Credit cards are the primary payment method for everything from business travel reimbursements to e-commerce and bar tabs. And some people borrow it and use it.

Written by Wolf Richter of Wolf Street.

Credit cards are a measure of spending, not borrowing. They are the primary payment method for consumers in the United States and have largely replaced checks and cash. They’re used to pay for everything from bar tabs to reimbursed business trips, and they can be expensive. According to the Nilsen Report, credit cards accounted for $5.8 trillion in transactions in 2022. New data shows consumers spent more than $6 trillion on credit cards in 2023, but only a small portion of that was held up as interest-bearing debt. Most were paid off on time without interest. And that’s what we’re looking at here.

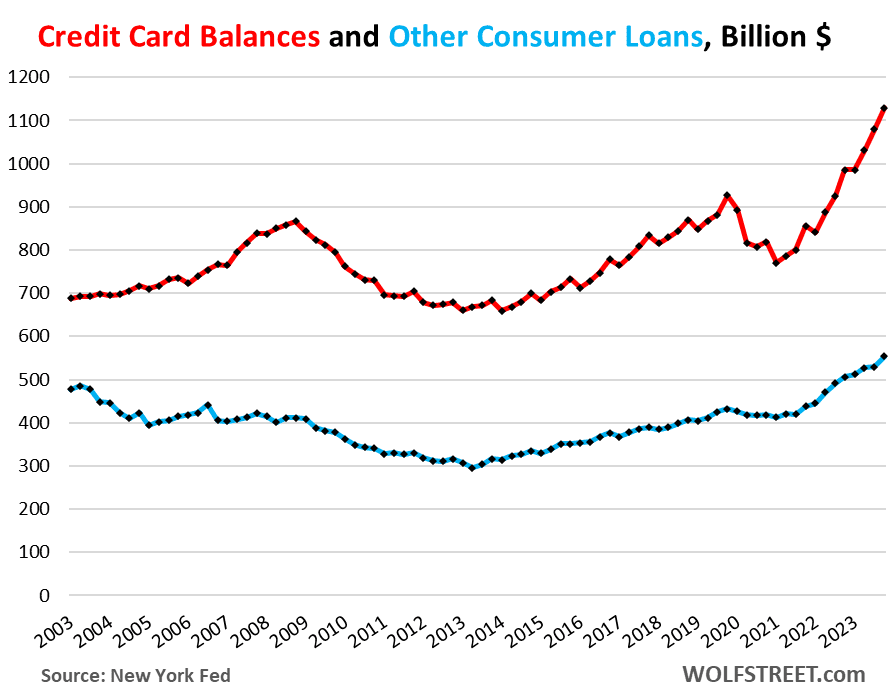

According to the New York Fed’s Household Debt and Credit Report, credit card balances (red line in the chart below) (statement balances before payments) increased by $50 billion from the third quarter to $1.13 trillion in the fourth quarter. became. Credit card balances rose 14.3% year-over-year as spending on goods and services increased significantly, including “revenge spending” on travel, restaurants and entertainment. That’s what we’ve come to affectionately and playfully call drunken sailors, but that’s not the case. Their income has increased faster than their expenses and they have been able to save some money, so they are very intoxicated.

“Other” consumer loans (blue line), such as personal loans, payday loans, and buy-later-pay-later (BNPL) loans, grew $25 billion in the fourth quarter from the third quarter and 9.3% year over year. increased by $47 billion. Over a year. BNPL loans are short-term loans that are subsidized by merchants and are interest-free for customers. And the entire loan he has to repay in 4-5 payments. they have been around forever. But now it’s more convenient. Note that the balance has increased very little over the past 20 years, even though population, income, and spending have increased.

