Jamie McGeever

(Reuters) – Future outlook for Asian markets.

Investors entered the new week in optimistic spirit after last Friday’s U.S. jobs report put a “soft landing” scenario on track, driving down the dollar and bond yields and fuelling a relentless “risk-on” rally in stocks.

Most of the world’s major stock markets are at all-time or multi-year highs and nothing is likely to destabilize them anytime soon.

Profit taking, end-of-quarter positioning, concerns about valuations and market concentration, and political and policy uncertainty have all played a role recently, but the overwhelming “buy low” sentiment has kept stock price declines shallow and short-lived.

European politics could have some influence on early Asian trading on Monday. France is set to have a hung parliament after Sunday’s general election saw a surprising upset in which a left-wing coalition took the top spot over the far-right, making it impossible for the far-right euroskeptic National Rally to govern.

Asia is off to a strong start, with Japanese shares hitting a new record of 41,100 points on Friday, up about 7% in just two weeks, and the MSCI Emerging Markets Index hitting a two-year high.

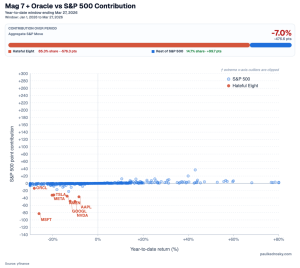

More broadly, the MSCI World and Nasdaq all hit record highs last week, while euro zone stocks hit a 23-year high last month. The MSCI 100 hit an all-time high in May.

The Asia-Pacific schedule is light on Monday, with attention focused on Japan’s bank lending, trade and current account balance and overtime pay figures. Philippine central bank Governor Eli Remolona and Treasury Secretary Ralph Recto will also speak at a business forum on Monday.

Overtime pay in Japan isn’t usually considered a top tier indicator, but this month it’s worth watching.

A recent trade union survey showed that companies are offering an average wage increase of 5.1 percent this year, the biggest increase in 33 years and well above the rate of inflation, which is currently hovering around 2 percent. But Friday’s figures showed that rising prices continue to squeeze consumer purchasing power, causing household spending to fall sharply in May.

That’s a headache for policymakers at the Bank of Japan, who want to raise interest rates and are prioritizing wage increases but are concerned about the impact on an economy that is far from buoyant.

Looking ahead, the most market-sensitive events in Asia this week are likely to be central bank policy meetings in New Zealand, South Korea and Malaysia, as well as China’s producer and consumer price inflation rates.

Globally, the drivers of markets are expected to be the US Consumer Price Index (CPI) on Thursday and two days of congressional testimony from Federal Reserve Chairman Jerome Powell scheduled for Tuesday and Wednesday.

Here are some key developments that could give further direction to the market on Monday:

– Japan’s wage growth rate (May)

– Japan’s current account balance (May)

– French General Elections