defeat S&P500 Taking more than five years is notoriously difficult. Even highly trained hedge fund managers often have trouble doing it. If you want to make it work, it may be worth considering companies that have a track record of above-average profits and still have the strengths that led to their past success. Although these conditions are neither sufficient nor necessary to beat the market, focusing on these factors is a good starting point.

In that spirit, let's discuss two companies that meet these criteria. HCA Healthcare (NYSE:HCA) and vertex pharmaceuticals (NASDAQ:VRTX). Here's why their stocks could deliver higher returns than the S&P 500 through 2030.

1.HCA Healthcare

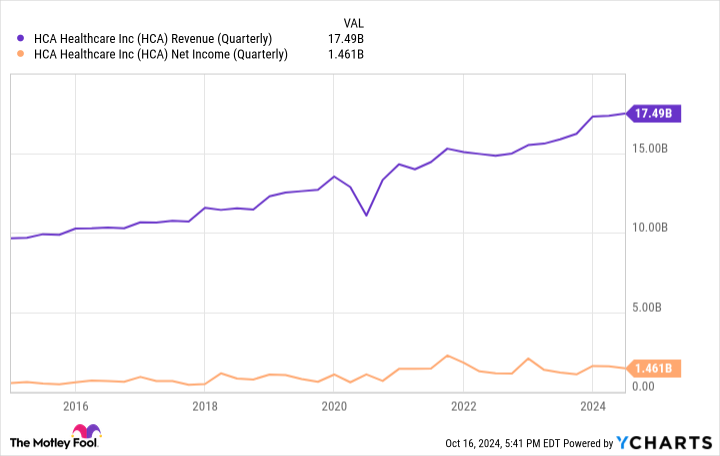

HCA Healthcare is a leading hospital chain in the United States with 186 hospitals and more than 2,000 different types of care centers. The hospital chain business is a difficult industry to break into. Challenges include managing dozens of medical facilities (an expensive plan) and building and maintaining relationships with physicians, patients, and third-party payers.

HCA Healthcare does these things as well as its competitors. In fact, the company's market share has generally increased over the years, outperforming most of its peers. Its market share rose from 24% in 2012 to 27% about a decade later. This includes the early years of the pandemic, when businesses experienced severe disruption. It was also grappling with economic issues, such as the need to rely on more expensive contract labor, which hurt profits.

However, HCA Healthcare has successfully navigated the situation. Unsurprisingly, the company achieved strong financial results along with increased market share.

What drives the company's success? Investing in facilities, updating equipment, and providing state-of-the-art services are all part of the company's strategy. HCA plans to further similar initiatives through 2030, by which time it aims to reach 29% market share. While the past does not guarantee future success, HCA Healthcare has proven strategies that can help you position yourself in a highly competitive and highly regulated industry.

In my view, the company is likely to perform roughly as well through 2030 as it has over the past decade.

2. Vertex Pharmaceuticals

Strong financial performance is important biotechnology industryAs in other cases. But drug companies must also demonstrate solid clinical and regulatory progress to impress investors. Vertex Pharmaceuticals can expect to outperform in both categories through 2030.

The company's drug portfolio, which treats cystic fibrosis (CF), a rare disease that affects internal organs, remains strong. Vertex is the only game in town. Vertex sells the only drug that treats the underlying cause of CF.

The company's progress in this area is a major reason for its generally strong performance over the past decade.

The second quarter's net loss was due to approximately $5 billion worth of acquisitions.

The company is now moving beyond CF. Its latest approval is Kasgevy, a gene-editing therapy for a pair of rare blood diseases: sickle cell disease and beta-thalassemia. Gene editing treatments will take time to implement, but within the next few years, Possibility of a blockbustershould meaningfully contribute to Vertex's sales and begin to improve its financial results.

On the regulatory front, Vertex Pharmaceuticals is awaiting approval for two new products: a new combination therapy for CF and a treatment for acute pain. Both should get the green light next year.

Given Vertex's pipeline, it should also see some clinical results in the coming years. The company is currently conducting a Phase 3 trial of inaxaprin in APOL-1-mediated kidney disease. There are some early-stage programs, including an investigational treatment for type 1 diabetes that has already shown some promise.

Vertex Pharmaceuticals has had enough progress that its stock has delivered above-average returns through the end of the 2010s. The company looks like an attractive option for long-term investors.

Don't miss out on this potentially lucrative second chance

Have you ever felt like you missed out on buying the most successful stocks? Then you'll want to hear this.

In rare cases, our team of expert analysts “Double Down” stock Recommendations for companies that are likely to take off. If you're already worried that you're missing out on an investment opportunity, now is the best time to buy before it's too late. And the numbers speak for themselves.

-

Amazon: If you invested $1,000 when it doubled in 2010; you have $21,285!*

-

apple: If you invested $1,000 when it doubled in 2008; That's $44,456!*

-

Netflix: If you invested $1,000 when it doubled in 2004; you have $411,959!*

We currently have “double down” alerts on three great companies, and we may not see an opportunity like this again anytime soon.

*Stock Advisor will return as of October 14, 2024

Prosper junior bakini There is a position available at Vertex Pharmaceuticals. The Motley Fool has positions in and recommends HCA Healthcare and Vertex Pharmaceuticals. The Motley Fool has Disclosure policy.

Prediction: These 2 stocks will outperform the S&P 500 through 2030 Originally published by The Motley Fool