Remember those bears who spent the spring and summer howling about rising unemployment numbers? September's better-than-expected jobs report finally silenced them. But if we hear any more bad reports in the coming months, we'll be back.

They would be wrong too. Over and over again. For each season.

This is because, quite simply, not only the unemployment rate but also employment growth are always lagging indicators. These are not useful as predictors of recession or the stock market. Except for the fact that false fear pervading the market is bullish (fear of false factors is always bullish).

It seems intuitively correct that rising unemployment causes a recession. Unemployment is often personal. One can imagine the pain and the cuts required. Consumer spending accounts for 68% of U.S. GDP, so layoffs would ripple through the economy and cause a recession. right?

Not at all. History shows that consumer spending is surprisingly stable, even during truly dire recessions. During the deep recession of 2007-2009, the broadest measure, personal consumption expenditures, fell by just 4.1% from peak to trough. During the 2001 recession, they generally rose (Excluding 9/11-related 1.6% month-over-month decline in September).

People who have recently lost their jobs are likely to skimp on luxuries. However, the majority of consumer spending is essential, not discretionary. Shoppers dig deep to keep buying groceries and primarily paying rent (or mortgage) and utility bills. Whether employment increases or decreases, spending rarely increases or collapses significantly.

To understand this, put yourself in the shoes of a CEO. As the recession begins to weigh on sales, executives cut costs. Reduce inventory, scale back bonuses, travel, and perks, cancel marketing campaigns, and cancel expansion plans. But what about layoffs? It's a horrible last resort that CEOs hate. Layoffs create bad publicity and disrupt company culture and workers' lives. And when the situation finally improves, replacing experienced help will be difficult and costly.

Similarly, companies don't hire the first time their performance improves. They want sustained sales growth to avoid being boomeranged by a false dawn. The fabled fear of a “jobs-less recovery” that is common at the beginning of an economic recovery consistently misunderstands this point. Work always follows growth, never guides growth.

What is an example? Although the 2007-2009 recession officially ended in June 2009, the unemployment rate has since peaked at 10% in October. Still, the unemployment rate only went down because demoralized workers stopped looking for work, and they weren't technically counted as unemployed (that's how it was calculated). Salaries did not bottom out until February 2010.

When the unemployment rate peaked, the S&P 500 index was already up 55.3%. When did salary increases resume? 66.8%! The unemployment rate remained above 9% until September 2011, but stock prices rose throughout that time.

Similarly, after the March-November 2001 recession, unemployment peaked 17 months later in June 2003. Employment numbers did not bottom out until August. By then, the bull market was raging and the recession was a distant memory.

In the flash of 2020, even amid lockdown-induced economic contraction, stock prices bottomed out in March, unemployment peaked in April, and net employment resumed in May.

First, stocks. Next is the economy. Work is final. everytime.

Employment data tells us how the economy has fared in the past, not where it is headed. The last few years have taken us to strange places. Yes, I mean the new coronavirus. The lockdown wreaked havoc on the economy, but it also affected the metrics by which it is measured. Including getting a job.

By September, more than half of the 0.4 percentage point rise in the unemployment rate in 2024 will be due to labor force growth. do not have Many of the layoffs are caused by people who left the workforce and returned to work amid a mental breakdown due to the coronavirus pandemic. Employment is growing, but the workforce is growing even more. The same goes for rising unemployment rates in Europe, Canada, and many other regions.

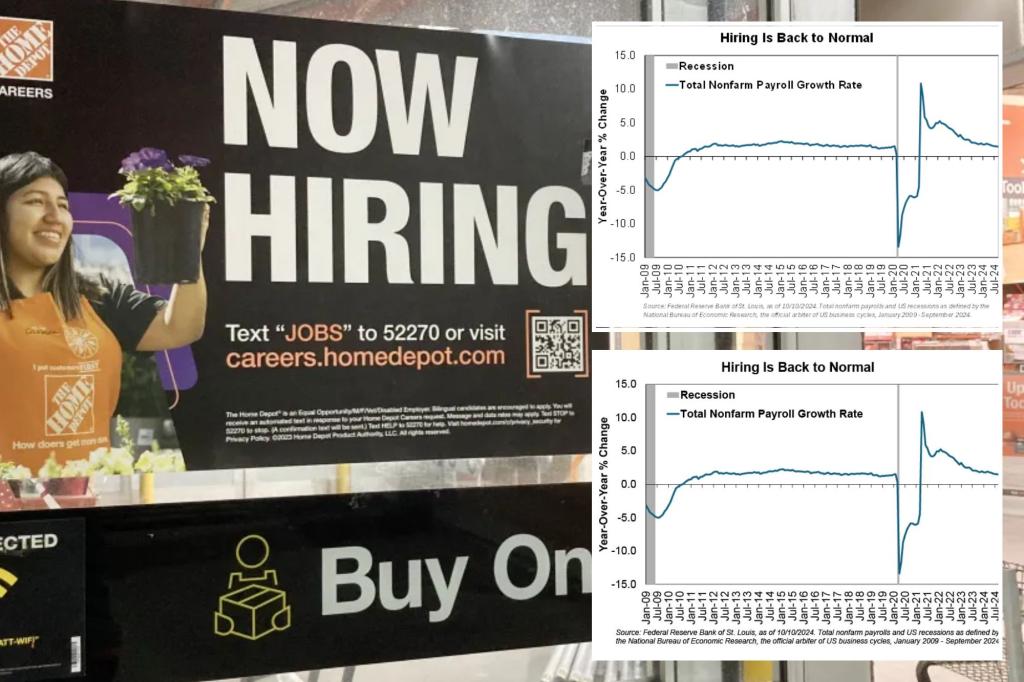

Yes, employment slowed after 2021 and rapidly increased to normal pre-pandemic employment rates in 2022. Consider 2009-2020. After employment numbers bottomed out in mid-2010, year-over-year growth has rebounded to between 1.2% and 2.3%. September's 1.5% year-on-year comparison is exactly at that level.

We are having a hard time recognizing that employment data has returned to normal post-COVID-19. But it's not something to fear or rejoice. Employment data will only catch up.

Ken Fisher is the founder and executive chairman of Fisher Investments, a New York Times bestselling author, and a regular columnist in 21 countries around the world.