Tumsa Sedgar

The March Consumer Price Index (CPI) report showed that inflation was actually accelerating, rather than slowing as some expected, and many high-yield stocks (SPYD) (SCHD) were sold off. Since the beginning of the year, the stock has been significantly underperforming compared to the S&P 500 (SPY).

move Going forward, it seems increasingly likely that the Fed will need to be somewhat cautious about the pace of rate cuts to prevent inflation from spiking again. This article examines three important implications of that reality. Together, each provides an important warning to high-yield investors.

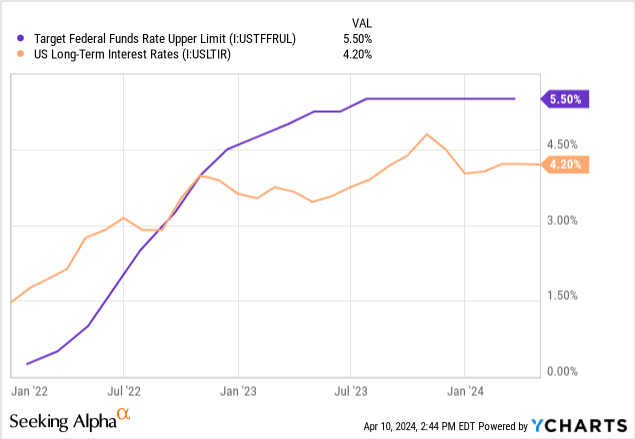

#1. Long-term interest rates are probably too low

Both short-term and long-term interest rates have risen significantly since the Fed’s rate hike campaign began in early 2022. However, short-term interest rates have risen much more than long-term interest rates, creating an inverted yield curve today.

This likely reflects the fact that the market expects the Federal Reserve to reduce short-term interest rates significantly over the next few years, thereby eliminating the curve inversion. But based on recent data, inflation appears to be hitting a brick wall well above the Fed’s long-term goal of 2%, and the Fed may not be able to meaningfully lower rates for some time. This means that to reverse the inverted yield curve, long-term interest rates will most likely need to rise significantly, rather than short-term rates fall.

#2. Pressure on trading partners is likely to increase

As inflation turns out to be stagnant and therefore it is becoming increasingly unlikely that interest rates will fall (in fact, as we have just discussed, long-term interest rates are likely to rise), trading partners for high-yield stocks. are very likely to face increased financial pressure. .

For example, REITs such as Simon Property Group (SPG), Realty Income (O), and Medical Property Trust (MPW) (VNQ) have suffered from the deadly combination of inflation and rising operating costs due to inflation. You may have to deal with tenants who are becoming increasingly financially challenged. Rising cost of capital due to high interest rates.

BDC (BIZD) is not exempt from this challenge either. This is because BDC’s counterparties will also face a difficult environment, with short-term interest rates on many borrowings remaining high, as well as business and input costs remaining high. persistent inflation. In fact, blue-chip BDC firm Ares Capital (ARCC) recently warned of this very phenomenon in its Q4 2023 earnings call, with the company’s CEO stating:

We have said in the past that defaults are likely to increase in the industry this year. It takes a while for that to show up, right? So there are some companies in the bottom quarter of our portfolio, and probably in your portfolio as well, that continue to live on revolver availability, cash, etc. while paying interest, but liquidity is becoming increasingly tight. So my prediction is that defaults will increase this year.

Utilities (XLU) may also face some pressure, particularly in politically more liberal jurisdictions, as higher interest expenses coupled with a more difficult base rate case could weigh on margins. There is sex.

#3. The possibility of a soft landing is increasing

The economy is starting to show some signs of fraying due to lower savings rates, record levels of consumer debt, weakening consumer sentiment and rising unemployment. If inflation persists and interest rates remain high, it will only cause more stress for consumers. The aforementioned increased stress on some businesses could further increase unemployment and further weaken consumers.

Additionally, there is a wall of commercial real estate debt that will come due in the coming months and years and will have to be refinanced at much higher interest rates than originally assumed in the past. This could trigger a wave of defaults and a commercial real estate apocalypse, and for CRE-sensitive regional banks (KREs), further developments could mirror what New York Community Bancorp (NYCB) experienced. May cause challenges.

Ultimately, combined with the headwinds from economic downturns that have already begun in Europe, Japan, China, and elsewhere, this could be enough to send the U.S. economy into recession. While this economic downturn may ultimately eliminate inflation, it is also likely to kill many jobs and businesses and cause significant pain for high-yield investors.

Takeaway for investors: Important warning

What this means for high-yield investors right now is that any investment thesis based on rapidly declining interest rates is extremely risky, if not foolhardy. For example, NextEra Energy Partners (NEP) will face debt and his CEPF maturity wall in the coming years and will it be able to sell pipeline assets and tap capital markets to overcome this minefield? It depends a lot on what you do. NEP looks attractive with a distribution yield of around 12%, but its high leverage and interest rate sensitivity make it a very risky bet at this point.

Instead, high-yield investors would be wise to pursue opportunities that are far less dependent on near-term interest rate declines. For example, midstream stocks like Enterprise Products Partners (EPD), infrastructure stocks like Brookfield Infrastructure Partners (BIP) (BIPC), and REITs like Agri Realty (ADC) all have very strong balances. In the short term, there is little dependence on capital markets. Be able to implement business strategies. However, all three companies still offer very attractive current yields and also have solid long-term growth prospects.

Weak market sentiment for the high-yield sector creates a huge opportunity for value investors to buy high-quality stocks at deep discounts, but it also creates an opportunity for investors whose investment thesis is driven by interest rates. It is important to avoid and navigate this sector carefully.