 million in revenue) business associate who operates in an industry that is important to the economy. He had 140 applicants for a recent job opening at this company. Coming out of the pandemic, there will usually only be one he or two hes (sometimes zero hes).

Could a lack of interest rate cuts trigger a healthy recession?

The second is artificial intelligence (AI). Please do not make any mistakes. Technology is transformative. But it’s pushing the boundaries of many stock valuations, and there’s a lot of hype going on. Retreating may be natural.

It’s smart to make a “market down” wish list. Here are some of mine.

cloud strike

Companies can reduce many expenses during periods of economic uncertainty, such as marketing, research costs, and personnel costs. But cybersecurity is a critical need and it would be foolish to cut back on it. This is the argument I used to buy CrowdStrike (CRWD) and Palo Alto (PANW) during the 2022 distress and 2023 economic recovery. Both stocks outperformed.

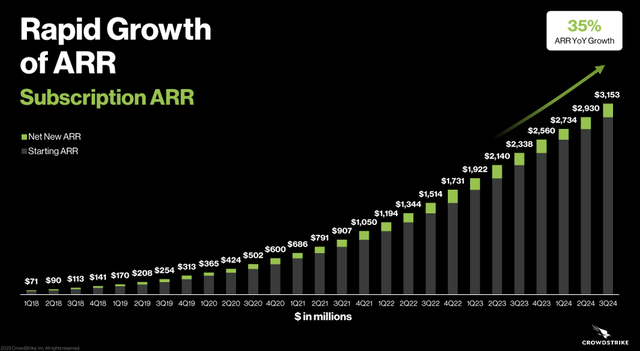

CrowdStrike achieved annual recurring revenue (ARR) of $3.2 billion last quarter in the comprehensive cloud-based modular security space, as shown below.

Source; Crowdstrike

The company has improved operating leverage and free cash flow is rapidly growing to reach $655 million by the third quarter of fiscal 2024.

I’ve been on the CrowdStrike bandwagon for a long time, including “doubling down” to $130 per share in this article. Since then, the stock has soared 150% and trades at a massive 28 times sales, but it was too rich for me. Watch for a definite rebound.

arm holdings

There’s a reason Nvidia (NVDA), one of the smartest companies on the planet, tried to acquire Arm Holdings (ARM) in 2020. Arm is deeply embedded in the semiconductor market. 99% of smartphones include this design, so you probably use it on a daily basis.

There is an important difference here. Arm does not produce chips. Arm creates the architecture and licenses it to top chip makers. You then receive a royalty on each chip shipped. To date, 280 billion units have been shipped. You may have heard about customers like Apple (AAPL), Alphabet (GOOG)(GOOGL), Amazon (AMZN), Microsoft (MSFT), and Taiwan Semiconductor Manufacturing (TSM). The market is booming.

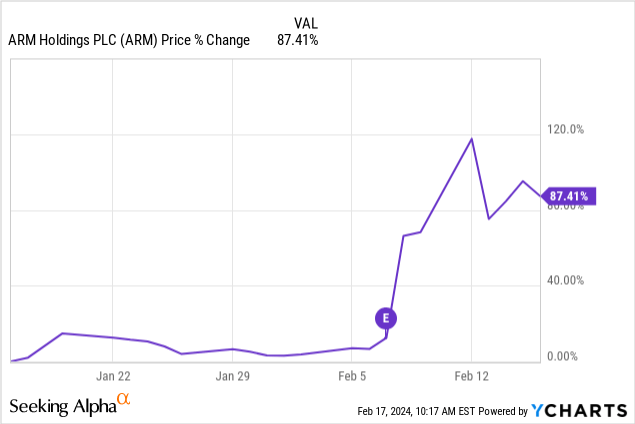

Arm’s fiscal 2024 third-quarter results showed a 14% increase in revenue to $824 million, but that wasn’t the only thing driving the stock’s incredible jump.

The company reported increased adoption of its latest architecture, “Arm v9”, generating double the loyalty of previous versions. Arm’s remaining performance obligations increased 38% year over year (YOY) from $1.75 billion to $2.4 billion.

Arm has a great business model. No chips are generated. Free cash flow is abundant due to low capital investment. It reportedly had a 30% margin last quarter.

A $130 billion market cap for a company with $3 billion in 12-month sales is very expensive. As the initial excitement wears off, the stock is likely to largely repeat its recent rally, which could present an opportunity for long-term investors.

Palantir

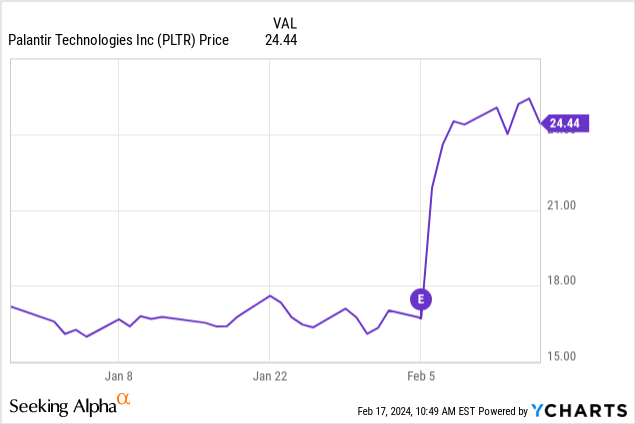

I’ve been making money with Palantir Technologies (PLTR) stock without owning a single stock. When the stock price fell below $8 per share in 2022, I bought a long-term $10 call option that has since closed. You can also do this by selling a put option leading up to the latest earnings release and closing it with the move shown below.

If Palantir can regain some of this jump, it looks like it could be a good play in the long run.

Palantir has long been entrenched in the defense industry and is looking to expand its market by growing its commercial business, and it’s paying off. U.S. commercial sales increased 70% sequentially to $131 million, and his number of U.S. commercial customers increased 55% to 221 companies.

Total revenue for the quarter increased 20% to $608 million, marking Palantir’s fourth consecutive GAAP profitable quarter.

The release of Palantir AIP (Artificial Intelligence Platform) comes as many companies are looking to leverage generative AI to improve decision-making and efficiency. Palantir will be a great partner and this will lead to further penetration into the private sector.

Warren Buffett said:

Most people become interested in stocks when other people are interested in stocks. It’s when no one else is interested that you become interested.

Wise advice. There are a lot of great companies doing amazing things right now, but valuation still matters and patience will pay off in the long run.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.