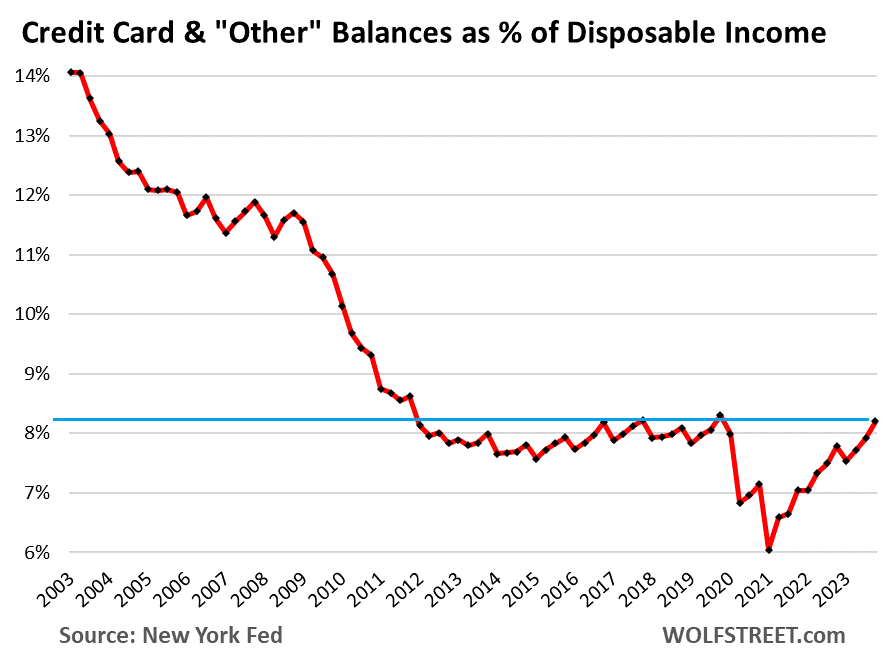

Credit card balances relative to disposable income.

Credit card balances and “other” consumer debt combined are $1.68 trillion, and disposable income (income from all sources except capital gains, less taxes and social security contributions) is the sum of $1.68 trillion that consumers This amounted to 8.2% of the income (income surplus to expenses).

This measure of credit card balances and other consumer loan burdens in relation to disposable income is up from record lows in free money and within the range of good pre-pandemic times.

One more thing to note. Twenty years ago, that rate was 14%, and some consumers ran into trouble during the Great Recession. Apparently, some lessons have been learned.

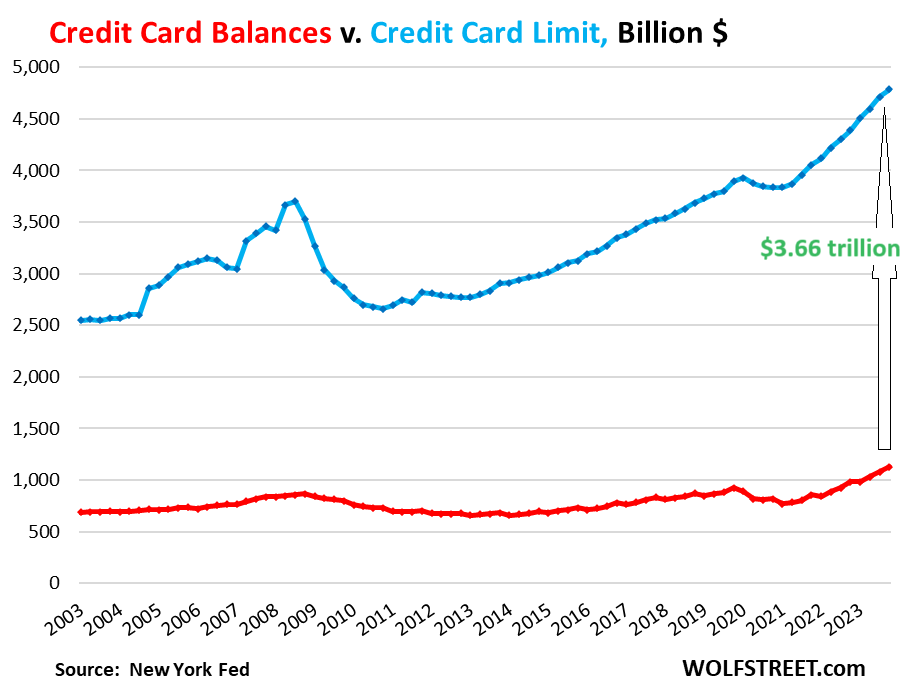

Credit is not tight except for subprime..

Despite all the fuss last year about credit tightening for consumers (now forgotten, even the Fed removed this language from its January meeting statement), credit tightening in the credit card space Not yet. Banks are as aggressive as ever to get people to open new accounts and are raising credit limits, with total credit limits surging at a record pace last year and rising in the fourth quarter. has reached $4.79 trillion, and credit card balances are also increasing. It reaches $1.23 trillion.

