Will the AI Bubble Burst the Bull Market?

There’s a rising concern about whether the current AI boom might lead to a significant market downturn, echoing sentiments from the year 2000. Some critics argue that the rapid rise in AI stocks is reminiscent of previous market bubbles.

Sure, market sentiment has definitely shifted since 2023. But, it’s worth noting that this surge in AI stocks seems to be backed by solid fundamentals, unlike the internet bubble back in the late ’90s.

Here’s a little insight about bubbles: When a lot of people are talking about a market bubble, it often means we might not be in one. True bubbles are quite rare and usually go unnoticed until they’re about to burst.

There’s indeed plenty of excitement around AI, and yes, the stocks that stand to gain from this excitement have skyrocketed. For instance, U.S. tech stocks have seen a 27% rise this year alone, with gains of 78% over two years and 160% over three. Companies have invested heavily—hundreds of billions—into AI this year, building infrastructure and acquiring necessary technology. Almost 90% of businesses are now making use of AI in some form, which is encouraging.

But this growth also sparks concerns about potential excess. Detractors point to high capital expenses and uncertainties regarding sustainable profit models in AI. Some analysts insist that while AI holds transformative potential, it’s crucial to first remove overvalued stocks from the market.

Interestingly, third-quarter earnings have shown less negative impact from current economic conditions than some anticipated. And then there’s the tech industry’s recent volatility—has the tide really turned? You’d think we’re on the brink of a dystopian scenario, akin to something out of a sci-fi movie. It’s wild how perspectives can shift, right?

Some skeptics worry about various AI firms issuing bonds, but it’s important to put things in perspective. Many large companies possess far more cash than debt. Yet, there are concerns about what some call circular financing, where suppliers invest in AI firms and subsequently use the returns to buy from them. It seems a bit shaky, almost like building on sand.

But really, that only represents a small percentage—less than 4%—of the companies pouring resources into AI, which isn’t too alarming.

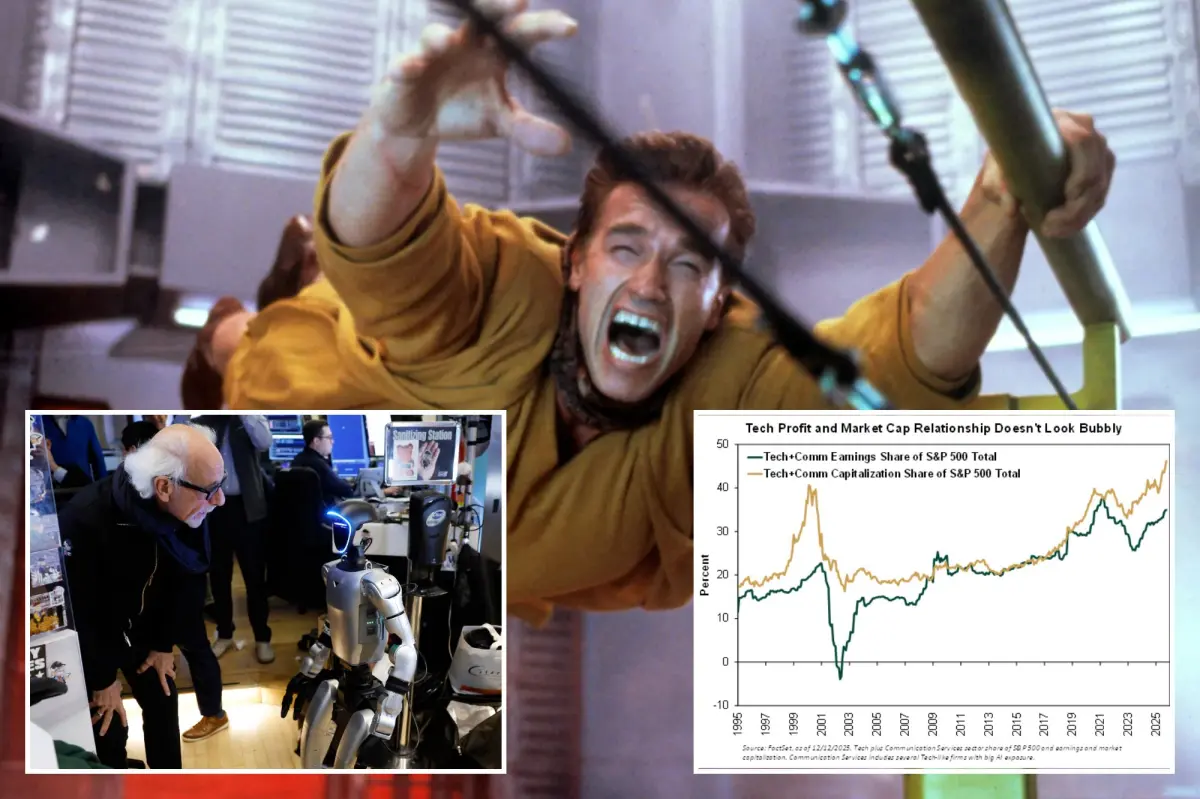

Let’s focus on the evidence. Most of the AI stocks driving the current hype belong to substantial companies that are also seeing rising profits. It’s not at all comparable to the year 2000. The truth is these companies are growing through available cash flow rather than accruing new debt or equity, marking a distinct difference from that era. Their revenues are consistently climbing, and AI innovations aren’t squeezing profit margins.

If there are any parallels to the past, it’s mainly technology, a narrative about the future, and high valuations. Back then, a flashy idea often got funded just because it had a “.com” at the end, but many of those investments didn’t hold up, leading to a dramatic collapse. There’s a myth out there—valuations don’t always predict stock performance. Tech stocks can swing wildly, and bubbles result in failures.

I remember the year 2000 distinctly. With nearly three decades in the field, you start to notice patterns. Often labeled a “perpetual bull,” I’d say I’m more of a cautious optimist. Historically, stocks tend to rise in around three out of four periods. In fact, I was among the few who anticipated the dot-com bubble burst, positioning my company in cash just ahead of that. It’s funny—back then, those warnings fell on deaf ears.

Now, those who are warning about a bubble are being celebrated as wise seers. That, in itself, is a sign of market optimism.

And as for timing? You might recall Alan Greenspan’s “irrational exuberance” comment from 1996. Surprisingly, the S&P 500 kept climbing, gaining an additional 116% before peaking in 2000—that’s quite a jump. U.S. tech stocks surged by another 384%.

So, perhaps it’s time to embrace the current enthusiasm. It’s just another element adding to the complexity of this bull market. And stay tuned; my predictions for 2026 will be interesting, especially considering that it doesn’t necessarily resemble 1997-2000.