Our drunken sailors and their credit cards.

Wolf Richter on Wolf Street.

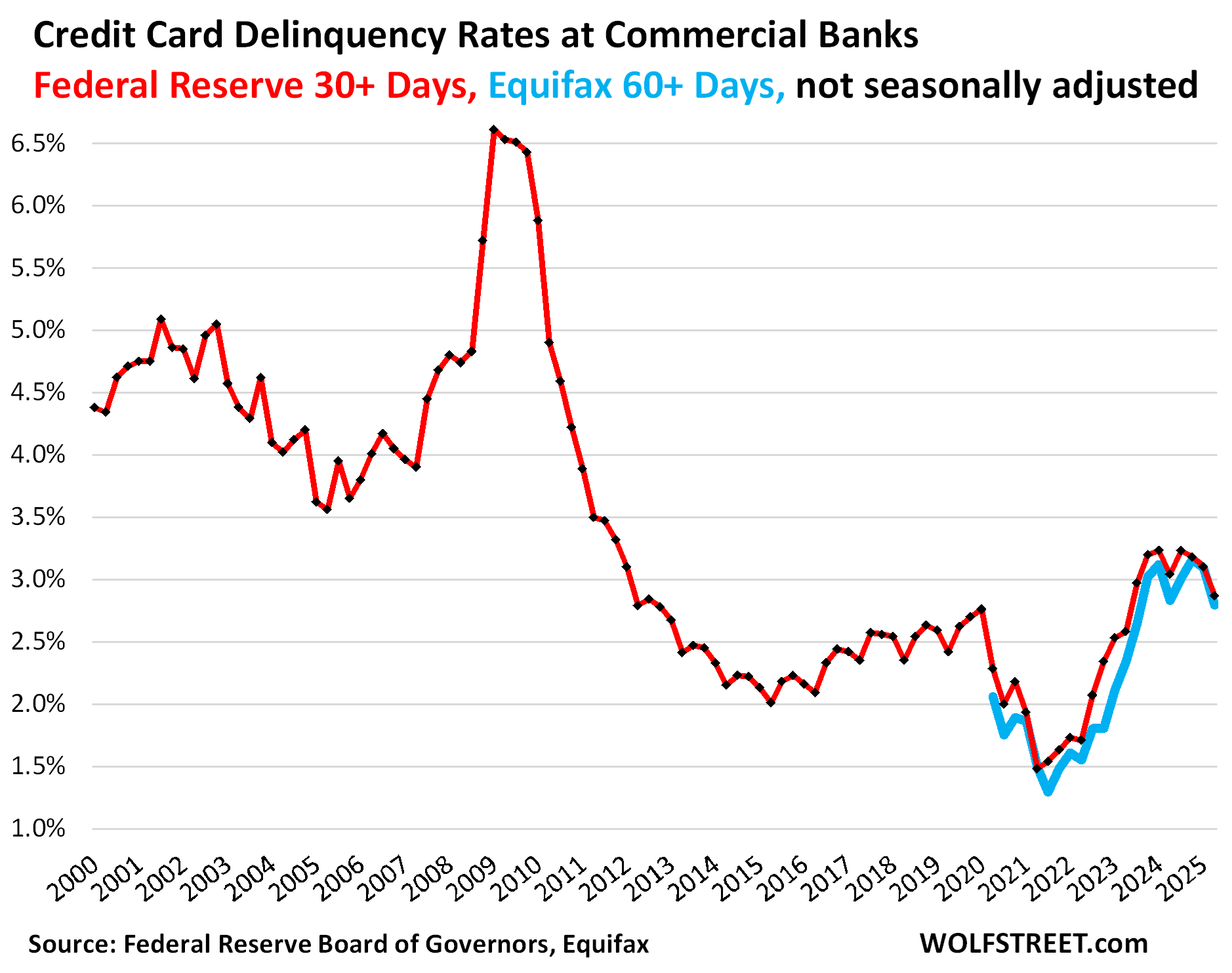

Recently, credit card delinquency rates—referred to by some as “drunken sailors”—have shown some notable improvements.

The delinquency rate for credit cards, defined as payments overdue by 30 days or more, decreased to 2.87% at the end of the second quarter, as reported by the Federal Reserve. This statistic includes credit cards held by those with subprime ratings.