And the total amount of unused credit available soared to a record $3.66 trillion. The credit crunch occurred during and after the Great Recession, as evidenced by the sharp decline in unused credit (blue line) as banks lowered credit limits, closed accounts, and healed wounds.

Subprimes always face more or less problems, that’s what makes them subprime. And, as we’ve already seen with auto loans, the subprime market is tight. But for others, banks want to lend them money.

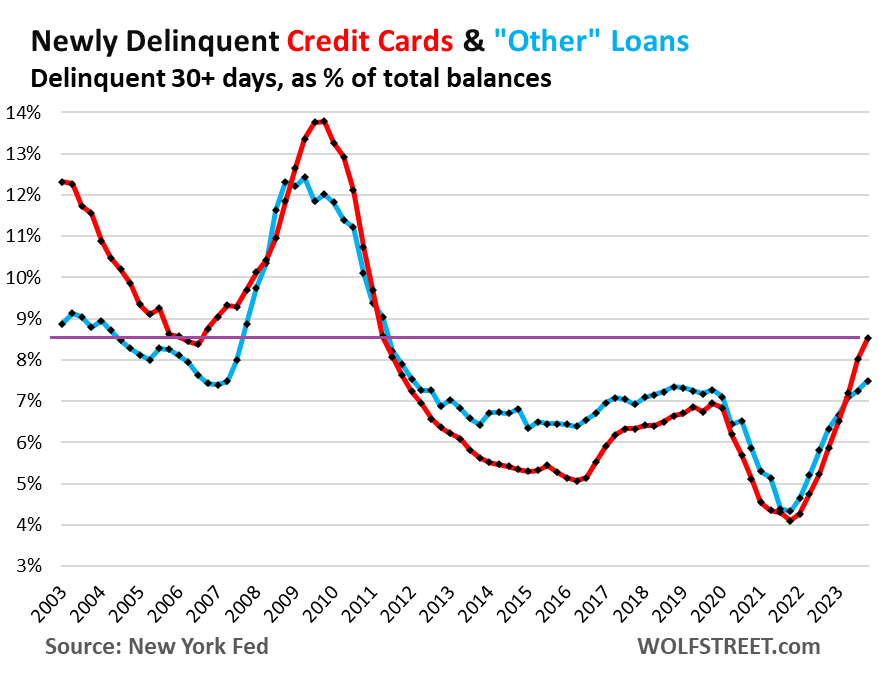

The arrears left a trough of money at their disposal.

Reality is setting in for some people. Credit card balances that were more than 30 days past due (transitioned to delinquent at the end of the quarter) increased to 8.5% in the fourth quarter. The rate in 2019 was approximately 7.0%. Before the Great Recession, his 8.5% was near an all-time low (red line).

“Other” consumer credit in arrears, including BNPL, rose to 7.5%, slightly higher than in 2018 and 2019 (blue).

How many American adults are behind on their credit cards?

new york fed bank study In November, just 2% of credit card holders were found to be more than 30 days past due, based on data from Equifax and the company’s own Consumer Credit Panel. That means 98% of his credit card holders still have one. But they are cardholders.

According to TransUnion (February 2023 report), only about 166 million American adults have a credit card, which means 64% of the 260 million adults (18 and older) have a credit card. You will have a card. Her 36% of remaining adults did not have a credit card. They only had debit cards (the second largest payment method) or no cards at all. And since those Americans don’t have credit cards, they can’t default on their credit cards.

Therefore, the percentage of adults (not “cardholders”) who are 30 days or more delinquent on their credit card balances is approximately 1.7%. This may be tough for the 1.7%, but not for the economy.

We’ve already talked about drunken sailors’ mortgages, delinquencies, and foreclosures. Introducing the HELOC: Mortgage balances, delinquencies, and foreclosures. and their auto loans and delinquencies: auto loan balances, subprime, delinquencies, and income: Who are the drunken sailors?

Enjoy reading and supporting Wolf Street? You can donate. I appreciate it very much. Click on the beer and iced tea mugs to see how.

Would you like to receive email notifications when new articles are published on WOLFSTREET? Sign up here.

![]()