Jasmine Merdan/Moment via Getty Images

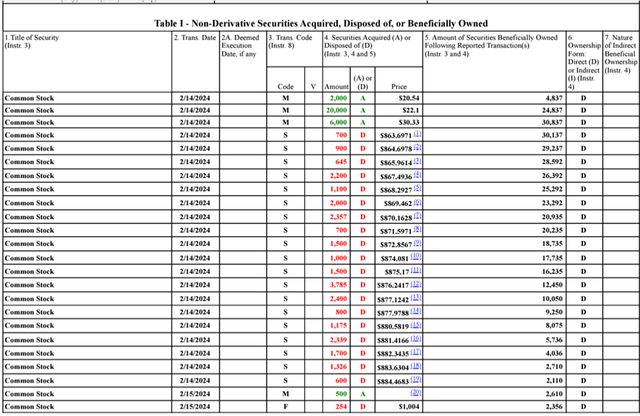

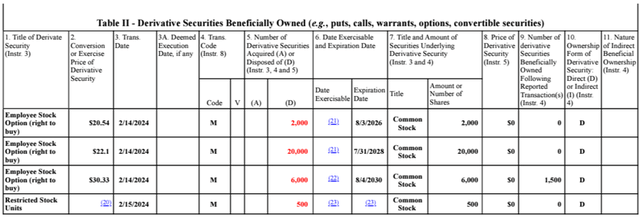

The first question that comes to mind after this huge rise in stock prices is the super microcomputer (NASDAQ:SMCI) There is still gas in the tank and the value will continue to rise. From January 2023 onwards, The stock price returned to 2.23 times and returned to the -20% level on February 16, 2024. A -20% drop in share price should ring alarm bells for any smart investor. but, Looking at the recently filed Form 4; Senior Vice President of Sales Don Clegg appears to have sold a large block heading into the weekend. The real question to ask is whether this selloff is the start of a new trend, and whether this large block sold by insiders is a signal to the market of impending events to come. Despite this decline in stock prices, I think: SMCI has significant upside potential given management’s ambitious growth strategy. I give him a Buy recommendation on SMCI stock, based on 5x FY25 sales and a price target of $1,700 per share.

form 4 form 4

operation

Q2 2024 was a watershed moment for SMCI, with the company experiencing strong top-line growth of 103% on a year-over-year basis. This level of growth shouldn’t go unnoticed for the 30-year-old company, as it plays a central role in the transition to high-capacity computing in his GenAI resurgence. Despite this rapid growth, management raised several concerns during the Q2 2024 earnings call, which are relatively common among companies that are at the center of enterprise AI initiatives. It appears to be. Palantir (PLTR) has seen similar interest in its platform, as more companies turn to AI technology to optimize their operations and then expand their sales teams to meet this growing interest. I experienced the challenges of SMCI is expanding with new facilities in Silicon Valley and Malaysia to meet growing interest in its hyperconverged infrastructure. SMCI serves as omnichannel for all major chip manufacturers, including NVIDIA (NVDA), Advanced Micro Devices (AMD), and Intel (INTC), making SMCI’s advanced computing systems a top choice for scaling GenAI in the data center. I believe that this will play an extremely important role. level.

JPMorgan (JPM) analyst Samik Chatterjee sees significant growth in the broader hardware market as AI takes shape.

As valuation multiples increase heading into 2024, the leveraging of AI in specific sections of broad hardware coverage presents a rerating opportunity, despite our cautious view of the sector as a whole in 2024. It’s likely to be a windfall moment. Discusses his increasing TAM opportunities regarding AI.

Although this article refers to SMCI’s competitors, the main point is that SMCI has continued growth opportunities within a growing TAM, and valuations will rise as hardware refreshes rise periodically. I think that’s getting across.

