Wall Street’s “Magnificent Seven” Faces Challenges in 2023

In 2023, analyst Michael Hartnett referred to a select group of U.S. companies as the “Magnificent Seven” due to their significant presence in the tech sector and their ability to outpace rivals in revenue and profits. This group includes:

-

Nvidia

-

Apple

-

Alphabet (Google)

-

Microsoft

-

Amazon

-

Meta Platforms

-

Tesla

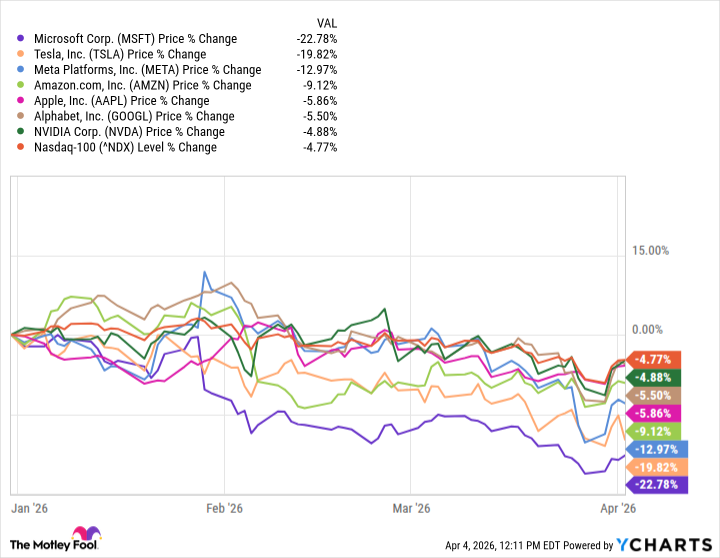

Historically, these companies have yielded better returns than most shares in the market. However, they are currently experiencing an unusual dip in performance. The Magnificent Seven’s average stock price has dropped by 11.5% year-to-date, while the Nasdaq-100 index has decreased by 4.8%, largely due to ongoing geopolitical tensions in the Middle East.

High-growth stocks often experience volatility in uncertain times, but such downturns can also present buying opportunities. Each of the Magnificent Seven has strong reasons for ownership, yet Amazon and Alphabet catch my eye as particularly appealing right now. An investor with $500 to spend could easily buy a share of each. It seems like a smart choice.

Amazon, the forerunner of the e-commerce boom in the late ’90s, derives its largest revenue from its retail platform, Amazon.com. Over the years, it has successfully expanded into areas like streaming services, digital ads, and, notably, cloud computing. This latter sector is where Amazon Web Services (AWS) has established itself as a market leader.

Offering a vast array of services—from simple data storage to intricate software development tools—AWS equips businesses for success in today’s digital landscape, playing a crucial role, especially in its AI initiatives. The platform manages numerous specialized data centers across the globe, supporting businesses in developing and deploying AI technologies.

These data centers utilize specialized AI chips, supplied mainly by Nvidia but also designed by Amazon itself. The latest Trainium2 chip promises a 40% improvement in price performance over rival hardware, with the new Trainium3 chip expected to offer an additional 40% efficiency. By the end of 2025, Amazon anticipates a $244 billion backlog in computing power ordered by cloud clients. Creating its own chips will enable quicker deployment of data centers compared to relying on external suppliers.

By 2025, AWS is projected to achieve $128.7 billion in revenue, with a 24% growth rate in the fourth quarter. This indicates strong AI-driven momentum. AWS also stands out as Amazon’s most profitable division, anticipated to contribute over half of the company’s operating profits in 2025.

Interestingly, Amazon’s stock is projected to decline by 9% in 2026 and has already seen a 17% drop from last year’s peak. The price-to-earnings ratio stands at 29.2, close to its lowest since the company’s IPO nearly three decades ago. In my view, this could be an enticing entry point for long-term investors.

Alphabet serves as the parent company to Google, YouTube, Waymo, and DeepMind, among others. Its Google Cloud platform, a significant competitor to AWS, offers similar services. Google Cloud is also one of Nvidia’s largest customers and has developed its own specialized chip, the Tensor Processing Unit (TPU), which excels in AI applications. Alphabet has utilized its latest Ironwood TPUs to train the cutting-edge Gemini 3 series of large-scale language models, marking a significant milestone in AI.

Over 120,000 companies globally leverage Gemini models through Google Cloud, fueling their own AI software development. This is crucial because increased usage of AI applications on Gemini translates to higher token consumption and, consequently, greater revenue for Google Cloud.

In 2025, Google Cloud achieved record revenues of $58.8 billion, with growth accelerating by 48% in the final quarter of the year. Despite this, Google’s main revenue stream, search, saw a surge in growth as well. New features, such as AI Overview, enhance user experience by merging traditional search methods with AI capabilities, drawing in more advertisers.

As things stand, Alphabet’s stock is trading at a P/E ratio of 27.2, making it more affordable than both Amazon and the Nasdaq-100 Technology Index at 29.3. The recent decline in the market might offer a prime entry point for long-term investors.