Central banks diversify their reserves with smaller “non-traditional reserve currencies.”

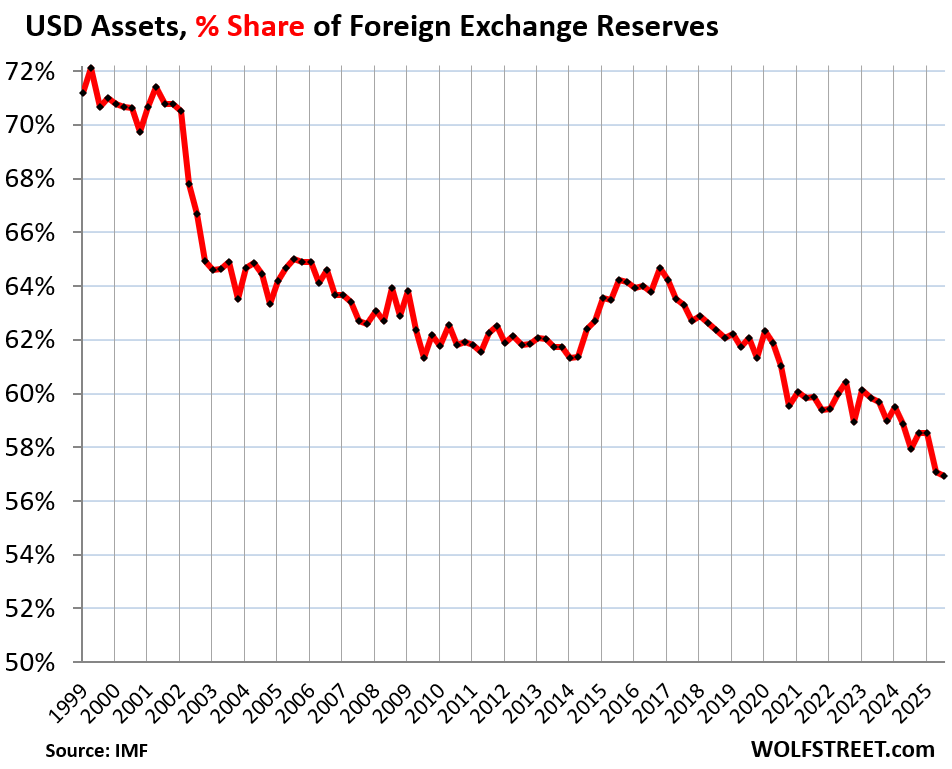

The proportion of US dollar assets held by central banks dropped to 56.9% of total reserves in the third quarter, marking the lowest level since 1994. This decline, from 57.1% in the previous quarter and 58.5% in the first quarter, is revealed in the latest IMF data regarding foreign reserves.

These US dollar assets include a range of securities like Treasury bonds, mortgage-backed securities, and corporate bonds. Notably, domestic currency assets, such as those from the Federal Reserve and the ECB, are not included in this tally.

Interestingly, foreign central banks did not actually sell off their dollar-denominated assets but rather managed to slightly boost their holdings. However, in contrast, they significantly increased their investments in other currencies, particularly in smaller, less traditional currencies, which caused the dollar’s share to dip further.

Even with a decrease towards the 50% threshold, the dollar remains the predominant reserve currency, standing taller than other currencies combined. Yet, this shift does have important implications.

Why is maintaining a dominant reserve currency important for the US?

When foreign central banks invest in US dollar-denominated assets, it generally drives up prices while pushing yields down. The strength of the dollar as the main reserve currency allows the US to fund its significant trade and budget deficits at a lower cost, a situation that’s persisted for decades. If this decline in the dollar’s prominence continues, there could be less demand for US government bonds, which might complicate efforts to maintain those deficits.

Looking back, the dollar’s share was already below 50% in the early ‘90s after a steady decrease from its peak of 85.5% in 1977. This drop coincided with severe economic challenges in the US, marked by high inflation and interest rates, alongside multiple recessions. Central banks started doubting the Fed’s capability to manage inflation, which has hit the country in waves of unprecedented intensity.

The dollar’s lowest point was 46% in 1991, but with inflation eventually controlled, central banks began re-accumulating dollar assets. The advent of the euro brought additional competition but was not as impactful as European leaders had anticipated. The promise of parity with the dollar faded amid the euro debt crisis that arose in 2009.

In the last decade, there has been a surge of smaller “non-traditional reserve currencies,” as identified by the IMF.

A graph illustrates the dollar’s share at year-end, with 2025 showing data from the third quarter.

Foreign central banks increased their dollar-denominated securities, but not by selling them.

As of the third quarter, holdings of dollar-denominated assets by foreign central banks rose to $7.4 trillion, indicating a third consecutive increase.

Since mid-2014, these holdings have mostly remained stable, despite some fluctuations. The decline in the dollar’s share over the years appears largely due to an increase in reserves held in diverse currencies as central banks widen their investment portfolios.

A chart displays the trillions of dollars held by foreign central banks in US dollar-denominated assets.

Leading foreign exchange reserves by currency.

Overall, central bank foreign exchange reserves climbed to $13 trillion in the third quarter.

Top holdings (in USD):

- USD assets: $7.41 trillion

- Euro assets (EUR): $2.65 trillion

- Yen assets (YEN): $0.76 trillion

- British pound assets (GBP): $0.58 trillion

- Canadian dollar assets (CAD): $0.35 trillion

- Australian dollar assets (AUD): $0.27 trillion

- Chinese renminbi (RMB) assets: $0.25 trillion

The euro, as the second largest currency, has maintained a share around 20% since 2015, after having previously approached 25% before the euro debt crisis.

Meanwhile, the remaining currencies are varied and less stable. The euro’s share has remained consistent since 2015, growing slightly at the expense of the dollar.

Emergence of “non-traditional” key currencies.

The accompanying graph highlights the significant growth of various small “non-traditional reserve currencies,” showing their total share reaching 5.6%, just below yen-denominated assets.

Interestingly, the share of the renminbi has been on a downward trajectory since early 2022, plummeting back to 2019 levels due to capital controls and other challenges.

In summary, both the US dollar and renminbi have started to lose ground to these emerging “non-traditional reserve currencies,” as central banks look to diversify their holdings away from traditional assets.