(Bloomberg) – This past week, while US stocks soared and recession talk persisted, currency traders remain quite pessimistic about the US dollar.

Strategists from JPMorgan Chase & Co. and Deutsche Bank AG believe the currency is still on a downward trajectory. The dollar index is hovering near its April lows, suggesting investors are hesitant to re-engage, even with easing trade tensions in China that have buoyed other markets.

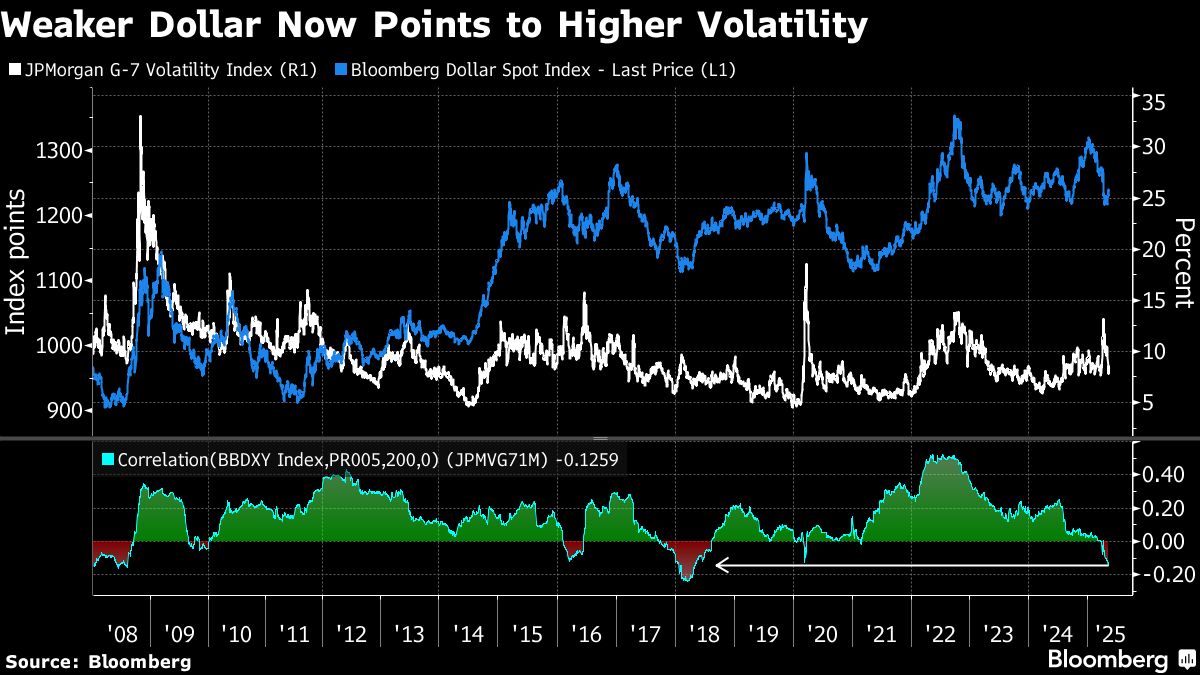

It has been quite a ride, with the dollar falling over 6% against a basket of currencies this year. Many analysts see US policymaking as unstable and unpredictable, which diminishes the dollar’s appeal as the Federal Reserve adopts a more cautious approach. Despite denials from Washington, some investors think that the Trump administration might actually be trying to weaken the dollar to benefit US manufacturing.

“With the Fed’s current stance, coupled with low growth and persistent inflation, along with continued uncertainty in US policies, we expect the dollar to stay under pressure,” said Kristina Campmany, a senior portfolio manager at Invesco. “We believe the dollar is just starting its decline, especially considering the amount of US assets held overseas, notably substantial stock shares.”

Expectations in the options markets for a weaker dollar next year have reached their highest since 2020. These long-term options tend to be favored by money managers rather than short-term speculators, indicating a broader reassessment of dollar risk is underway.

“American exceptionalism is slowly diminishing, and these trends are likely to continue,” Kaimaksha Triviedi, global currency director at Goldman Sachs, remarked to Bloomberg Television this week.

On the flip side, the S&P 500 surged over 5% this week. Optimism over President Trump’s Middle East tour has spurred hope regarding tech trading and inflation data. Notably, US equity funds saw an inflow of about $19.8 billion for the week ending May 14th, according to Bank of America data, marking the first influx in five weeks.

Despite a temporary 1% rise in the dollar following news of the US and China agreeing to cut tariffs, it quickly lost those gains as the week progressed. Still, the dollar remained restrained from making further gains by week’s end.

Jitania Kandhari, Associate Chief Investment Officer at Morgan Stanley, viewed the dollar’s earlier recovery as a brief exception in a broader trend, predicting it could face another 6% decline before year’s end.

“We’ve enjoyed a period of US exceptionalism, but that trend will take years to revert,” Kandhari stated in an interview.

According to George Saravelos, global currency strategy head at Deutsche Bank, while US asset inflows are cooling, nations like Taiwan are asking banks to reassess risk management for US investments. This suggests a dwindling interest in Treasury purchases, typically viewed as the safest bet.

He noted a noticeable separation between US yields and the dollar, pointing out that the dollar’s weakness against the yen coincides with a rise in Treasury values, especially since Japan has long been a major investor in US bonds, and its slowing engagement is significant.

JPMorgan analysts maintain that shorting the dollar remains a valid strategy. They argue that a relaxed US approach to tariffs may bolster economic growth elsewhere, positively influencing other currencies.

Mark Nash from Jupiter Asset Management indicated that investors are increasingly looking for nations with significant dollar reserves, opting to shorten their dollar positions against local currencies, with the Korean won and Indonesian rupiah standing out.

“Asia seems to be leading this global repatriation trend,” he commented. “Investors are pulling capital back from the US.”

Meanwhile, traders in the derivatives market have turned decidedly bearish on the dollar, with the latest Commodity Futures Trading Commission data showing they hold approximately $16.5 billion in positions anticipating further dollar losses as of May 13th.