Understanding the Weakening Dollar

I’m constantly searching for engaging graphs that can shed light on what my clients find interesting or highlight ideas that might get overlooked. Recently, a quarterly conference call I participated in—kicking off in 2026—zeroed in on the weakening dollar. Given the potential impact of a faltering US dollar, it’s essential to explore what’s happening with this global reserve currency and its consequences for stocks, bonds, and commodities.

In 2025, international stocks finally began to rival the US market. Until that point, the US had been at the forefront of the global economy and stock market. However, everything shifted last year as international stocks surged more than 33%, far outpacing the relatively modest gains of the S&P 500 and Nasdaq 100. To put it simply, international stocks were seeing about double the growth compared to those in the US.

What’s the simple explanation for this? The US dollar hit its lowest point since 2017.

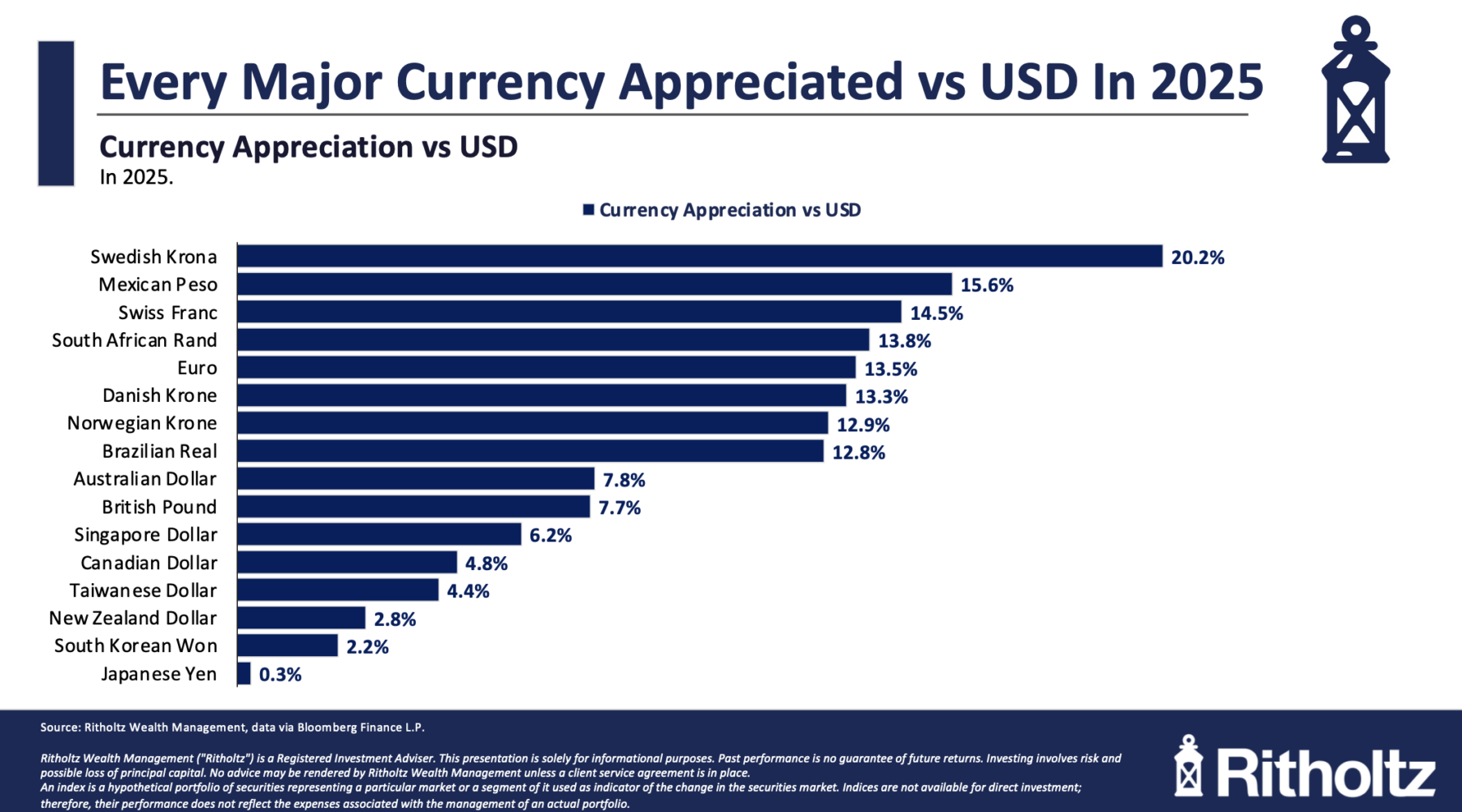

As illustrated in the accompanying chart, every major currency outperformed the dollar in 2025. Yes, even Japan’s currency gave the US dollar a run for its money.

Now, this isn’t about politics or any partisan issue; it’s just the reality. The dollar declined by 9.2% last year. The last time it experienced such a drop was in 2017, when it fell 9.9%. Interestingly, both instances occurred during Trump’s initial term and were influenced by customs duties and diminishing trading partners.

Foreign investors, including private equity, sovereign wealth funds, and public money sources, are now opting to reduce risks associated with the US. They’ve been selling U.S. stocks, converting their profits into local currencies—like euros, pounds, or yen—and investing back in their own markets.

I genuinely can’t think of another valid reason for all these currencies to strengthen against the US dollar without considering these dynamics. Usually, interest rates and the dollar hang together in a somewhat predictable fashion. When you see this kind of deviation, it suggests that something unusual is happening.

This situation reveals what can occur when trading partners and security allies grow discontented with US policy. They essentially “vote” with their dollars.

I wouldn’t call myself an alarmist. I don’t believe this foreshadows the end of the dollar as the world’s reserve currency or a complete demise of US influence. Still, it’s a situation to monitor closely. Treating your trading partners poorly usually invites pushback. They don’t just roll over; they respond, perhaps by investing in local assets.

Given that global markets are performing better than those in the US, it raises questions. What might spur a change in this trend? I have my doubts that this administration will adjust its course without significant push from the Supreme Court, and frankly, I’m surprised they haven’t acted in straightforward cases.

This is how I see the narrative surrounding the dollar.

Previously:

Tariff Update (January 27, 2026)

Stocks and Market Myths (January 16, 2026)

Potential for Tariff Reversal (November 5, 2025)

Probability Machine (August 28, 2025)

Can Tariffs Be “Overturned”? (July 31, 2025)

MiB: Special Edition on Global Tariffs (September 3, 2025)