As a large portion of Americans digs into their savings to tackle rising expenses and mounting economic pressures, there’s potential to enhance long-term financial stability. This varies significantly from state to state.

Why is it important?

Many Americans are experiencing financial instability. Some even worry more about running out of money than about their mortality. Meanwhile, those anxious over cash flow and the stock market have started to engage with their retirement accounts more fervently than before.

What do you know

The economic anxiety felt by many stems from several factors, including recessions, inflation, rising healthcare costs, as well as soaring grocery and gas prices. There are also concerns about tariffs and possible cuts to Social Security and Medicaid.

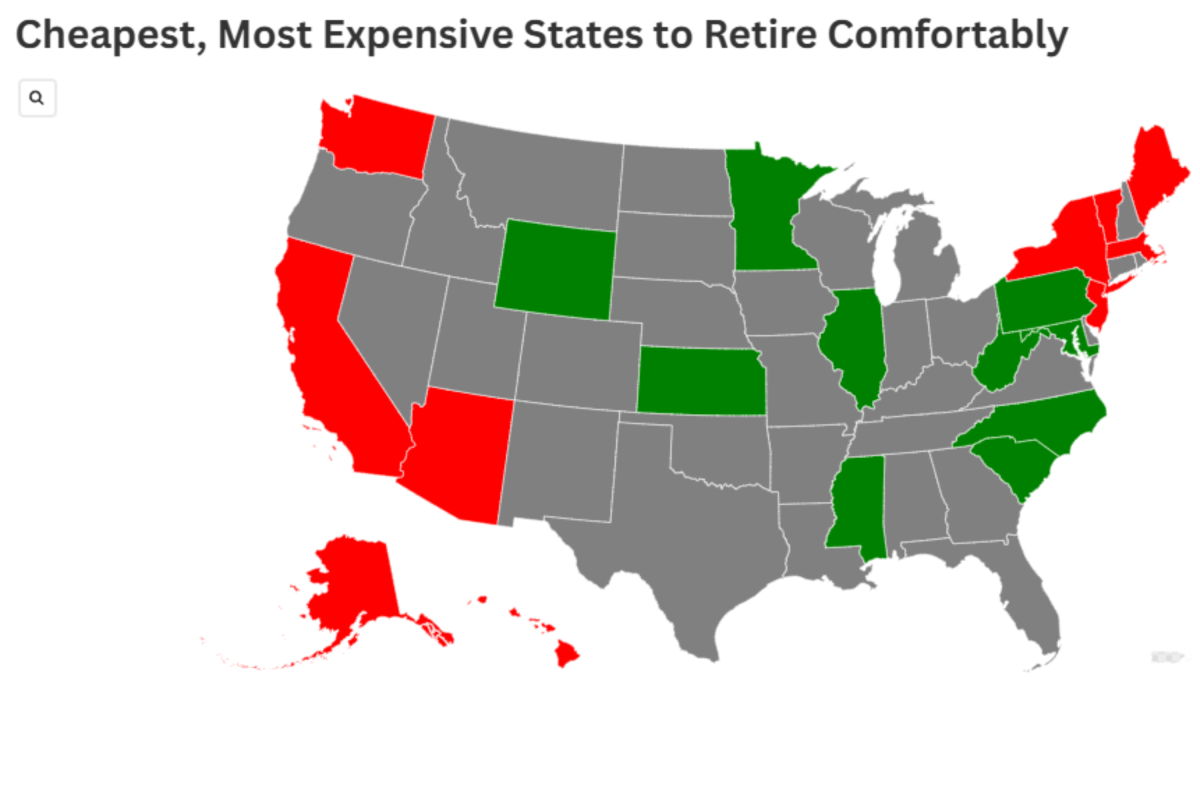

Kiplinger, a well-known source for business forecasting and personal finance tips, has released a list of states where you can stretch your savings the furthest during retirement.

The ten states with the lowest savings requirements for retirement are:

- West Virginia – $712,913

- Kansas – $741,455

- Mississippi – $753,472

- Pennsylvania – $864,633

- South Carolina – $869,140

- Minnesota – $870,642

- Wyoming – $872,144

- Illinois – $873,646

- North Carolina – $905,192

- Maryland – $924,720

On the other hand, the ten most expensive states for retirement savings are:

- Hawaii – $2,212,084

- Massachusetts – $1,645,764

- California – $1,612,716

- Alaska – $1,292,753

- New York – $1,292,753

- New Jersey – $1,163,566

- Vermont – $1,153,051

- Washington – $1,145,540

- Main – $1,144,038

- Arizona – $1,133,522

A recent AARP study indicates that about 20% of adults over the age of 50 lack retirement savings, and around 61% are concerned they won’t have enough to retire comfortably.

Interestingly, Americans are significantly more inclined to save for retirement when they have access to employer-sponsored plans. Yet, AARP suggests that nearly 57 million individuals lack such access.

According to John Tamny, founder and president of Parkview Institute, we’re at a “critical juncture” when it comes to fiscal policy, a thought echoed across multiple administrations in Washington, DC. He mentioned that the Trump administration has undertaken essential steps towards improving long-term fiscal health by tackling systemic issues, modifying international trade relationships, and implementing housing reforms aimed at boosting supply-side incentives.

“There’s a lot of tension,” Tamny noted, highlighting concerns over tariffs, housing costs, and qualification criteria for spending. “But these aren’t new problems. What’s unusual is the readiness to confront them directly. That suggests a need to adjust retirement planning to focus on resilience rather than fear.”

“In our current environment, preparing for retirement needs a flexible approach. It should include investments that guard against inflation, adjustable expectations around retirement age, and a variety of income sources. While Social Security may witness changes, being proactive now could safeguard the program’s future,” he added.

A survey conducted by Vanguard looked at data from nearly 5 million retirement account holders and discovered that a record 4.8% struggled with 401(k) withdrawals in 2024, compared to 3.6% in 2023.

Tamny also emphasized the impact of geography on how different age groups and financial standings influence retirement perspectives. For those in high-cost locales, planning needs to be particularly meticulous. This includes residents in coastal cities like California and Florida, where living expenses and climate-related issues complicate financial planning.

“For people in high-cost states, it’s essential to think critically and strategically about where you live,” he suggested. “Given the rise of remote work and more flexible benefits, moving is more feasible than ever.”

“Retirement security isn’t just about how much you save anymore; it’s also about how wisely you spend what you have saved.”