I wrote on the 15th about some interesting deals for the week:

- Long on the EUR/USD currency pair, which dropped by 0.26% this week.

- The USD is positioned long, seeing a decline of 1.87%.

- There’s a long position on USD silver, decreasing by 0.96%.

- If every day in New York surpasses $80.43, the outlook for WTI crude oil is long, although this setup hasn’t been established yet.

Overall, this translates to a loss of 3.09%, averaging about 0.77% loss per asset.

This morning, both the Middle East and Europe faced startling news. The US allied with Israel in combat against Iran, employing advanced weaponry to swiftly take out Iranian nuclear facilities. The Iranian regime, along with its forces, has been under attack for over a week now. It seems like a significant win for both Israel and the US.

The US asserts that the strike was entirely successful. Interestingly, the International Atomic Energy Agency reports no spike in radiation levels at these facilities post-attack.

According to Al Jazeera, Iranian engineers have been working for the last three days to remove materials from the Fordow plants. It’s uncertain whether this development is vital, but there appears to be a sense of relief across regions like the Middle East, Europe, and the US today.

The Iranian government claims that uranium previously enriched before the attack was taken out from Fordow. Considering what the US and Israel have shown so far, it’s reasonable to speculate on their current considerations.

Meanwhile, the Iranian regime is issuing blood treatment threats, yet US citizens assert there’s nowhere safe—this comes after alleged war crimes involving attacks on Israeli civilian buildings with cluster munitions last week. So far, Israeli targets have only faced smaller missile attacks (around 45), but reports suggest the Iranian Navy might shut down the Strait of Hormuz and could potentially strike Dubai’s targets. If successful, WTI crude prices may jump above $100 per barrel, though deliveries have been proceeding normally. Reportedly, Israel struck Iranian naval assets in Bandar Abbas yesterday.

In the US, several Congressional Democrats have condemned Trump’s actions, with some calling for a permanent procedure, while rumors suggest Congress had previously endorsed such a strike. Others are concerned that Trump has entangled the US in yet another Middle Eastern conflict.

Predicting market responses to these events is challenging. There could be more fallout later today before the markets open. For instance, the Tel Aviv Stock Exchange gained over 1.6%. Initially, gold prices surged about $40 per ounce following the attack, but later declined.

Current evidence suggests the market may view recent events as favorable for risk appetite, although crude oil remains particularly vulnerable to potential Iranian retaliatory measures.

Last week’s significant data releases included:

- Federal Reserve Policy Conference – The Fed maintained its interest rates, aligning with expectations, although there’s a slow pace of potential cuts. Still, the CME FedWatch tool hints at two more 0.25% cuts expected by the end of 2025.

- Bank of Japan Policy Meeting – The bank has indicated a course towards further rate hikes, albeit with some board members showing a hint of dovish tendencies, potentially weakening the yen.

- Bank of England Policy Conference – No changes were made, in line with expectations, though a few members voted for a cut.

- Swiss National Bank Policy Conference – The SNB reduced rates to 0.25% as anticipated.

- Retail Sales in the US – Surprised many by showing a contraction of 0.9% versus the expected 0.5%.

- UK CPI (Inflation) – Came in higher, with an annual rate of 3.4%.

- New Zealand’s GDP – Exceeded expectations, showing an annual increase of 0.8%.

- UK Retail Sales – Undercut expectations, posting a monthly decline of 2.7% when only a 0.5% drop was anticipated.

- Australia’s unemployment rate held steady at 4.1%.

Looking ahead, next week will feature a lighter schedule with no major data releases, but key events may include Chairman Powell’s testimony before the US Congress and the core PCE price index data. The implications of the Iranian conflict will likely play an even bigger role in market movements.

Key upcoming data points this week, in order of likelihood, are:

- Federal Reserve Chairman Jerome Powell’s testimony before Congress

- Core PCE Price Index for the US

- Final GDP for the US

- Canada’s CPI (inflation) data

- Australian CPI (inflation)

- Canada’s GDP

- Service & Manufacturing PMIs for the US, Germany, UK, and France

- US unemployment claims

The most consequential events within the Forex market will likely stem from the top three items listed.

