ETFs and mutual funds are popular options for investors looking to diversify their portfolios. They both involve pooling money from various investors to buy a collection of assets like stocks or bonds. However, they differ quite significantly in their structures, and these differences can impact returns.

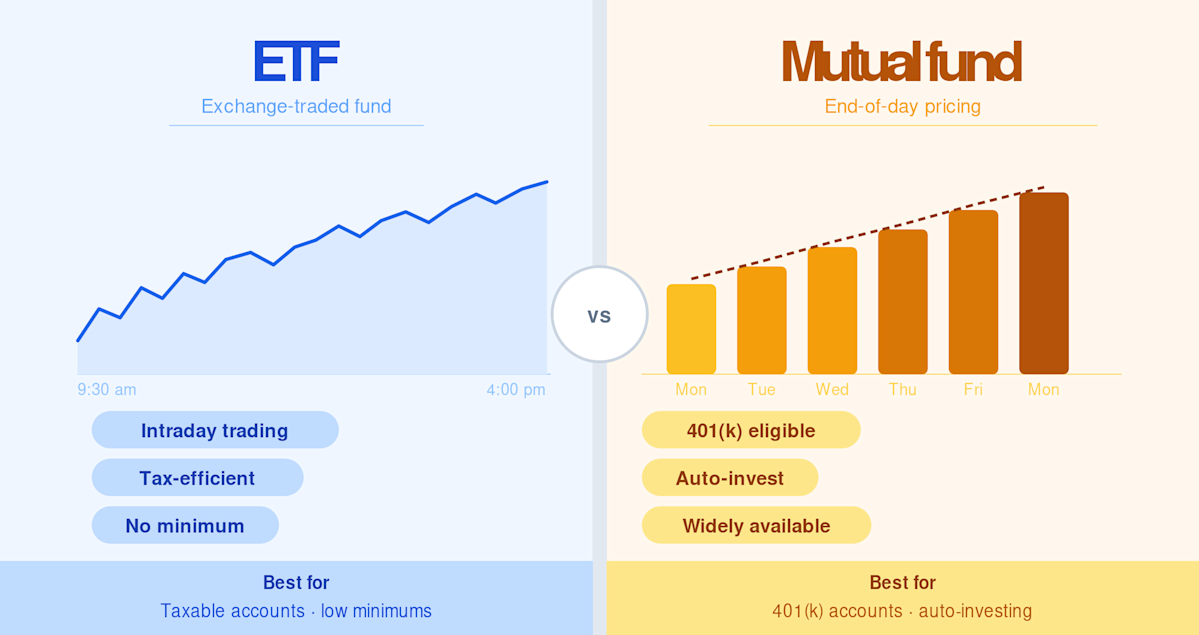

In a nutshell, ETFs tend to be more cost-effective, tax-efficient, and flexible compared to mutual funds. Mutual funds might be a better fit for those looking for automatic investing options, such as through 401(k) plans, especially when the exact timing of trades isn’t critical. Let’s dive into the specifics:

Key Differences: ETFs vs. Mutual Funds

| ETF | Mutual Fund | |

|---|---|---|

| Trading | Exchange intraday (similar to stocks) | Once a day at end-of-day NAV |

| Typical Expense Ratio | 0.03% to 0.20% (index) | 0.03% to 1.0%+ (index to active) |

| Tax Efficiency | High (in-kind redemptions) | Low (cash redemptions can create taxable events) |

| Minimum Investment | Price of one share (can be fractional) | $0 – $3,000 (varies by fund) |

| Automatic Investment | Limited (depends on brokerage) | Generally easy (many funds support it) |

| Available in 401(k) | Rarely | Yes, most 401(k) plans offer mutual funds |

| Commission | $0 at major brokerages | $0 (no-load funds) |

Cost Comparison: Generally in Favor of ETFs

When looking at costs for index investing, they tend to be quite similar. For instance, the Vanguard S&P 500 ETF has a fee of 0.03%, which isn’t much different from the 0.04% fee for VFIAX, a related mutual fund. Fidelity even offers a fund with a 0.00% fee. At this level, the costs aren’t a substantial concern.

However, the difference is more pronounced with actively managed funds. Morningstar’s data shows that these have average annual fees around 0.66% while managed ETFs often fall between 0.20% and 0.50%. This structure tends to appeal more to budget-conscious investors.

Over the long haul, a difference of 0.20% compared to 0.66% on a $100,000 investment really adds up, so understanding costs is crucial.

