Market movements:

- WTI crude oil fell $1.20 to $67.10.

- US 10-year bond yield fell 2.9bps to 4.15%

- Bitcoin rises by $2,544 to $101,540

- Gold rises $1 to $2,633

- S&P500 rose 0.2%

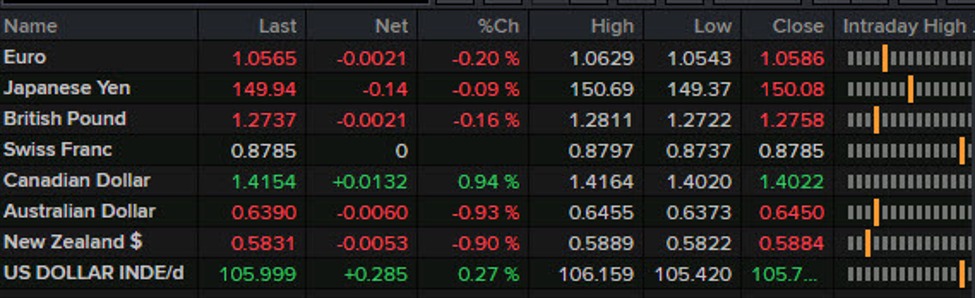

- Japanese yen leads, Australian dollar lags

This week's theme has been that it's difficult to connect market movements with economic news and data, and today was no exception. The jobs report was marginally dovish, but it was borne out by odds rising from 70% to 85% in December and a 5bps drop in two-year bond yields. Initially, the dollar weakened, as you might expect. There were similar movements elsewhere, with USD/JPY falling from 150.50 to 149.50 and EUR/SUD rising from 1.585 to 1.0625.

However, about an hour after the announcement, currency movements began to reverse (bond movements did not), euro movements completely disappeared, and yen movements were halved. Some may point to UMich's data or Bowman's comments, but that's an overstatement.

Some of that could go into USD-denominated assets such as mega-cap tech stocks that have hit new highs, but that is unlikely. I struggle to offer any other insight other than repeating that the US dollar will still be the cleanest and dirtiest shirt in 2025.

Dirty shirts in this day and age are commodity currency, and that's not good for global growth. The Canadian dollar had a good excuse, as everything beneath the surface of the jobs report was weak, with the unemployment rate rising to its highest level since 2016. It's clear that high interest rates are hurting, we need 50bps next week and the market is currently pricing in the Canadian dollar. 83%. It would be the lowest weekly closing price since 2020, close to the four-year low set in November.

What was less expected was the poor performance of the Australian and New Zealand dollars on Friday. While sympathy trading could be in play, today's weakness comes after Chinese stocks rose +1% on optimism about stimulus at next week's labor conference, and copper prices has also improved.

In any case, the Australian and New Zealand dollars are both near their lows this year, and the RBA was the first to rise on November 10th (no rate cut expected), so it's worth noting.

Have a great weekend!