I’ve often come across a set of familiar questions regarding market trends. People express concerns about valuations, tariffs, inflation, the independence of the Federal Reserve, and recently, the reliability of BLS data.

However, one question that pops up more than others is about market concentration. I’d like to share why I don’t see this as a critical issue for the ongoing bull market and what it might imply for stocks moving forward.

There’s quite a bit to unpack here—taking a broad view, grounding it in some solid facts, and looking at historical context.

What’s the general situation? The title of this discussion is Magnificent 493.

Many investors focus on identifying companies poised to benefit directly from advancements in artificial intelligence, but that can be a tricky approach. History shows that thousands of firms flock to the latest technology during each wave of innovation. Some may thrive, while many falter. Yet, the biggest winners tend to be these massive beneficiaries—customers.

Consider the countless companies that produced personal computers in the ’80s and ’90s, or the multitude of American firms that entered the automotive sector. One well-known illustration is from the 1990s Internet boom with all its dot-com startups. It’s easy to overlook names like Juniper Networks or pets.com.1

Despite the chaos of the 2000 dot-com crash, their collective influence was substantial.

When we think of internet firms, we typically picture a small facet of the economy dedicated to certain web technologies. But really, every company today can be considered an internet company in some form. Emails, websites—these are now staples in our working lives. We share content online, hold meetings via Zoom or Google Meet, and track compliance through digital channels.

What company, in this day and age, doesn’t utilize some form of internet technology?

Now, let’s apply that same thinking to the emerging field of artificial intelligence. Companies that employ AI thoughtfully are seeing gains in efficiency, productivity, and profitability.

