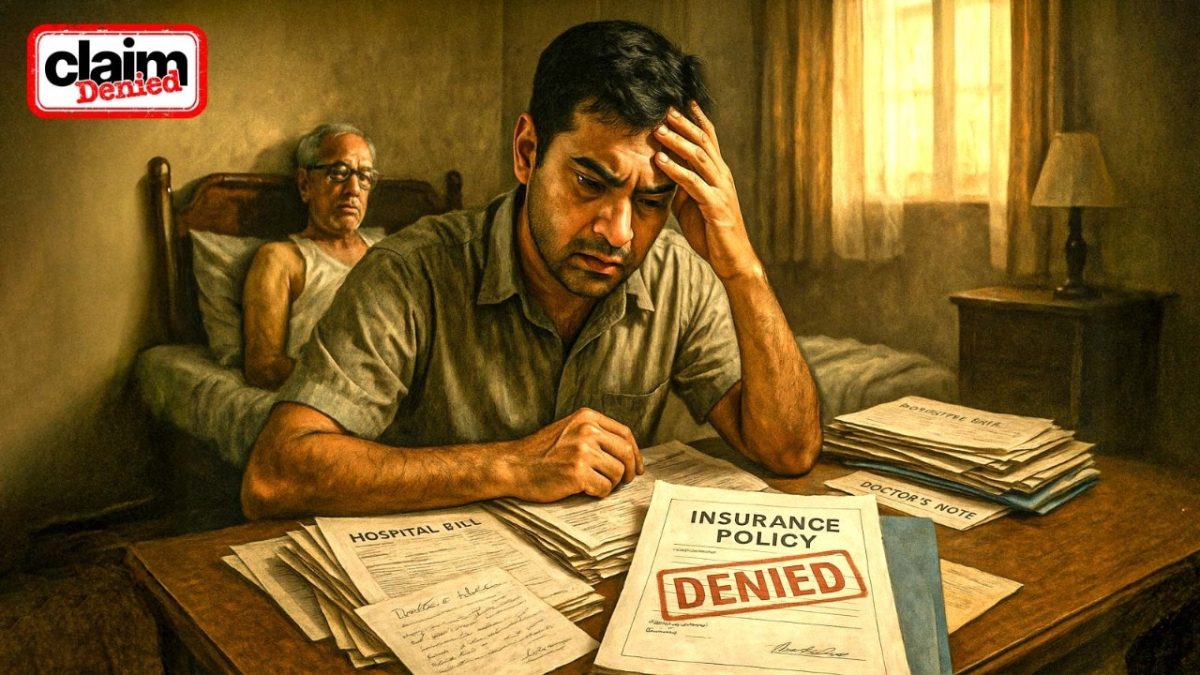

Family’s Health Insurance Ordeal

In April 2024, Vipin Vishnu Ajayan’s father suffered from severe chest pain, and the family hoped their new health insurance would cover the treatment. They had purchased a plan months earlier that promised Rs 5 lakh coverage for both parents, costing about Rs 32,000 annually.

What should have been a straightforward claim turned into a lengthy struggle filled with denials and poor communication.

After the initial tests showed serious cardiac issues, doctors suggested a stent procedure. The family expected cashless treatment at a Network Hospital, but the insurance company denied the claim, citing insufficient documentation and suggested applying for a refund later.

As the only earning family member, Vipin had to pay the hospital bills upfront.

Claim Denials and Frustration

In a statement to Indiatoday.in, Star Health mentioned that the claims were often rejected due to non-disclosure of pre-existing conditions during policy purchase. They argued that full transparency is vital for fair pricing and proper coverage.

In this specific case, they flagged medical instability shortly after the policy was bought. “A claim was made within three months for a 60-year-old man with significant coronary artery disease, which is medically improbable given the short history,” the company stated, leading to denials of both cashless claims and refund requests.

Vipin firmly disagrees with this assessment. He pointed out that all documents did not confirm any prior heart issues, including letters from cardiologists. Yet, claims continued to be dismissed. “They kept asking for more paperwork, and their replies were just automated denials. I mean, a heart attack doesn’t exactly announce itself,” he said.

Vipin also expressed confusion over the insurer settling the amount before an Ombudsman hearing without asking for further documentation, calling it contradictory. “It’s strange that StarHealth would want to settle before the hearing without additional details,” he commented.

He is convinced that the insurance company only acted after persistent follow-ups. “Star Health seemed to intentionally slow down the process, only responding due to my relentless pursuit. It has really made me question their honesty through this whole ordeal.” He noted inconsistencies during the policy purchase, such as being asked about his parents’ health, to which he responded truthfully. If that information was accepted then, why was it doubted later?

Vipin raised concerns about the company’s focus on policy sales, seemingly indifferent to customer welfare. “Once the policies are sold, families face unnecessary obstacles and frustration in accessing services they’ve already paid for,” he added.

Ombudsman Intervention

Frustrated, Vipin reached out to the Insurance Ombudsman in November 2024. Prior to the hearing, the insurer offered a partial settlement that included interest from July 3, 2024, totaling Rs 1,03,859.

However, Vipin remained dissatisfied, especially after learning that his father had been removed from the policy without any notification in September 2024. “Despite my efforts and complaints, StarHealth did not adequately reinstate my father’s coverage, and their response even misrepresented my mother’s status,” he explained.

StarHealth stated that they complied with the Ombudsman’s directions for recovery and claim processing but maintained their medical views. “We believe it’s unlikely such a condition could develop in that short timeframe,” they reiterated.

Vipin criticized the company’s customer service. “Calls often went unanswered, and sometimes the sales agents would block me. We had to escalate matters just to get basic things done. Even my experience with the Ombudsman felt dismissive,” he said.

Advice for Policyholders

Abhishek Kumar, founder of Sahajmoney, mentioned that cases like Vipin’s are not uncommon. He recommends keeping thorough documentation, seeking pre-authorization for cashless claims, and asking for written explanations if a claim is denied.

“If a claim is denied, escalate the issue through the company’s complaint channels and Nodal officer. If unresolved after 30 days, use the Bima Bharosa portal and consider approaching the Insurance Ombudsman. As a last resort, the consumer court is an option,” he suggested.

Regarding policy cancellations, he clarified that insurers must give at least seven days’ notice if fraud or misrepresentation is established. Affected policyholders can demand reinstatement by filing complaints with the insurer.

Kumar cautioned about real-world delays and noted that while regulatory bodies like IRDAI aim to improve service standards, often the resolution still takes longer than expected.

For Vipin and his family, this entire experience has brought about significant stress and financial strain. What should have been a safety net during a medical emergency turned into a year-long battle for their patience, resolve, and trust in the system.