(Bloomberg) – Wall Street is experiencing its most significant rise since May, buoyed by the strengthening tariff agreements between President Donald Trump and the European Union, as well as a trade ceasefire extension between the U.S. and China. Stocks are nearing record highs while bond yields have softened.

With the beginning of the week shaping market trends for the remainder of the year, the U.S. dollar has continued its rally from July. The euro, on the other hand, has dropped the most it has in over two months, with the S&P 500 hovering around 6,400. Following two years of strong note sales, the Finance Ministry has seen minimal issuance. Oil prices are on the rise, particularly after Trump indicated that Russia may accelerate its efforts to agree on a ceasefire in Ukraine.

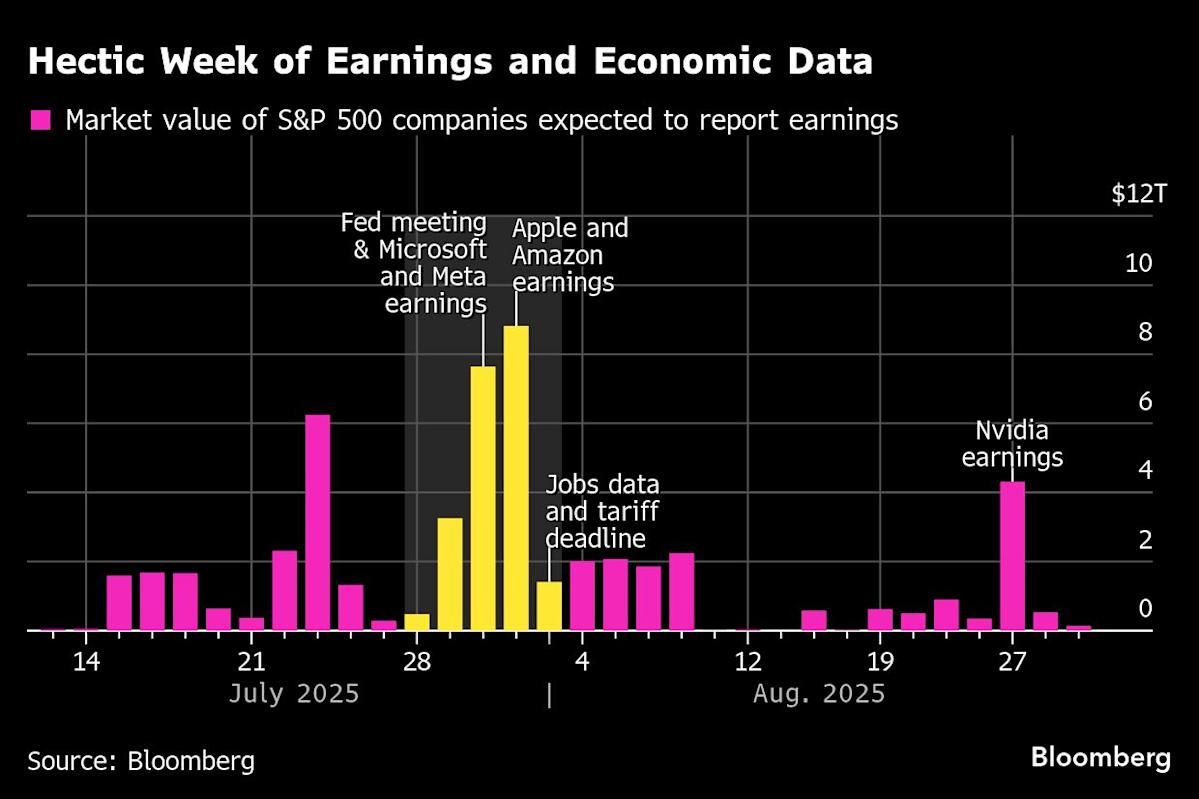

As the U.S. prepares to impose tariffs on August 1, traders are gearing up for a wave of vital data related to employment, inflation, and overall economic activity. A key moment is expected on Wednesday, as the Federal Reserve is likely to keep interest rates unchanged. After that, several major tech companies are set to report earnings, collectively representing a staggering $11.3 trillion market cap.

“This week is pivotal for the market,” observed Chris Larkin from Morgan Stanley’s E*Trade. “We might see some momentum shift in either direction.” U.S. and Chinese officials are engaged in two days of talks aimed at prolonging the tariff ceasefire beyond the mid-August deadline. Meanwhile, Canadian Prime Minister Mark Carney mentioned ongoing trade discussions with the Trump administration.

Trump has expressed optimism about reaching an armistice with Ukraine, imposing a new timeline that could compel Moscow to halt its military actions. “While we’re maneuvering over tariffs, we’re effectively making substantial shifts, either positively or negatively, enabling American businesses to strategize and adapt,” said Peter Bookbar in a report.