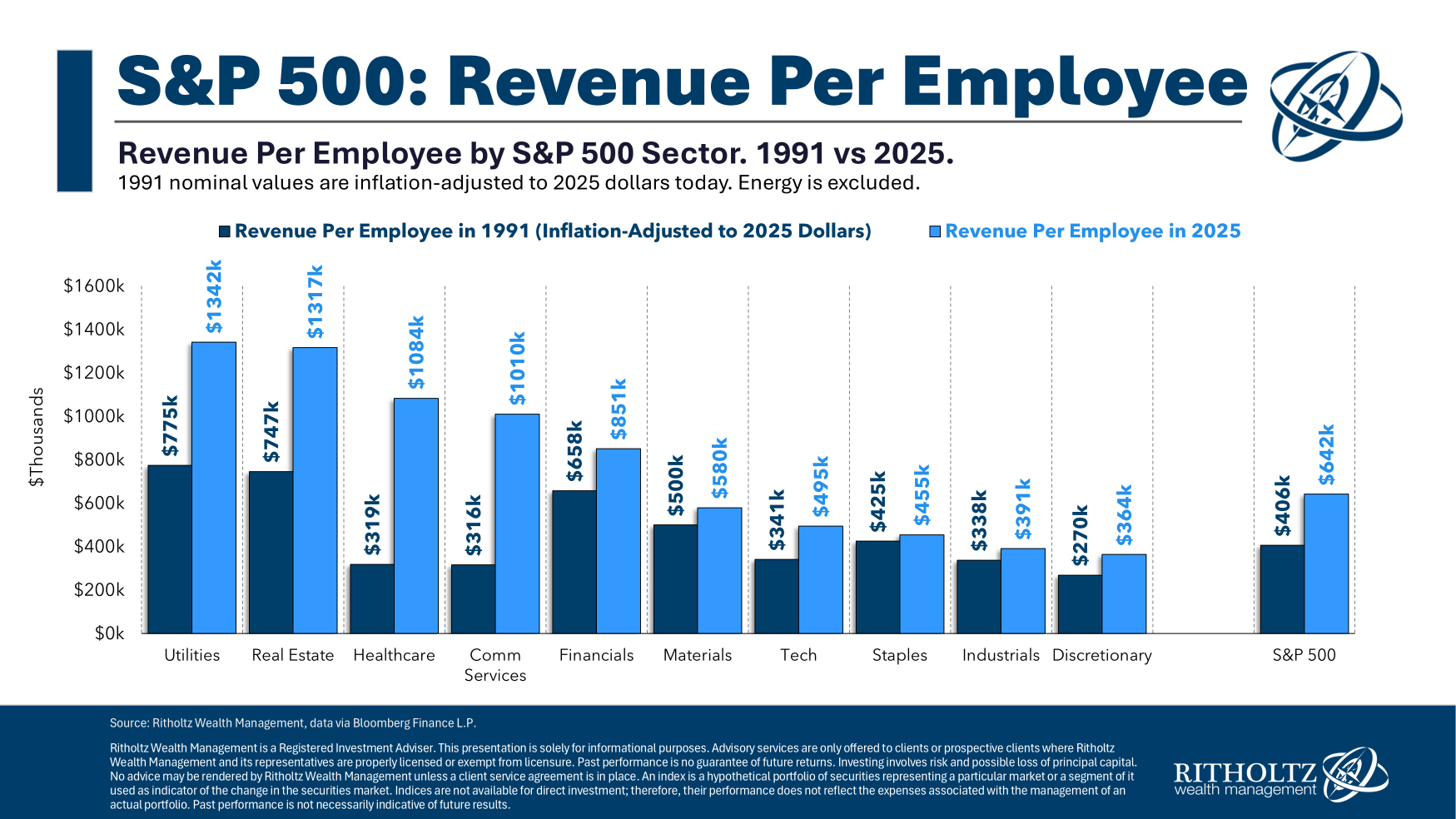

If you take a look at the chart mentioned, it illustrates the revenue per employee from 1991 to 2025 (adjusted for inflation). This span shows a notable rise in technology adoption—encompassing computers, the Internet, mobile devices, applications, and software. Consequently, corporate revenue per employee has steadily increased over time.

This indicates the successful assimilation of innovation. And, importantly, we’re still in the early stages of AI development.

Some of you might be thinking, “Okay, but what about the issue of valuation?” Let’s dive into that. While there are valid concerns about the massive concentration in the S&P 500’s “epic seven,” I find myself more interested in how companies throughout the S&P 500, Russell 2000, and Wilshire 5000 stack up in comparison. At least, that’s how I view it from my bird’s-eye perspective. Let’s take a closer look at what’s unfolding.

My colleagues at Bloomberg, Eric Baltunas and Brean Dougherty, highlighted an interesting angle:

The “epic seven” might actually be closer to an epic seventy. They may have their roots in the “epic seven,” but they act more like a broad collective of seventy, having acquired over 800 companies and expanded into various sectors. They’re growing organically, functioning effectively as a highly technical conglomerate.

Sam Ro elaborated on this trend:

“Nvidia, Microsoft, Apple, Alphabet, Amazon, Meta Platforms, and Tesla—these trillion-dollar firms known as ‘The Magnificent Seven’ make up nearly one-third of the S&P 500’s market capitalization. This level of concentration raises concerns for some. What if demand for one or more dwindles, leading investors to abandon their shares?”

My favorite rebuttal to this worry is that these seven companies effectively operate as seven separate enterprises.

Now, let’s reflect on what historical data reveals regarding concentration.

David Marlin from Marlin Capital points out that this “magnificent seven,” accounting for 35% of the S&P 500, isn’t unprecedented. Back in 1881, railways made up 63% of the market, and in the ’70s, well before passive indexing came to fruition, the “nifty fifty” represented over 40% of the S&P 500.

Every market cycle has had contributors, not detractors. If you’re searching for reasons to be cautious about this marketplace, you’ll find them without trouble. Conversely, rationalizing a long-term position—beyond typical trends and average returns—is also an option.

I’m not denying that this could be confirmation bias on my part, but there’s a strong case to be made here.

Refer to:

Intriguing stats from the market’s growth narrative (Samlo, August 10, 2025)

Recent TCAF episodes, August 8, 2025

Are S&P 500 firms indeed achieving more with less? Yes, with three charts to prove it. (Matt Celminaro, August 6, 2025)

Previously:

All Time Highs are bullish (June 26, 2025)

Grandly Underrated 15 Years (April 28, 2025)

Managing Noise (June 17, 2025)

______

1. Juniper Networks peaked in 2000 at a market cap of $77 billion. Fast forward twenty-five years, it’s around $13.3 billion now. Pets.com has become obsolete, but Chewy has emerged successfully in the same space. The Metropolitan Fiber Network went bankrupt in 2002, only to be acquired by Zayo Group a decade later.