Important points

- ORCL has seen its stock drop 42% in six months, yet RPO surged 438% to $523 billion in Q2 FY26, indicating potential long-term revenue growth.

- To satisfy rising AI demand, ORCL is expanding its data centers and GPU capabilities, which should help cloud growth in Q3.

- Oracle’s multicloud database segment experienced an impressive 817% growth in the second fiscal quarter.

Oracle (ORCL) has faced a significant decline, with shares down 42.8% over the last six months. This is quite a contrast to the Computer & Technology sector’s overall return of 12.8% and the Computer Software industry’s return of 25.8%, making ORCL a weaker performer among its peers. The stock’s drop was especially pronounced in January 2026, fueled by concerns about capital management and execution, leading to an extra 15.6% dip.

Despite these challenges and the rising unease around capital allocation, some fundamental indicators may encourage investors to think twice about potentially holding on or waiting for some stabilization before they buy into 2026. The company’s progress and strategic stance in AI infrastructure suggest a need for careful consideration, which goes beyond just short-term market reactions.

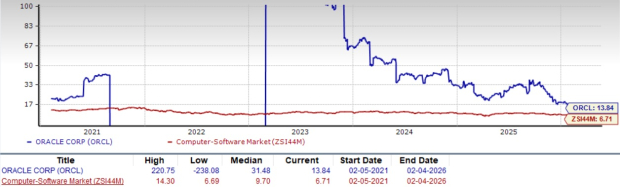

ORCL 6-month price performance

Image source: Zacks Investment Research

Unprecedented order backlog suggests long-term earnings prospects

In Oracle’s second quarter results for fiscal 2026, a notable shift in business trajectory was revealed through significant contract revenue gains. Remaining performance obligations skyrocketed 438% year-over-year to reach $523 billion, including an additional $68 billion just this quarter. This backlog features major commitments from industry leaders like Meta and NVIDIA, who are turning to Oracle’s cloud infrastructure for their AI workloads. Such a robust contracted revenue forecast offers considerable long-term visibility, with about 33% expected to convert to recognized revenue within the next year.

Management’s optimistic outlook suggests confidence in transforming this extensive backlog into actual financial gains. They are holding steady on their full-year revenue guidance of $67 billion for 2026 while anticipating an additional $4 billion for 2027 based on faster RPO conversion. This pipeline illustrates that even amidst market skepticism about investments in AI infrastructure, Oracle is securing real customer commitments instead of just riding on speculative demand. The third-quarter guidance projects a 37% to 41% boost in total cloud revenue, excluding currency effects, indicating continued strength in this core growth area.

Strategic infrastructure expansion position for future capacity

Oracle’s proactive capital deployment strategy reflects a careful approach to satisfy existing contractual obligations rather than making speculative investments, even if this raises concerns for short-term investors. In the recent second fiscal quarter, the company provided around 400 megawatts of data center capacity to clients and boosted GPU capacity by 50% since the prior quarter. This expansion is directly aligned with customer commitments, and the SuperCluster facility in Texas is progressing well, with over 96,000 NVIDIA chips already delivered. Currently, Oracle boasts 147 operational customer-facing regions and plans for an additional 64, surpassing cloud competitors in geographic range and offering customers versatile deployment options.

In February 2026, Oracle unveiled intentions to raise between $45 billion to $50 billion through a mix of debt and equity to build more capacity for key clients like Advanced Micro Devices and TikTok. The fiscal 2026 capital expenditures ballooned to about $50 billion from an earlier estimate of $35 billion, yet management has stressed that these investments directly support revenue-generating equipment. The company’s resolve to uphold investment-grade debt ratings via strategic financing exhibits a sense of financial discipline. Further, the introduction of Oracle AI Database 26ai Enterprise Edition for Linux has enhanced its autonomous database features for AI needs.

Multi-cloud strategy drives differentiated market position

In an increasingly consolidated cloud infrastructure landscape, Oracle’s multicloud strategy has established itself as a significant differentiating factor. The multicloud database segment saw an incredible 817% growth in the second quarter, thanks to partnerships that incorporate Oracle databases. Customers can run Oracle workloads within various cloud platforms, preserving database revenue while broadening the potential market beyond Oracle’s own services. This encourages smoother transitions for customers selecting cloud providers and enhances revenue opportunities.

Oracle has established 72 multicloud data centers seamlessly integrated with its competitors’ cloud platforms. This cooperative strategy allows for revenue capture from database workloads, independent of underlying infrastructure preferences. During the second quarter, cloud infrastructure revenue climbed 68% year-over-year to $4.1 billion, and total cloud revenue hit $8.0 billion, reflecting 34% growth. Despite setbacks in January 2026, which included a bondholder lawsuit and multiple analyst downgrades, the core multicloud strategy appears robust and continues to produce meaningful results across various customer segments globally.

Evaluation and competitive environment

Oracle’s elevated valuation mirrors both anticipated growth and concerns regarding execution risk. The stock trades at a trailing-12-month price-to-book ratio of 13.84x, which substantially exceeds the industry average of 6.71x. In the cloud infrastructure sector, Oracle squares off against major players like Google’s Cloud, Amazon Web Services, and Microsoft Azure. Alphabet has utilized its search engine revenue to fund its cloud ventures, while Amazon capitalizes on its early market lead. Meanwhile, Microsoft has seamlessly integrated Azure with its productivity services to create a compelling bundle. These competitors possess greater financial resources, as evidenced by stronger balance sheets.

ORCL trades at a premium

Image source: Zacks Investment Research

Nonetheless, Oracle’s expertise in databases and its multicloud collaborations with Alphabet, Amazon, and Microsoft present a unique market stance. This strategic alliance enables Oracle to tap into multiple cloud environments simultaneously, thus mitigating competitive disadvantages by leveraging specialized databases that supplement Alphabet’s, Amazon’s, and Microsoft’s infrastructures.

Conclusion

The 42% decline in Oracle’s stock price has crafted a complicated investment scenario, where intrinsic strengths contrast with valid enforcement concerns. The company’s record backlog, strategic infrastructure initiatives, and unique multicloud positioning present compelling reasons for current stakeholders to remain invested, despite the fluctuations. However, short-term pressures, such as high valuations and increasing capital requirements alongside litigation issues, suggest that careful investors might want to hold off until there’s more clarity regarding the sustainability of the capital structure and the timing for revenue realization. Currently, ORCL carries a Zacks Rank of #3 (Hold).