Interestingly, back in June 2025, we anticipated the EUR/USD currency pair would rise, and here’s a look at how that’s unfolding:

Last week, there wasn’t any significant price movement in the Forex market, which is why I hesitate to make predictions every week.

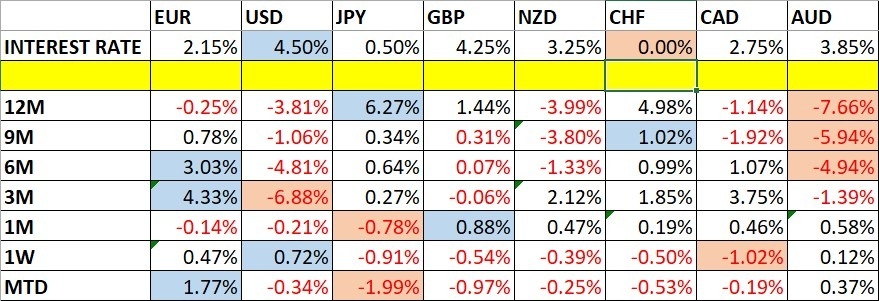

In terms of performance, the US dollar emerged as the strongest major currency, while the Canadian dollar ranked weakest. Overall, volatility decreased last week, capturing just 19% of crossings among critical foreign currency pairs.

For those trading USD in the Forex market, keep an eye on whether 97.54 holds as a critical level. If you’re involved in other marketplaces, there’s less reason to stress about the dollar’s performance.

The Tel Aviv Stock Exchange 125 Index noted a 1.6% rise this morning, buoyed by its best week in almost five years.

It might seem counterintuitive that the Israeli stock market is thriving amidst conflict, but we need to recognize that their military capabilities far exceed those of their opponents.

Following the recent US-led destruction of Iranian nuclear sites, Iranian retaliation seems relatively subdued at the moment.

Though discussions often center on the nuclear threat to Israel, it’s worth establishing that even a nuclear-armed Iran wouldn’t destabilize Israel’s economy fundamentally.

Israel faces its challenges post-conflict, but we might witness more activity surrounding the Israeli stock market next week.

The EUR/USD currency pair seems to be maintaining its effective long-term bullish trend, showing a solid record of adherence to those patterns.

Prices have reached recent highs but experienced significant pullbacks, only to rise once more. The weekly chart has printed a notable doji candlestick.

Some pressing questions arise:

- Will the US’s success in Iran foster a stable market, or will fear of retaliation drive investors to safer havens?

- Could the US dollar see substantial gains from a flight to safety, while the euro’s position remains uncertain?

If the initial part of today’s Tokyo session shows bullish trends for this currency pair, it may be prudent to consider following that trend.

Even with the US dollar showing some weakness last week, the overall picture for precious metals remains strongly bullish, showcased by long-term upward trends.

The immediate future depends on the market’s reaction: if participants fly to safety or if there’s significant retaliatory action from Iran post-attack.

Gold prices hovering around $3,420 per ounce indicate a slight drop from recent peaks, but caution is warranted for those considering new trades—waiting for a solid closure above $3,500 might be wise.

Silver in USD touched a remarkable 13-year peak above $36 per ounce last week. However, the recent weekly candlestick hints at a potential decline. Still, there’s a persistent bullish trend in precious metals, including silver.

For those who prefer a cautious approach, holding off for a clearer signal of upward momentum before entering new trades may be beneficial.

Turning to WTI crude oil, the daily chart reveals several bullish indicators:

- A bullish double bottom forming around $55.00.

- A cup and handle chart pattern following that double bottom, or something quite similar.

- Continued bullish momentum from last week.

Clearly, crude oil prices rose significantly following the outbreak of the conflict between Israel and Iran. Ongoing tensions could further fuel price hikes, especially considering the US’s involvement.

With Iranian threats hovering, there’s anticipation around potential volatility. If Iran retaliates successfully, crude prices could soar past $100.

It’s essential to be cautious in trading such a volatile environment. The best approach might be to wait until the end of the day and look for a confirmed higher close above $80.43 before making new long trades.

To recap, here are the best deals for this week:

- Long on the EUR/USD currency pair.

- Long on the USD.

- Long on silver when prices surpass $37.13 in New York.

- Long on WTI crude oil if it exceeds $80.43 daily in New York.