Tax Efficiency: The Advantage of ETFs

ETFs have a clear advantage when it comes to tax efficiency, which goes beyond just expense ratios.

With mutual funds, when investors redeem shares, the fund usually needs to sell underlying securities to raise the necessary cash. If those securities had gained value, the resulting capital gains can be passed down to all shareholders, even those who didn’t sell their shares. In fact, Vanguard’s actively managed funds in 2023 distributed an average capital gain of 4.7% of its NAV, putting shareholders on the hook for taxes for gains they didn’t even realize.

ETFs avoid this issue thanks to an in-kind creation/redemption mechanism in the primary market. Authorized participants who redeem ETF shares receive a basket of the underlying assets instead of cash, meaning no taxable events occur for investors.

For taxable accounts, this distinction can represent a difference of 0.5% to 1.0% yearly in after-tax returns, making even minor differences in expense ratios seem less significant.

Trading: Flexibility of ETFs

ETFs are traded on exchanges throughout the day just like stocks. You can buy in the morning, sell later in the day, and control prices through limit orders, which gives you a clear view of your transaction costs as soon as each order is filled.

Mutual fund prices, however, are only available once a day at 4:00 PM ET. If you make a buy order at noon, you won’t know the executed price until the end of the trading day. You also can’t use limit orders or stop-loss strategies with these funds, making them less flexible. Although for many long-term investors, the ability to trade intraday might not be that useful, it can lead to impulsive decisions if you’re not careful.

Yet, for those wanting more control over their transactions, ETFs are often preferable.

Minimum Investment: ETFs Win for Smaller Investors

Most mutual funds require an initial investment between $1,000 and $3,000. For instance, Vanguard’s Admiral Shares typically start at $3,000, while Fidelity’s ZERO Fund has no minimum but is only for Fidelity customers.

Conversely, ETFs can be purchased for the price of a single share, with some brokerages offering the ability to buy fractions as low as $1. This accessibility makes ETFs more appealing for new investors or those looking to build a portfolio gradually.

Automatic Investing: Mutual Funds Hold the Advantage

This is one area where mutual funds clearly have the upper hand. Most platforms let you set up automatic purchases easily, such as buying a certain amount of shares every month without worrying about market fluctuations. This method is perfect for dollar-cost averaging.

While some brokerages do allow automatic investing in ETFs, it’s not as widespread. If your brokerage doesn’t enable automatic fractional shares, you’ll have to place orders manually each time.

So, if you’re someone who prefers a hands-off approach, mutual funds may be more convenient.

401(k) Plans: Mutual Funds Dominate

Typically, 401(k) plans primarily offer mutual funds instead of ETFs. It’s not a judgement call—just how the retirement planning structures are set up. Your employer selects the options available in the plan, which nearly always includes mutual funds.

If you have access to a low-cost index mutual fund within your 401(k), it’s usually worthwhile to use it due to the significant tax advantages associated with 401(k) accounts. The tax benefits of pre-tax contributions and tax-deferred growth greatly outweigh the differences between ETFs and mutual funds.

ETFs are best utilized in brokerage accounts and IRAs where you have more flexibility in decisions about your investments.

The Verdict: Which to Choose?

Opt for ETFs if:

- You’re investing in a taxable account—this is where tax efficiency really matters.

- You prefer to start small, as there’s no minimum investment necessary.

- You value ease of transaction over automatic purchases.

- You want to build a holistic portfolio with control over costs.

On the other hand, choose mutual funds if:

- You’re contributing through a 401(k)—most plans don’t offer ETFs.

- You prefer automatic monthly contributions—mutual funds excel here.

- You’re after the lowest cost index fund (often equivalent to an ETF), particularly from Vanguard or Fidelity.

- You don’t want to stress over market timing or stock prices.

For many investors, the practical approach is: Use ETFs in taxable accounts for their tax advantages, while utilizing low-cost index mutual funds through your 401(k). These will likely be mutual funds.

Ultimately, the distinctions between a well-chosen ETF and a well-chosen mutual fund are not immense. However, the gap between either of those and high-cost actively managed funds is significant. So, aim for the lower-cost options available for each type of account and focus on remaining invested.

Conclusion

ETFs and mutual funds share more similarities than differences. Both can effectively track the same index and generally do so at comparable costs. The structural edge that ETFs have—like tax efficiency and intraday trading—holds substantial value in taxable accounts. On the other hand, the benefits of mutual funds, such as automatic investing and availability in 401(k)s, carry greater importance for retirement savers and more passive investors. In the end, many portfolios will likely blend both options.