Despite concerns, credit card delinquency rates show improvement

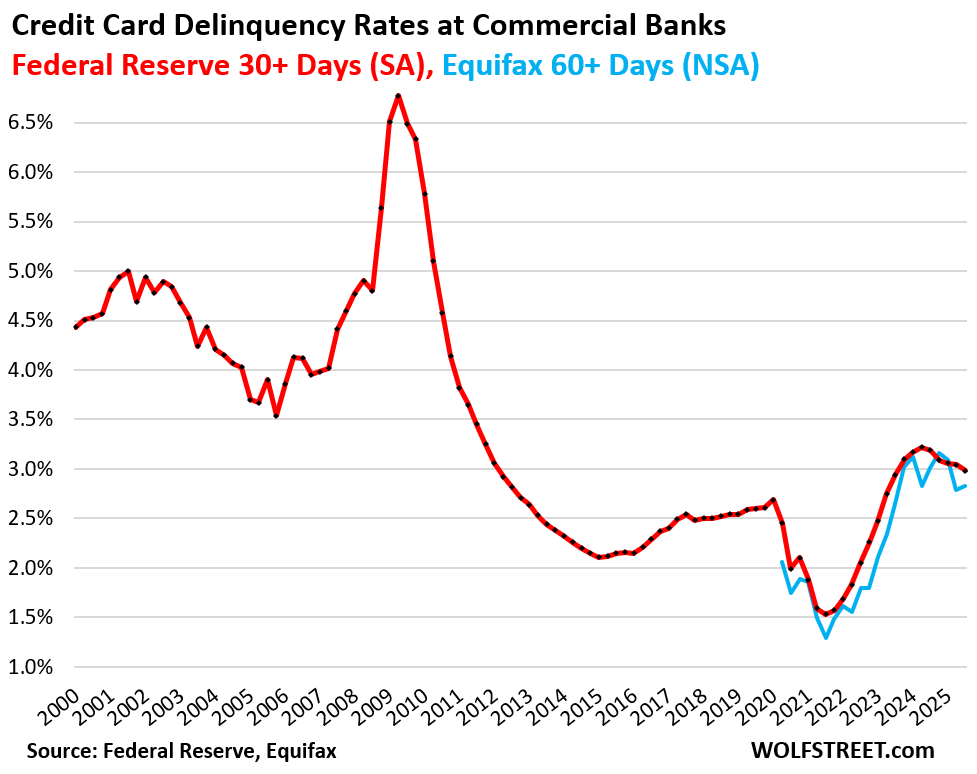

During the period of easy money, credit card delinquency rates dropped significantly. However, after that era came to a close, rates spiked, peaking in early 2024 before beginning to decline again.

Delinquency rate over 30 days The Federal Reserve reported today that outstanding credit card balances across all commercial banks have changed, with the seasonally adjusted rate dropping to 2.98% at the close of the third quarter. This marks the lowest level since the second quarter of 2023 and is down from 3.19% the previous year. This data encompasses cards held by subprime borrowers.

Delinquency rate over 60 days According to Equifax, the non-seasonally adjusted rate fell slightly to 3.02% year-over-year, down from 3.23% in Q3 2024.

For prime consumers Fitch Ratings provided data showing that the serious delinquency rate for well-rated cardholders (60+ days late) dropped to 0.91%, the lowest level recorded outside the easy money period.

This situation has manifested what some have dubbed the “frying pan” pattern. It illustrates how delinquency rates dipped during the easy money phase and then returned to just below pre-pandemic levels, forming a recognizable shape on various graphs tracking delinquencies and foreclosures.

Credit card balances: an indicator of spending, not merely debt In the third quarter, credit card balances surged by $67 billion year-over-year, reaching $1.23 trillion. This rise is driven by increased personal spending and inflation, as reported by the New York Fed’s Household Debt and Credit Report.

It’s important to note that credit card balances reflect spending habits rather than borrowing per se. When we talk about balances, we refer to what is owed before any payments. Credit cards have largely taken over as the primary method of payment for consumers in the U.S., often being used for everything from parking meters to business travel expenses, which are usually reimbursed by employers. Annually, approximately $6 trillion is charged to credit cards, with most balances being paid off without accruing interest.

The focus here is really on spending increases fueled by rising prices, rather than borrowing more. The month-end balances don’t account for interest but indicate the actual borrowed amount.

“Other” consumer loans, including personal loans and buy now pay later (BNPL) schemes, saw a slight increase of 0.7% year-on-year, totaling $550 billion, which is quite modest considering the overall inflation rates. Over the past two decades, this category has grown very slowly, even as population and income have increased.

What’s the actual cost? The combined credit card and other consumer debts rose by $71 billion year-over-year, totalling $1.78 trillion. The debt-to-income ratio is often used to assess how well borrowers can manage debt burdens. It gauges how much debt a consumer holds compared to their income.

For consumers, the best measure is disposable income, which excludes capital gains. This includes wages, salaries, and other forms of income while also factoring in taxes. Since the Bureau of Economic Analysis has not updated disposable income figures for September due to a government shutdown, they relied on earlier months to estimate the figure for September.

The balance of credit cards and other consumer loans as a percentage of disposable income slightly decreased to 7.7%. This change happened because disposable income increased at a slightly higher rate than the debt balances: 4.7% versus 4.1%.

Credit limits and available credit Banks earn revenue from swipe fees whenever credit cards are used for purchases. Thus, they are incentivizing customers to open new accounts by offering rewards like cashback or loyalty points.

Current total credit limits stand at $5.3 trillion, which is rising faster than the balances owed. This creates a record amount of unused credit, now totaling $4.1 trillion.

Third-party collections The rate of consumers engaged in third-party collections has remained historically low, decreasing from over 14% a decade ago to just 4.9% in the latest quarter.

Third-party collections affect credit histories when lenders report delinquent loans to credit bureaus after selling them to collection agencies for a fraction of the original value. This data comes from a partnership with Equifax that anonymized consumer information.

This wraps up our analysis of consumer debt and credit. If you’re interested in exploring various facets of consumer debt, including auto loans and mortgages, there are comprehensive reports available.