Turning to operational aspects, SMCI has a production capacity of 4,000 lacs/month as of Q2 2024. As of this period, the company has a production capacity of 1,500 racks/month of racks with direct attach liquid cooling and expects capacity build to reach 5,000 racks/month. I believe this additional capacity will allow his SMCI to drive significant revenue growth, as this type of cooling is essential for the next generation of high-performance computing. As of Q2 2024, the company’s facilities were operating at 65% occupancy across its U.S., Netherlands and Taiwan facilities, and that gap is rapidly closing. The company is aggressively expanding its production capacity with a new facility in Silicon Valley and a facility in Malaysia, as well as expanding capacity (2-3x) at facilities in the Asia-Pacific region, which will increase the company’s size. It provides a low-cost, high-volume solution to your expansion challenges. With this additional build-out, I believe management anticipates margin headwinds due to headcount and capital equipment additions, which could result in an additional four to two quarters of negative free cash flow. thinking about. I don’t think capital outflows should be a concern as the company is in a revitalized growth phase and needs to invest in working capital and capital equipment to meet market demands. With these new facilities, management believes the company will be able to meet its annual revenue goal of $25 billion. Despite the near-term margin headwinds, I believe that once the facility is built and operational, SCMI will enjoy economies of scale as it is positioned to meet market demand for integrated solutions.

Looking to the financials, SMCI expects strong revenue growth to continue in FY24-FY25 as it scales up production on the back of the AI boom. The company expects some margin compression through gross profit and operating profit as the company enters a period of significant capital and operating investments to expand its business scale. As the company achieves this scale, we expect margins to trend upward through FY2025, but have yet to reach FY23 margins.

corporate report

Although I’m optimistic about the company, there are some negative risks to consider before building a position. Geopolitical risks between ~are increasing~ Taiwan and China If tensions escalate, SMCI’s production could be affected. 14.7% of its total sales in FY23 came from Asia, making this a long-term but potential risk to consider when making investment decisions. Another risk worth considering is whether the company’s sales strength will continue as it invests in these new facilities. If AI regulations become more stringent and infrastructure demand suddenly drops, SMCI could be at a disadvantage with excess capacity.

Finally, there is Taiwan Semiconductor (TSM). double the ability CoWoS supports Nvidia’s growth with advanced chip packaging processes. This could be a positive signal for demand for SMCI’s infrastructure.

Value and shareholder value

corporate report

Ultimately, you need to think about how to evaluate SMCI. The older group of IT infrastructure companies does not justify SMCI’s high trading multiple, which is very expensive by comparison.

corporate report

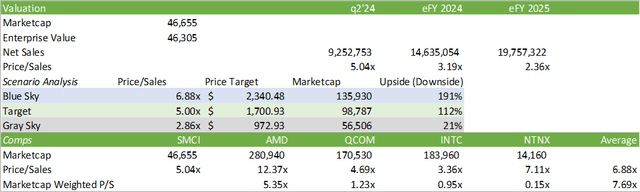

Comparing SMCI to AI technology names such as AMD, QUALCOMM (QCOM), Nutanix (NTNX), and INTC provides a more realistic comparison as the company’s recent valuation increases are more similar to this group of companies. You can get it. Considering these results, 6.88 times sales is too high for SMCI as it relies heavily on hardware integration in its business operations and its profit margins do not expand as much as its peers even as it expands its business scale. I think it comes down to evaluation. I believe that this 6.88x figure is an absolute sky-high valuation that will probably never materialize. I think the current valuation of 5x sales is more appropriate for his SMCI, with 112% upside potential based on FY25 earnings. I believe this recent decline was unwarranted given the massive sell-off by insiders and the fact that there is still gas left in the tank for SMCI stock. I recommend his SMCI stock as a buy based on eFY25 earnings with a price target of $1,700 per share.

corporate report

technical trading

On the tactical side, using Elliott Wave theory, the stock should recover and reach $1,345 per share in the next cycle before returning to around $1,125. From there, the stock should reach my basic price target of $1,700 per share in the final wave. For active traders, I believe each pullback is a buying opportunity to build a position. Be aware that tactical trading does not provide evidence that a stock will reach its potential, and be aware of the risks you are assuming when trading short-term positions.

TradingView