Momentum investing is often overlooked. A recent survey from the Cambridge Judge Business School suggests that stocks outpacing the S&P 500 in the last year may yield over 17.5% in the coming year.

What are momentum stocks?

Momentum stocks are shares in companies that experience a significant catalyst—something that drives their prices up or down. Events like earnings reports, mergers, acquisitions, and breakthroughs in technology or medicine play key roles here. Many of these investors also use technical indicators like the relative strength index (RSI) and the moving average convergence/divergence (MACD). This technical perspective seems to resonate most with investors.

Why invest in momentum stocks?

As market conditions shift, astute investors know how to adapt their strategies for better returns while minimizing risk. Buying into momentum stocks can enhance your earnings, provided you understand what to look for in them.

When assessing momentum stocks, consider these points:

- Focus on those that have outperformed the S&P 500 over the past year.

- Opt for stocks within a rising cycle or experiencing secular growth.

- Scrutinize stocks in industries undergoing significant transformation.

- Utilize technical indicators like MACD and RSI to optimize your entry points.

- Stay updated on relevant data and news to make necessary adjustments, as momentum can shift quickly.

Drawbacks of momentum stocks

The downside of these investments is that they can rapidly lose their momentum and change direction. This approach often requires a hands-on, time-intensive method that isn’t ideal for the average retail investor. It’s crucial for momentum investors to distinguish between actual shifts in momentum and mere volatility.

Here’s a selection of stocks exhibiting promising momentum:

Pagaya Technologies (PGY)

Futu Holdings (FUTU)

Holy Grail (GRAL)

Mitsubishi UFJ Financial (MUFG)

Vertiv Holdings (VRT)

Hims & Hers Health (HIMS)

Interdigital (IDCC)

Super Microcomputer (SMCI)

Trimas Corporation (TRS)

Tempus AI (TEM)

Brief analysis of Futu Holdings

Futu Holdings (FUTU) operates as a tech-driven digital brokerage and asset management platform globally through its U.S. subsidiary, Moomoo. Tencent is also a key shareholder.

So, with over 125% gains since April, why do I still feel optimistic about Futu?

As Hong Kong’s leading high-tech broker, Futu has shown record revenue and profit growth. Its profit margins are among the industry’s best, and ongoing trading interest from China could fuel further momentum. I believe that its strong earnings growth per share, combined with international expansion, positions it for even greater success in the coming years. Additionally, new U.S. crypto offerings could significantly boost revenues.

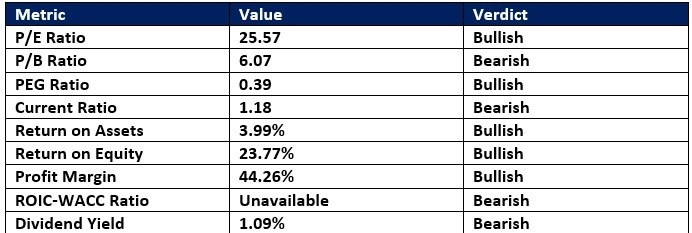

Futu boasts a price-to-earnings (P/E) ratio of 25.57, which is relatively low compared to the S&P 500’s ratio of 30.01.

The average analyst target for Futu is 205.10, indicating potential for significant gains with reduced risk of downturns.

Futu Holdings technical analysis

- The D1 chart for Futu shows price movements within Fibonacci retracement levels between 0.0% and 38.2%.

- It also indicates Futu Holdings is operating within bullish price channels.

- Generally, the indicators suggest a positive trend.

My view on Futu Holdings

I’ve established a long position in Futu within the range of 177.51 to 191.60. This stock seems fairly priced even after substantial rallies. The PEG ratio suggests further room for growth, and its profit margins rank highly in the sector, anticipatory of enough free cash flow to support expansion.

Brief analysis of Vertiv Holdings

Vertiv Holdings (VRT) manufactures and delivers essential infrastructure and services for data centers and communication networks globally, operating in over 40 countries with various regional headquarters. The company maintains many manufacturing and assembly facilities and employs more than 30,000 individuals. Vertiv is also part of the Russell 1000 Index.

Despite the recent loss of momentum, why am I still positive about holding Vertiv?

Vertiv has solid foundations, positioning itself well in the AI sector while managing to sustain growth through challenges. Its PEG ratio indicates untapped value, and the company invests 5% of its revenue in R&D, holding 3,000 patents and 1,800 trademarks.

With a P/E ratio of 61.04, Vertiv is competitively priced against the Russell 1000 index’s ratio of 63.42.

The average analyst target for Vertiv is 157.42, suggesting significant potential for upward movement from current prices.

Vertiv Holdings technical analysis

- The D1 chart for VRT indicates price movement within Fibonacci levels of 38.2% to 50.0%, showing positive activity after breakouts.

- It also demonstrates support zones, although indicators are leaning bearish.

My view on Vertiv Holdings

I’ve taken a long position in Vertiv Holdings between 121.41 and 134.93, citing good organic growth rates, a robust backlog exceeding $8.5 billion, and a diverse customer spectrum as reasons for my optimism. I see it as a top contender in the data center space.

Thinking of trading momentum stocks? There are options to explore with reputable brokers.