Nvidia, Taiwan Semiconductor, and Amazon Set for Growth

Nvidia anticipates significant growth by 2026, with momentum building as we approach the close of 2025. Several stocks are positioned to take off, thanks to favorable conditions ahead.

I see three stocks likely to skyrocket soon: Nvidia (NASDAQ:NVDA), Taiwan Semiconductor (NYSE:TSM), and Amazon (NASDAQ:AMZN). I think these companies present great buying opportunities right now, and it might be wise for investors to consider acquiring them before we hit 2026.

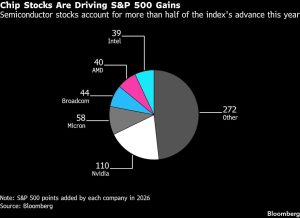

Nvidia’s stock has been largely driven by the artificial intelligence race, gaining traction since 2023. Their GPUs are vital for the current AI infrastructure, and it looks like this trend will continue. Remarkably, Nvidia has reported $500 billion in orders for pivotal data center GPUs expected by the end of 2026. Given that Nvidia generated $165 billion in revenue over the last year, the potential for growth is substantial if they meet these production goals.

This scenario encourages considerable buying of Nvidia stock ahead of the year’s end, making it an appealing stock to consider, even after its recent surge.

Next is Taiwan Semiconductor Corporation (TSMC), which stands to gain as Nvidia and other companies rely on TSMC to fabricate chips for high-performance computing. TSMC is recognized as the top chip foundry globally, and its capabilities are considered among the best. With soaring demand for Nvidia’s chips, TSMC’s sales are likely to climb. Plus, TSMC is rolling out new 2nm chip technology that promises significant energy efficiency—around 25% to 30% less power consumption compared to older 3nm nodes. This improvement could encourage more purchases of high-end chips from Nvidia clients.

There’s a sense that TSMC is well-positioned for the eventual leaders in the AI arms race, and as investment in AI technology continues to swell into late 2025 and beyond, TSMC will likely see benefits.

Finally, let’s consider Amazon. The company has had a rough patch this year and, until their recent earnings report, had been the least performing of the Magnificent Seven stocks. However, there’s a bit of a reversal happening. I’m optimistic that investors will recognize Amazon as a solid bargain soon.

Amazon’s growth narrative has largely revolved around improving margins from high-margin sectors like advertising and its cloud service, Amazon Web Services (AWS). While margins haven’t seen much improvement lately, it’s likely due to heavy reinvestments into AI computing capabilities. Once this focus shifts, Amazon might experience a significant cash flow influx, which could lead to stock buybacks and increased shareholder returns.

Another detail worth remembering is that AWS holds the largest share of the cloud market. While competitors have shown rapid growth, AWS continues to lead, especially as its clients deploy AI workloads through its platform. Amazingly, despite the challenges, it’s still a formidable contender. There are predictions that it could have a fantastic finish in 2025 and regain ground against its peers in 2026.

Before diving into Nvidia stock, it’s essential to consider all angles.