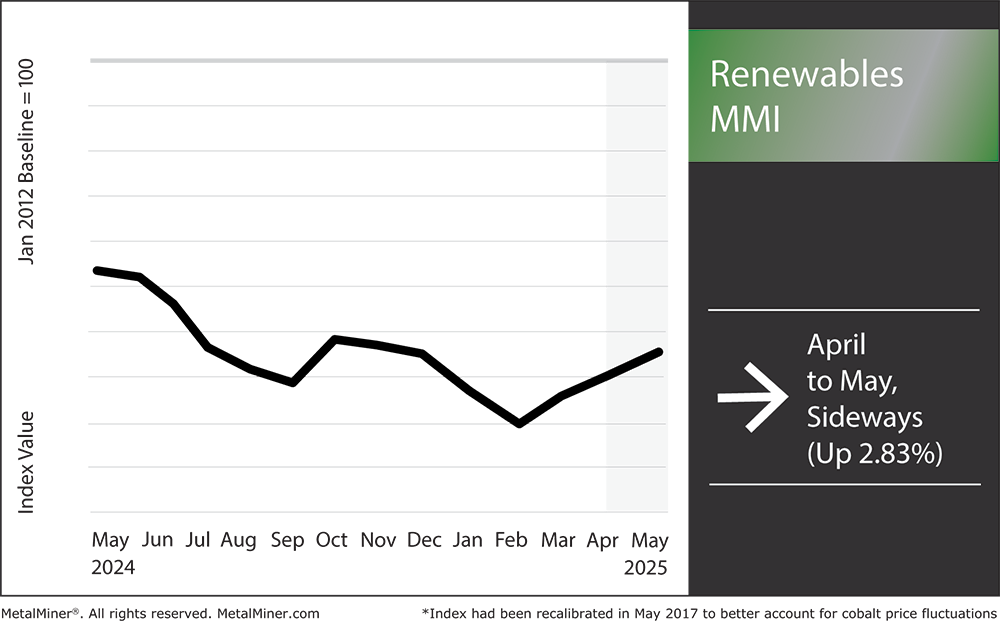

Renewable Energy MMI recently experienced a mild increase of just 2.83%. Over the past few weeks, there have been notable price fluctuations in various metals like copper, steel, lithium, and cobalt, largely driven by U.S. companies eager to secure materials ahead of potential customs duties. For instance, U.S. copper prices surged in the early part of the year as buyers acted quickly in anticipation of possible import restrictions, only to see a drop in early April when China responded.

Trading data indicates that copper futures fell by 14% within a week, with prices on the London Metal Exchange hovering around $9,000 per ton. This volatility highlights the typical dynamics of imported arbitrage. U.S. prices are currently about $756 per ton higher than the global benchmark. As the reality of the market settles in, it’s clear that copper’s short-term outlook has been declining since its peak in March, which puts pressure on buyers.

In the steel sector, the situation appears more stable. Earlier concerns about tariffs drove hot-rolled coil prices to multi-year highs, but by early April, prices started to stabilize. Reports suggest that while bids for steel plates have risen, prices for hot-rolled coils have softened since their March highs, around $920. Additionally, domestic factory lead times have shortened since the rush in early March, indicating a possible dip in short-term demand.

Despite these adjustments, American steelmakers are still in a tight spot. The tariffs announced on April 4 had already kept protective measures on items like steel and aluminum, which maintain a 25% tax rate.

When it comes to battery metals, there’s a sense of mixed narratives. After a spike last year, lithium prices are currently facing intense pressure due to oversupply, driven by increased production and high inventory levels. S&P Global suggests that the influx from new mining projects and the reopening of operations in China could lead to further declines in lithium carbonate and hydroxide prices through Q1.

Looking ahead, S&P predicts continuous downward pressure as we approach the second quarter of 2025. This has dropped lithium prices on the Asian index to nearly a three-year low, raising questions on whether this is a mere correction or a longer-term shift.

Cobalt also displayed volatility, falling to its lowest in nine years at the beginning of the year. Following an unexpected lifting of a four-month export suspension in the Democratic Republic of the Congo, cobalt prices surged roughly 40% through March, concluding Q1 at about $34,000 per ton. However, the market remains on edge as shipments from the Congo are expected to resume, and many traders doubt that price increases will hold.

Amid these trends, policy changes add another layer of complexity, especially with the 2024 Trump campaign outlining a broad tariff plan aimed at restructuring the metals market. An official fact sheet from April mentioned a new 10% levy on all imports, set to take effect on April 5. This has raised concerns among many regarding its potential impact on metal pricing, although the duties have been postponed until July. If implemented, these restrictions could introduce short-term volatility into the market.

While Trump’s tariffs have mostly avoided copper, the looming threat of a trade war could affect the supply chains for battery metals such as lithium and cobalt, which are critical for clean energy projects and electric vehicles. Currently, copper and steel prices are stable despite the looming customs gathering, while lithium and cobalt appear to be adjusting to these broader supply fluctuations.

Meanwhile, grain-oriented electric steel saw a rise of 10.17% this past month. Prices for this specific type of steel have shifted from being relatively flat to showing some increase lately. Industry indices suggest that North American prices may reach approximately $3.87 per kilo in May, reflecting a modest monthly rise of 0.5%. With new U.S. factories coming online and a solid stream of electric steel orders, there’s potential for continued stability through the summer.

Demand for grain-oriented steel is climbing due to efficiency needs, but production bottlenecks indicate possible import interruptions affecting transformers. Buyers and planners are closely monitoring the proposed trade measures.