This week’s trade highlights for November include a few notable points.

- Long USD/JPY currency pair, which decreased by 0.38% over the week.

- Long positions on the S&P 500 index after closing above 6,920, although this wasn’t a planned move.

- Long on the Nasdaq 100 Index after closing above 26,288, which also wasn’t set up beforehand.

- Long KOSPI composite with a quarter-sized position, despite the index falling 4.11% last week.

- Long Nikkei 225 index with a 1/4 size position, which dropped by 3.86% for the week.

Overall, these trades resulted in a loss of 2.37%, averaging a loss of 0.47% per asset.

Here’s a summary of key data from last week:

- ADP Nonfarm Employment Change – Slightly better than expected, indicating the U.S. economy added 42,000 jobs last month, compared to the projected 32,000.

- US ISM Services PMI – Better than expected, indicating a stronger U.S. economy.

- US ISM Manufacturing PMI – Worse than anticipated, suggesting the manufacturing sector is struggling.

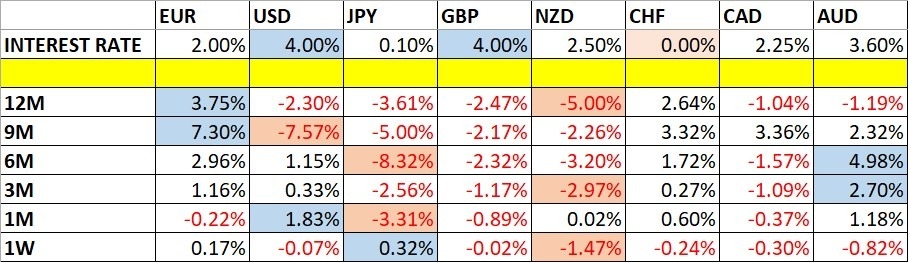

- Bank of England rates and monetary policy report – The Bank decided to keep interest rates steady at 4%, although the vote was surprisingly close, raising concerns about potential cuts. This initially caused the pound to drop, but it recovered by Friday amid a rebound in risk assets.

- RBA Interest Rates – No surprises here; rates remain at 3.60%.

- Swiss CPI – This indicated deflation rather than inflation, at 0.3% month-on-month, which boosted the Swiss franc.

- Canada’s unemployment rate – At 6.9%, which is better than expected but still relatively high, had minimal impact on the Canadian dollar.

- New Zealand unemployment rate – Stood at 5.3%, as anticipated.

Some U.S. data was supposed to be released last week but got postponed due to the ongoing federal government shutdown.

Last week, the biggest data releases included strong U.S. jobs numbers that helped the markets recover somewhat. Meanwhile, the Bank of England moved closer to the likelihood of cutting interest rates. Despite a trading recovery in New York on Friday, the stock market saw its steepest decline in months, with most major markets down, raising concerns about excessive price rises and high valuations, particularly in tech.

Interestingly, the new bullish trend for the U.S. dollar seems to be losing steam. The CME FedWatch Tool hints at an increased 70% chance for a 0.25% rate cut in December, up from 63% the week before, although the dollar gained some ground on Friday.

In legal news, there’s about a 60% probability that the U.S. Supreme Court may rule against President Trump regarding his constitutional authority for tariffs. If that happens, he could still use other tools, but they would be less effective.

The government shutdown continues but seems to have limited impact beyond delaying U.S. economic data updates.

This Tuesday marks a public holiday in the U.S., Canada, and France.

Looking ahead, much hinges on whether the government shutdown resolves next week, especially with crucial inflation data set for release. If the shutdown continues into Thursday, that data may not come out as scheduled. PPI data for the U.S. is due on Friday, with a similar situation.

This week’s important data points are:

- US CPI (inflation)

- US PPI

- US retail sales

- UK GDP

- U.S. unemployment insurance claims

- Australia unemployment rate

- UK unemployment insurance claims

Again, this Tuesday is a public holiday in the U.S., Canada, and France.

The ongoing shutdown may lead to indefinite delays in U.S. data.

For November 2025, we had forecasted that the USD/JPY currency pair would rise in value.

So far, the performance looks like this.

I didn’t make a weekly forecast last week.

After a large price movement in the NZD/JPY cross, indications suggest a rise next week, despite the NZ dollar’s ongoing weakness.

