The Resilience of the 60/40 Portfolio

Back in 2019, I wrote a eulogy for the 60/40 portfolio, which blends 60% stocks with 40% bonds. It seemingly vanished on October 16, 2019, mainly due to persistently low interest rates and some questionable decisions by the Federal Reserve. This marked the 27th time in a decade that it had “disappeared.” Some might hope it stays gone this time, especially those who often caution against timing the market or who favor day trading.

Despite my feelings about it, there was little I could do. Year after year, various financial outlets labeled it “dead.”

Low bond yields have really complicated things for anyone aiming for a balanced portfolio. When I first wrote my piece, the yield on the 10-year Treasury stood at about 1.5%. That was likely to drop even lower as the pandemic began, dipping below 0.5%. Shortly after, interest rates climbed back to around 5%. By 2022, it almost felt like the end for the 60/40 portfolio; it was a tough year for investments, almost like getting hit by a truck. But then again, here we are.

Interestingly, short-term Treasuries and cash entered the scene, offering some stability on the fixed income side. Understandably, many investors hesitated to hold bonds after the rough experiences of recent years.

Those who invested in a comprehensive bond market fund faced the poorest returns in history for high-quality bonds. Throughout the 2010s, when bond yields were skimp, investors were pushed not only to take on more risk but also into more complex investment strategies. Some asset managers seem to believe that success hinges on venturing into alternatives, leveraging, or private placements.

Now, I don’t completely dismiss these types of investments. While they may not suit every investor, they can work for those who grasp the complexities and know how to navigate them rationally. However, adding layers of complexity can make managing a portfolio much trickier. High fees, low liquidity, and the challenges of rebalancing contribute to confusion, and sometimes, even if you understand what you’re doing, the results might still not be what you hoped for.

It’s worth noting that the bond market suffered immensely in 2022, as investors faced principal losses while yields rose significantly. Bonds are often seen as a boring investment, so they aren’t likely to revolutionize things anytime soon. Yet from 2022 onwards, profits are expected to grow gradually due to rising yields.

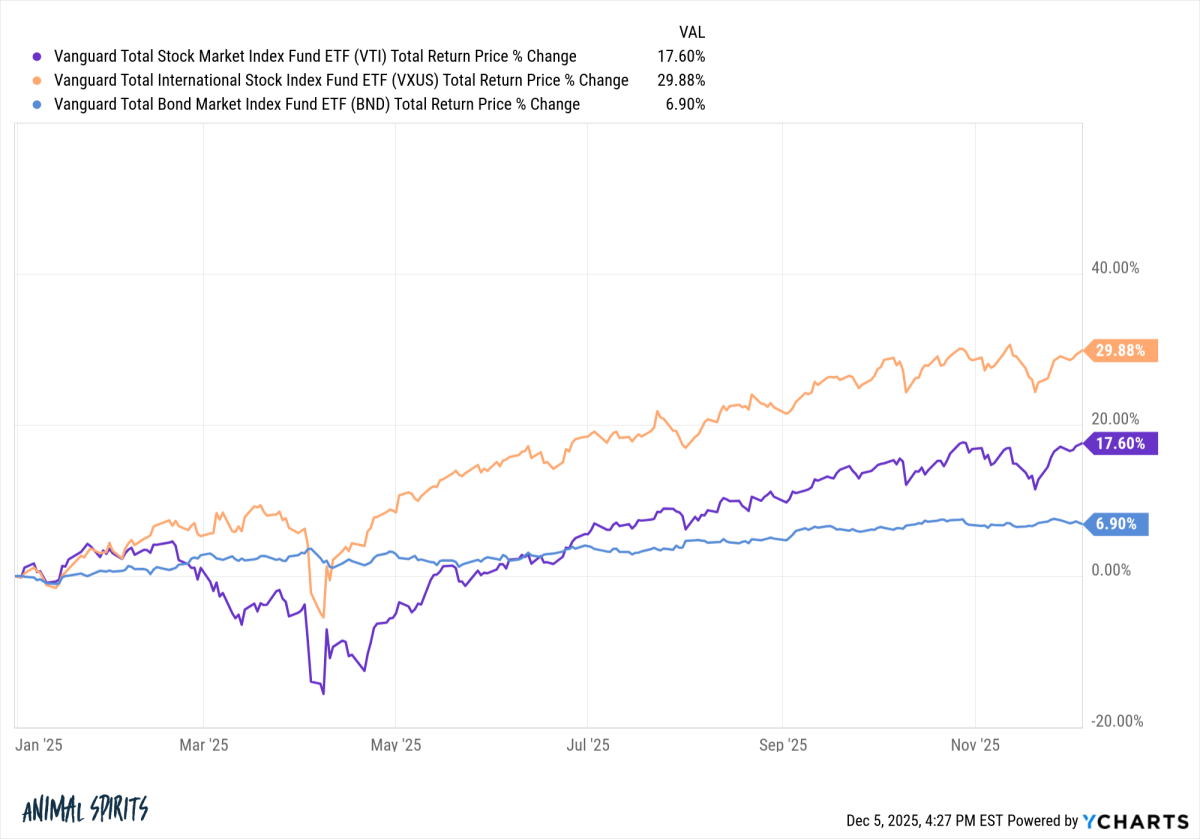

If you take a look at a straightforward three-fund Vanguard portfolio this year, things are looking pretty good, and that includes the bond segment.

International stocks have rallied by 30%, and US stocks are up nearly 20%. But bonds? They’ve increased by almost 7%, making this a fantastic year for them.

When you put it all together, a 60/40 portfolio made up of these three funds could see a rise of nearly 16% in 2025. That’s quite an accomplishment.

This particular portfolio managed to grow by 7.8% annually in the 2020s, even after enduring the worst bond market crash in history.

So, rather than saying the 60/40 portfolio is gone, it seems more accurate to say it just took a little nap for a year or two.

In the realm of investing, being boring is still quite effective.

Recently, I discussed the Plain Vanilla portfolio and more in a video.

Well, I’ve also been reading up on some interesting titles.

Just to clarify:

- 60% US stocks, 20% international stocks, 40% bonds.

- This portfolio dropped by 16% in 2022.