Currently, the Japanese yen is close to its lowest point against the US dollar since 2024. Interestingly, even though the yen has depreciated, on a trade-weighted basis, it’s not as weak as it was back then. So, in some sense, it’s already cheaper. There’s some talk about potential public intervention to halt this slide, coming from Japan’s Ministry of Finance. However, past experiences suggest any such actions might not yield the desired results. The primary issue is that the market is pushing for higher interest rates, yet they remain elevated. It’s somewhat frustrating since the existing rates don’t sufficiently reward investors for the risks they perceive.

This situation is tricky—while rising interest rates might help stabilize the yen, they could just as easily lead Japan into a fiscal crisis. Essentially, Japan feels trapped.

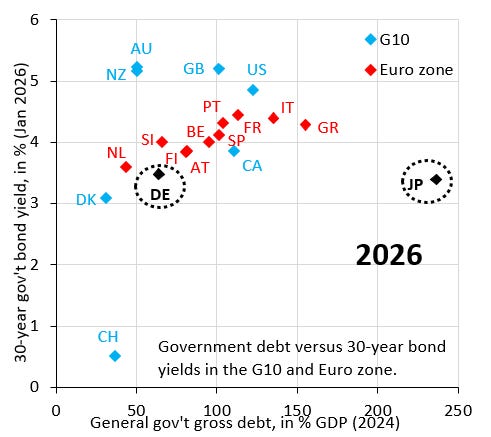

There’s a schematic I find useful, which illustrates the dilemma. The horizontal axis shows total government debt, while the vertical represents the 30-year government bond yield. Japan’s yields are indeed rising, but they’re still low relative to its massive debt. For comparison, Germany’s debt is lower, yet its bond yields are slightly higher than Japan’s. The ongoing bond purchases by the Bank of Japan are keeping yields from rising to where they likely should be. As long as these yields stay artificially low, the yen will continue to face pressure, no matter what steps are taken officially.

However, letting yields increase is like opening a can of worms—it’s risky and could lead to a fiscal crisis. Since it’s uncertain how high yields could go, Japan cannot simply relax its bond-buying strategy entirely. Yet, there is a potential solution here. As noted previously, Japan’s net debt is significantly lower than its total debt because the government has various assets. A feasible approach could involve selling off some of these assets to tackle the overall government debt problem.

To put things into perspective, Japan’s net debt stands at around 130% of GDP, while gross debt hovers near 240%. Sure, some assets are not easily liquidated and may take time to sell, but even a small step in this direction could significantly bolster the yen. That’s the direction Japan ought to consider. And since this wouldn’t count as an official foreign exchange intervention, it likely wouldn’t bear the same ineffectiveness we’ve seen before.