Last week, the Japanese yen emerged as the strongest major currency, while the NZD was the weakest. Volatility dropped, with only 22% of major pairs and crosses shifting more than 1%.

Next week’s volatility will depend on the government shutdown’s progress. If resolved, important U.S. data could spark increased market activity.

These predictions can be acted upon in either live or demo Forex accounts.

Despite a significant fall, the U.S. dollar index showed a bearish candlestick last week, about to hit a pin bar. While it’s slightly below a level from 26 weeks ago, it’s above where it was 13 weeks ago, suggesting a long-term downward trend may have ended, potentially setting the stage for a new bullish phase.

The dollar experienced declines as market confidence wavered regarding the Federal Reserve’s stance on interest rates leading up to Wednesday’s meeting. Markets are factoring in a 70% probability of a rate cut in December, an increase from 63% the previous week.

With crucial inflation-related data missing due to the shutdown, the dollar’s fate will likely pivot on upcoming inflation and PPI results once the situation normalizes. Alternatively, other currencies are expected to become more active, potentially leading to a sharper decline for the dollar.

I still lean towards going long on the U.S. dollar rather than shorting it.

Last week, the NZD/USD currency pair saw a significant drop, with the kiwi losing ground despite a slight decline in the USD. The kiwi’s issues stem from a deepening recession and the Reserve Bank of New Zealand facing tough choices amid economic contraction. Further rate cuts seem likely, and if global risk sentiment worsens, New Zealand’s economy could become even more vulnerable.

Although the foundations signal more downside potential, the long-term price trend shows the NZD tends to find substantial support around $0.5500. It’s a notable threshold, yet recent lower highs imply a breakdown could happen.

The price movement last week felt overextended, but it’s logical to anticipate a dip towards the $0.5500 mark, followed by a significant rebound. Should the price settle below this point, it would indicate a dramatic turn for the kiwi.

The USD/JPY pair’s weekly chart illustrated a bearish, indecisive candlestick. We’re in a long-term bullish trend, but the price remains within a consolidating triangle pattern.

New uncertainties regarding both the dollar and yen are surfacing. The dollar seems poised for a new long-term bullish trend, but there are signs of stalling. Conversely, the yen has been weakening, but inflationary pressures could push the Bank of Japan to consider raising rates further.

Most traders should probably wait for a bullish breakout above the upper trend line before entering long positions. A daily close over 154.25 yen would be advisable, or just to be safe, wait for the round number of 155.00 yen.

Despite a significant drop last week, the stock index rebounded on Friday, recovering about half of its losses. There’s speculation that the U.S. market is due for a major correction, although it hasn’t materialized yet. The key level on the price chart signifies where financial institutions usually start reducing or closing long positions.

The market remains bullish, trending upwards. So, traders with open positions might want to hold until it falls below 6,620 or even 6,500. However, entering new trades before a new high above 6,920 seems unwise.

Bulls should also be wary of the significant 7,000 mark, which could drive profit-taking if reached.

Much of what applies to the S&P 500 index also pertains to the Nasdaq 100 index, though the Nasdaq’s prices traded below the level where institutions usually back off before larger gains. It’s likely that institutions saw this as a buying chance, making a convincing rally a positive sign.

However, tech stocks appear more susceptible than the broader market, which could be viewed as bearish, given that the recent market rise has been primarily driven by AI trends.

As with the S&P 500, holding onto existing positions again seems prudent, but new trades should be delayed until reaching an all-time high above 26,288.

Japan’s Nikkei 225 has performed notably well this year, outpacing the traditionally strong U.S. market, up over 63% since April. This impressive rise is attributed to a global bull market and signals of Japan’s economic recovery from prolonged deflation. The Bank of Japan’s recent decision to maintain low rates also contributed.

While new long positions may be put on hold, a quarter-sized long position with a trailing stop could be a smart approach.

Closing at record highs across the board is certainly a bullish indication, especially as the Nikkei outperforms the KOSPI Composite Index, suggesting going long here makes sense.

In summary, the top trades for this week include:

- Long USD/JPY currency pair after closing above 154.25 yen.

- Longs on the S&P 500 index upon closing above 6,920.

- Long on the Nasdaq 100 Index after closing above 26,288.

Looking to act on weekly forex forecasts? Check our curated list of the top ten forex brokers.