The EUR/USD pair is projected to finish the week down by 0.21%, though it has managed to stay above 1.16 for the third consecutive day. There seems to be a significant resistance that is limiting any upward movement, especially since recent U.S. economic data might not keep the Federal Reserve from lowering interest rates.

Positive PMIs bolster the euro, while Moody’s caution on France dampens momentum

U.S. inflation figures haven’t sparked action from Fed supporters, falling short of anticipated lows, yet they remain away from the central bank’s 2% goal. In fact, S&P Global’s early PMIs for manufacturing and services have shown growth this October, hinting at a resilient economy.

On another note, the University of Michigan’s report on consumer sentiment came out amidst the U.S. government shutdown, which has now lasted for over 200 days. It showed that American consumers are feeling a bit more pessimistic about the future and expect prices to keep climbing.

The U.S. dollar has recently lost some of its gains, particularly after the Trump administration initiated a trade investigation into China’s adherence to the limited trade agreement established during his first term.

Across the Atlantic, the HCOB Flash Purchasing Managers’ Index (PMI) inched up from 49.8 to 50 for manufacturing and from 51.3 to 52.6 for services in October. Both results surpassed expectations, indicating a surge in business activity driven by increased demand.

At this moment, Moody’s changed France’s outlook to negative while confirming its AA3 rating. The rating agency expressed concerns that “political instability in France may hinder its ability to tackle pressing policy issues like an expanding budget deficit and growing debt.”

Market Trends: EUR/USD Remains Stable Despite Strong U.S. PMI Data

- The U.S. Dollar Index (DXY), which measures the dollar’s performance against a selection of currencies, rose by 0.03% to 98.94, capping gains for the EUR/USD pairing.

- For September, the U.S. Consumer Price Index (CPI) saw a 3.0% increase year-over-year, slightly below the expected 3.1% and just above August’s 2.9%. When excluding food and energy, the core CPI also edged up 3.0% year-on-year, though it dipped by one-tenth from the previous month.

- Business activity in the U.S. picked up pace in October, reaching the second-fastest rate this year, according to S&P Global’s PMI data. The report also noted robust new business growth in 2025, emphasizing ongoing private sector resilience. The S&P Global Manufacturing PMI increased to 52.2 in October from 52.0 in September, indicating consistent expansion. The service sector’s PMI rose from 54.2 to 55.2, marking the strongest level in three months and showcasing solid business activity.

- The University of Michigan’s October Consumer Confidence Index was revised down to 53.6 from an initial estimate of 55.0, falling short of the expected 55.1. One-year inflation expectations saw a slight decline to 4.6% from 4.7% in September, while five-year expectations crept up to 3.9% from 3.7%.

- Market anticipations suggest that the U.S. central bank might lower interest rates by 25 basis points (bps) to a range between 3.75% and 4%, with traders already factoring in another 0.25% reduction at the December meeting.

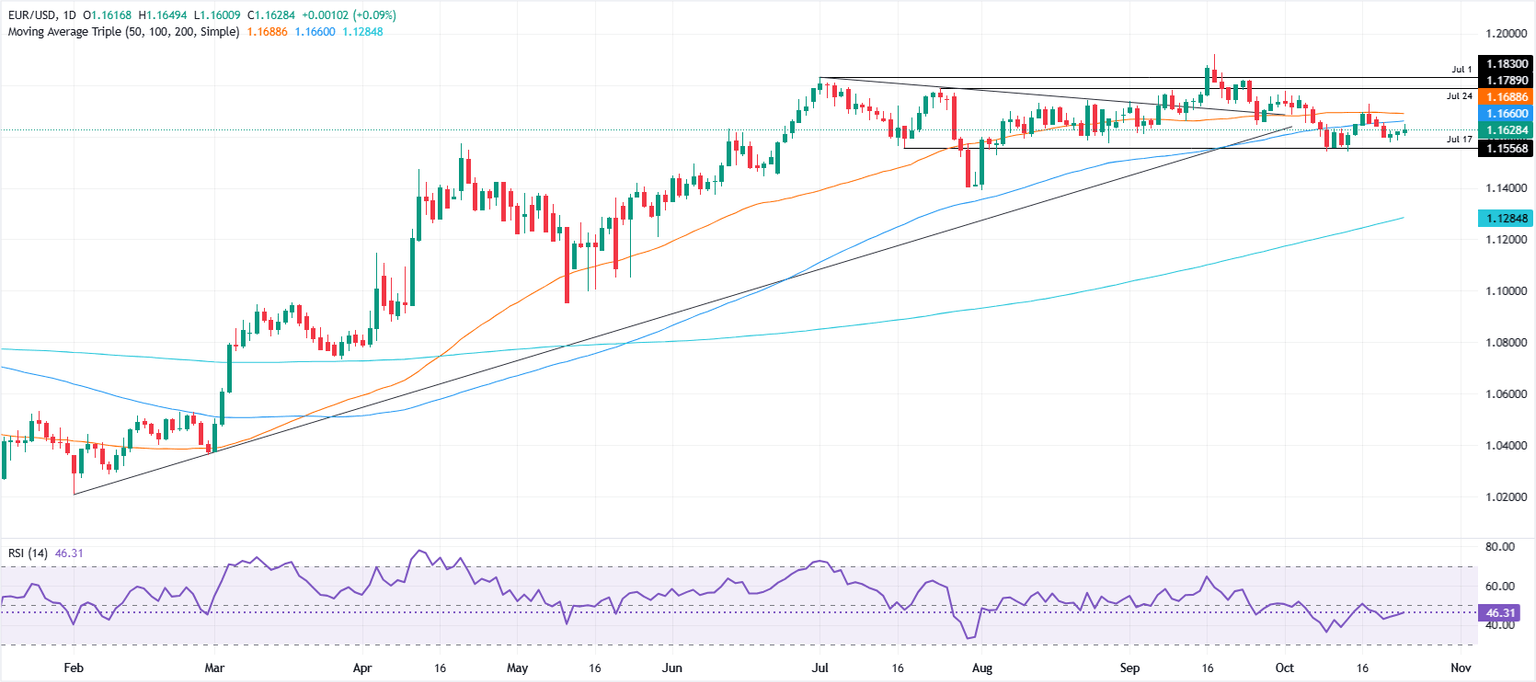

Technical Outlook: EUR/USD Holds Steady with a Slight Bullish Bias

The technical picture for EUR/USD has seen a modest improvement but still leans neutral, as it hovers below key resistance levels marked by the 20-day and 100-day simple moving averages (SMAs) at 1.1653 and 1.1658. The Relative Strength Index (RSI) has dipped below the neutral 50, signaling increasing bearish momentum.

In terms of immediate support, levels are noted at 1.1600, 1.1550, and 1.1500. If it breaks through this range, it could mark a low point reminiscent of August 1, which was around 1.1391. On the upside, resistance aligns with the 20-day and 100-day SMAs, but a strong move past 1.1700 could set sights on 1.1800 and the July 1 high of 1.1830.