Emerging markets outperform

The fourth quarter started on a positive note for investors. of Morningstar US Market Index Despite the brief period of panic that plagued investors in August and September, it rose 6% compared to the third quarter. However, these gains were overshadowed by markets outside the United States. Developed markets excluding the US and emerging market Both indexes rose 8.2%. The latter was supported by Chinaan increase of 28.6% in the quarter. Emerging market stocks took advantage of the dollar's weakness, falling 4.3% against the euro over the quarter.

Number of jobs moves dollars

Against this backdrop of optimism, Friday's employment report was well received. The unemployment rate unexpectedly fell to 4.1% (254,000 compared to the expected 150,000) as more jobs were created in September. The dollar rose 0.5% against the euro for the week and two-year Treasury yields rose 0.2% as market participants digested the impact of future interest rate cuts. Morningstar Markets Editor Tom Lauricella digs deeper into the data.

European stocks increase in value

Despite the recent surge in stock prices, Morningstar analysts continue to believe that the U.S. market is I see value in the department. However, we see greater opportunity outside the United States, as shown in the table below from Morningstar's Q4 European Market Outlook. This is a comparison of the price/fair value ratios of US stocks and European stocks as of September 19th. In these markets, European assets appear to offer better value than those in the United States.

High yield bonds are lagging behind stocks

When assessing whether a return is attractive, people either look at it through an absolute lens (how much did it rise?) or a relative lens (did it give a higher return than other assets presenting similar risks?) I tend to use . But for most investors, the third lens is more helpful. Did it do the job it needed to do?

This is especially important when considering: US high yield bondsreturned 5.3% in the quarter and 15.7% in the past 12 months. These assets combine some of the characteristics of stocks and high-quality bonds, allowing investors to choose between controlling risk or delivering returns in their portfolios. The 15.7% return is high, but lower than the stock's return over the same period, making it a disappointing replacement. And while high-yield bonds didn't fall as much as stocks in early August, they still show a positive correlation, which isn't helpful if the assets are used for risk management. In this context, returns on high-yield bonds can be considered disappointing.

This shows the importance of giving all assets a clearly defined role within a portfolio. Otherwise, you may misjudge the attractiveness of expected and realized returns and make avoidable mistakes when changing your portfolio.

Earnings season is heating up again.

Individual stocks will be in the spotlight again in the coming weeks as U.S. companies, starting with banks and asset management companies, report their third-quarter results. Analysts last week lowered their forecast for U.S. market earnings growth to 4.2% from 7.8% at the end of June. This is not unusual, as companies are keen to lower expectations before earnings in order to create positive “surprises” and associated stock price increases.

Rather than participate in this tedious game of expectation management, our analysts use data provided by companies to identify changes in the long-term prospects of a business and, by extension, changes in its fair value. You can follow this effort on our dedicated earnings page and see when companies report using our new earnings calendar.

CPI data deadline

After last week's drop in unemployment, market pundits will focus on the latest inflation data released on Thursday. Core consumer price inflation is expected to remain stable at an annual rate of 3.2%. A high number would likely raise concerns that the Federal Reserve would have to cut future interest rates more slowly, leading to volatility in asset prices.

Highlights of this week's market and investment events

- Monday, October 7th: consumer credit

- Wednesday, October 9th: minutes From the March Federal Open Market Committee meeting

- Thursday, October 10th: consumer price index report, First unemployment insurance claim Report, Revenue from Tilray Brands TLRY

- Friday, October 11th: producer price index Report, preliminary version University of Michigan Consumer Sentiment IndexBlackRock Finance BLK, JPMorgan Chase JPM, Wells Fargo WFC

Check out the complete weekly calendar of economic reports, consensus forecasts and company earnings.

For the trading week ending October 4th

- The Morningstar U.S. Market Index rose 0.21%.

- The strongest performing sectors were Energy (up 6.85%) and Utilities (up 1.17%).

- The worst performing sector was real estate, which fell 1.97%.

- The yield on the 10-year US Treasury note rose from 3.75% to 3.98%.

- West Texas Intermediate crude oil prices rose 8.51% to $74.57 per barrel.