Thierry Withman from Macquarie Group noted that the current strength of the dollar could suggest that new EU agreements favor the U.S., which might also hint at the U.S. re-establishing connections with its primary allies. Ian Lyngen and Vail Hartman of BMO Capital Markets added that, although the real economy hasn’t yet felt the full impact of this shifting landscape, recent data has certainly reinforced the narrative of U.S. economic exceptionalism.

Federal Reserve Chairman Jerome Powell and his colleagues are scheduled for a boardroom discussion on Tuesday, amidst considerable political pressure and evolving trade dynamics. This gathering is somewhat rare, coinciding with the release of key economic reports on GDP, employment, and the Fed’s preferred inflation measures. A robust recovery is expected in the second quarter based on forecasts.

Although the Fed is anticipated to refrain from cutting interest rates this week, ongoing shifts in inflation data—especially in the context of tariffs—could provide a stronger indication that cuts may occur in the fall. As for the stock market, while it appears highly valued, some analysts believe there’s still room for growth.

This earnings season has started strongly, with Microsoft Corp. and Meta Platforms Inc. set to report on Wednesday, while Apple Inc. and Amazon.com Inc. will do so on Thursday. Corporate America seems to be handling tariffs well—around 82% of S&P 500 companies that have reported so far are on track to achieve their highest quarterly profits in about four years.

Lori Calvasina at RBC Capital Markets stated that it’s still early to fully assess the implications of tariffs on inflation and corporate earnings. “If the outlook for 2026 isn’t as bright as investors hope, it could present risks for the stock market,” she warned.

John Stoltzfus from Oppenheimer Asset Management noted that successful trade negotiations could lead to a third consecutive year of 20% profits for the S&P 500 and has raised the year-end target for the U.S. benchmark to 7,100. Some analysts, like Morgan Stanley’s Michael Wilson, have become more optimistic regarding the S&P 500 due to anticipated strong revenue. Meanwhile, Craig Johnson from Piper Sandler highlighted that technical indicators suggest increasing participation in stocks beyond the lows recorded in April.

“Even if momentum has slightly waned as investors wait for returns, the overall market breadth remains encouraging, providing opportunities for investors to buy the dips,” he remarked. Lisa Shalett of Morgan Stanley Wealth Management pointed out that the stock market’s impressive rebound is reinforcing investors’ tendency to buy on dips.

In what could be termed a classic convergence of technical momentum and basic strength, analysts are observing that the S&P hasn’t fluctuated significantly in over a month, signaling that bears may be retreating. “No one is looking to short this market, and even typically skeptical investors seem to be getting drawn in,” said Hackett, pointing out that despite not being at the peak yet, the likelihood of reaching one is rising.

Company highlights:

-

Samsung Electronics Co. has secured a $16.5 billion deal to produce AI semiconductors for Tesla Inc., enhancing its struggling casting division.

-

Cisco Systems Inc. was downgraded to inline by Evercore after valuation adjustments following recent profits.

-

Nike Inc. has been noted by JPMorgan Chase & Co. for its recovery following a five-year multi-year plan affecting its revenues.

-

PayPal Holdings Inc. will soon allow businesses to accept over 100 cryptocurrencies at checkouts.

-

Roche Holding AG aims to test whether an experimental drug can prevent Alzheimer’s symptoms in high-risk individuals.

-

U.S. regulators are investigating the death of an 8-year-old Brazilian boy who received treatment with Sarepta Therapeutics Inc.’s Elevidys.

-

Arrowhead Pharmaceuticals Inc. has announced it expects a $100 million milestone payment from Sarepta Therapeutics Inc. soon, creating pressures on the biotech firm still grappling with earlier drug sales concerns.

As a Bloomberg strategist observed, “New trade agreements in Europe and recent consultations with China are likely to bolster risk sentiment in the coming days. The August 1 deadline seems less significant now, as some frameworks are emerging between Europe, China, and Japan.”

Some key market movements:

Stocks

-

The S&P 500 showed minimal change around noon in New York.

-

Nasdaq100 increased by 0.3%

-

The Dow Jones industrial average hardly budged.

-

Stoxx Europe600 slipped 0.2%

-

MSCI World Index fell by 0.2%

-

Bloomberg 7 Total Return Index rose by 0.7%

-

Russell 2000 index dropped by 0.1%

Currency

-

Bloomberg Dollar Spot Index increased by 0.7%

-

The euro declined by 1.1% to $1.1610

-

The UK pound fell by 0.3% to $1.3393

-

Japanese yen decreased by 0.5% to 148.47 per dollar

Cryptocurrency

-

Bitcoin fell by 0.5% to $118,260.47

-

Ether decreased by 0.4% to $3,808.07

Bonds

-

Treasury yields rose by 2 basis points to 4.41% for 2010.

-

Germany’s 10-year yield dipped by 3 basis points to 2.69%

-

UK 10-year yield rose by one basis point to 4.65%

Spot commodities

-

West Texas Intermediate crude rose by 1.9% to $66.43 per barrel.

-

Spot Gold dropped by 0.7% to $3,314.74 per ounce.