During the period when easy money was flowing, late payments significantly declined for a couple of reasons. First, with fewer opportunities to spend on dining out, traveling, and entertainment, credit card balances went down. Additionally, many took advantage of available funds to settle any outstanding debts. But, once this easy money phase ended, delinquency rates spiked in the second quarter of 2024 before stabilizing.

The severe delinquency rate, which encompasses those overdue by more than 60 days, also saw a drop to 2.79% by the end of the second quarter, marking the lowest level since 2023.

For prime-rated cardholders, the severe delinquency rate decreased to 0.93%, reflecting the lowest position since the third quarter of 2023.

This figure is consistent with historical lows recorded prior to the easy money era that began in July 2016.

It’s worth noting this “frying pan” pattern, which I’ve discussed previously, as it appears consistently in various credit measures since the pandemic altered many financial behaviors.

Credit Card Balance: Expense Scale

Credit card balances, noted as the red line in the chart, increased by $27 billion from the first to the second quarter, climbing to $1.21 trillion, reversing a trend of seasonal declines that typically happen during the first quarter, according to New York’s household debt and credit report.

Looking at it year-over-year, credit card balances rose 6.7% due to both increased consumer spending and rising prices.

These balances essentially reflect spending habits, rather than borrowing capacity. They represent the amount owed before any payments are made. Credit cards now dominate consumer transactions in the U.S., often replacing checks and cash. They are involved in nearly $6 trillion in annual transactions, including expenses covered by reimbursements. Most of these balances are cleared daily or monthly, often avoiding interest charges.

Meanwhile, “other” consumer loans, which come from personal loans and buy-now-pay-later plans, have seen a decline, diminishing steadily over the past year despite population growth and rising incomes.

How much is the burden?

In the first quarter to second quarter period, credit card balances and other consumer debt combined rose by $25 billion (1.4%), totaling $1.75 trillion.

Year-over-year, there’s been an increase of $63billion, which is about 3.7%.

The debt-to-income ratio remains a classic indicator of how well borrowers manage their debt. To analyze the combined balances of credit cards and other revolving debts, we consider their relationship to disposable income.

According to the Bureau of Economic Analysis, disposable income encompasses household income from all sources, excluding capital gains, and includes post-tax wages, interest, dividends, rental income, small business earnings, and government payments.

While disposable income increased modestly quarter-over-quarter, it grew faster compared to the same time last year.

- Quarter-over-quarter: Disposable income +1.25%, credit cards and others +1.45%.

- Year-over-year: Disposable income +4.5%, credit cards and others +3.7%.

As a result, the ratio of disposable income to credit card and other debt slightly increased to 7.76% from 7.75% in the previous quarter, though it remains lower than the same period a year ago. During the easy money phase, that ratio dropped to just 6%, but now, with the end of easy money, it has reverted to the lower end of pre-pandemic levels.

Credit limits and available credits will expand to New High

To boost revenue from transaction fees, banks are actively encouraging the opening of new credit card accounts and raising credit limits. Total credit limits have surged to a record $5.23 trillion by the second quarter.

This trend has resulted in total available credit—total credit limit minus negative credit card balances—reaching a historic high of $4.03 trillion.

Following the Great Recession, banks reduced risk by cutting credit limits. More recently, even during the pandemic, lending tightened significantly.

Third-party collections

This quarter, the percentage of consumers facing third-party collections—meaning their delinquent accounts were sold to collections agencies—for credit cards and other debts rose to 4.7%, which is up from a historic low last quarter.

Such entries appear on a consumer’s credit history when lenders report to credit agencies that they have sold a late debt to a collection agency. Data on these collections comes from anonymized sources via partnerships with credit agencies.

And just in case you missed our report on other American debt:

We also cover significant delinquency rates and balances related to subprime and prime auto loans. Subprime lending, which often includes high-risk borrowers, continues to present challenges.

Additionally, we examine mortgages, housing obligations, income relationships, serious delinquencies, and foreclosures for the second quarter of 2025, where both taxpayers and investors are feeling the impact this time around.

Household debt, debt-to-income ratios, serious delinquencies, collections, foreclosures, and bankruptcies are all part of a broader picture that remains complex. For instance, long-standing federal student loans are finally receiving more attention.