- Of the 703 U.S.-listed companies covered by Morningstar, 427 companies (61%) increased, 5 companies remained unchanged, and 276 companies (39%) decreased.

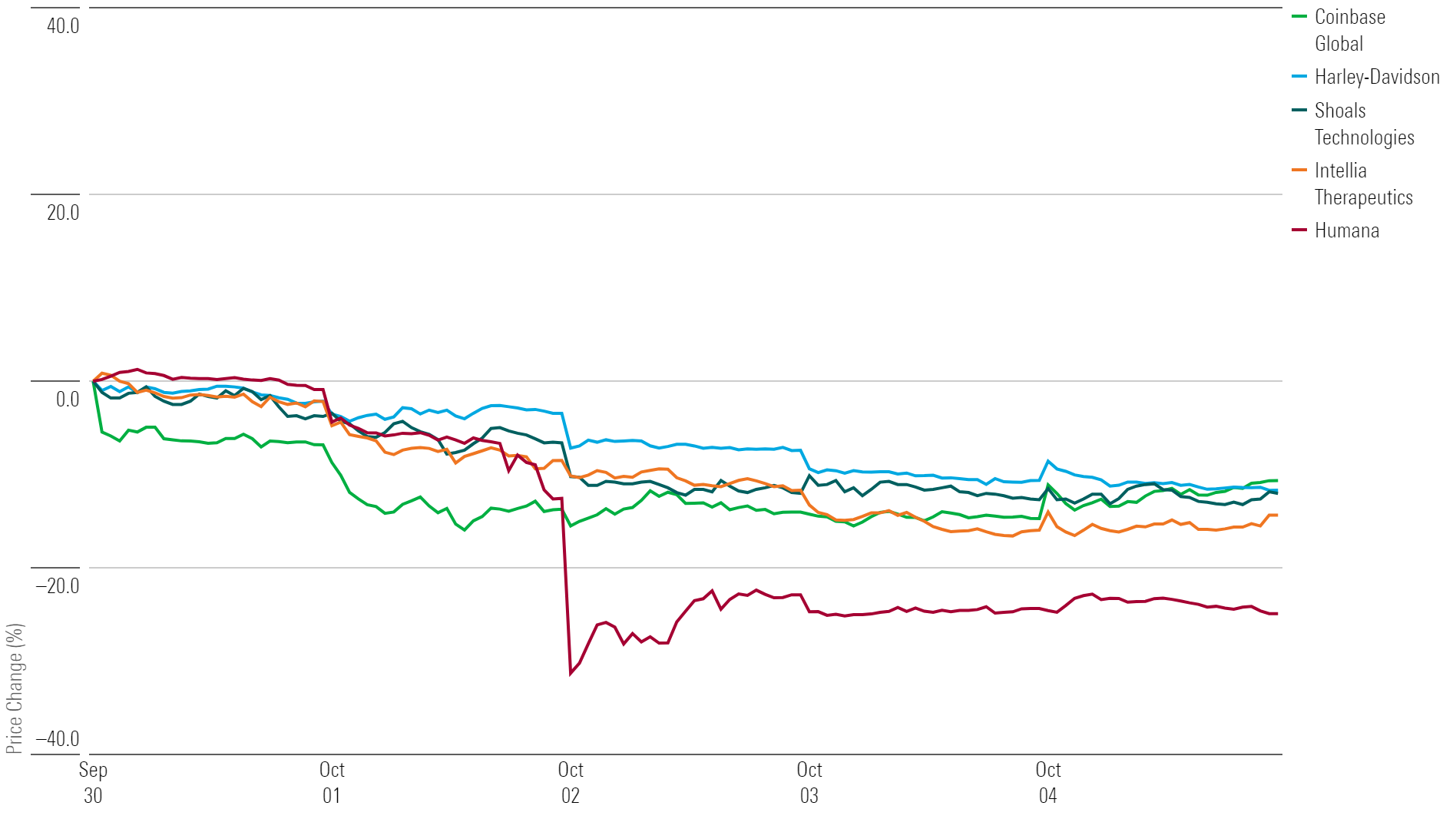

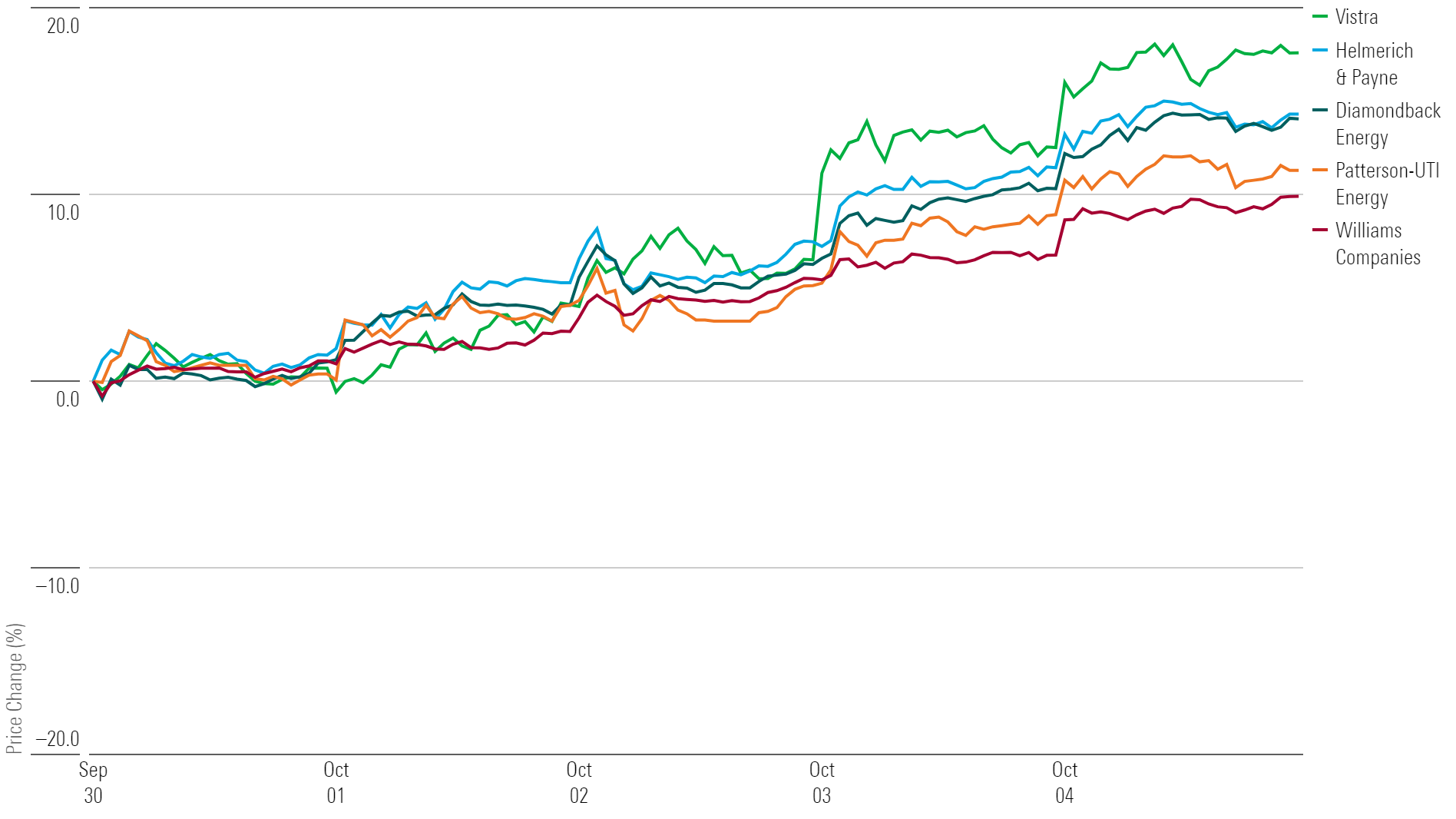

Which stocks are going up?

Vistra VST, Helmerich & Payne HP, Diamondback Energy FANG, Patterson-UTI Energy PTEN, Williams Companies WMB

Which stocks are falling?

Humana HUM, Intellia Therapeutics NTLA, Shoals Technologies Group SHLS, Harley-Davidson HOG, Coinbase Global COIN