Everyone is talking about the AI bubble, confirming it or denying it, but this is what it looks like from a leverage perspective.

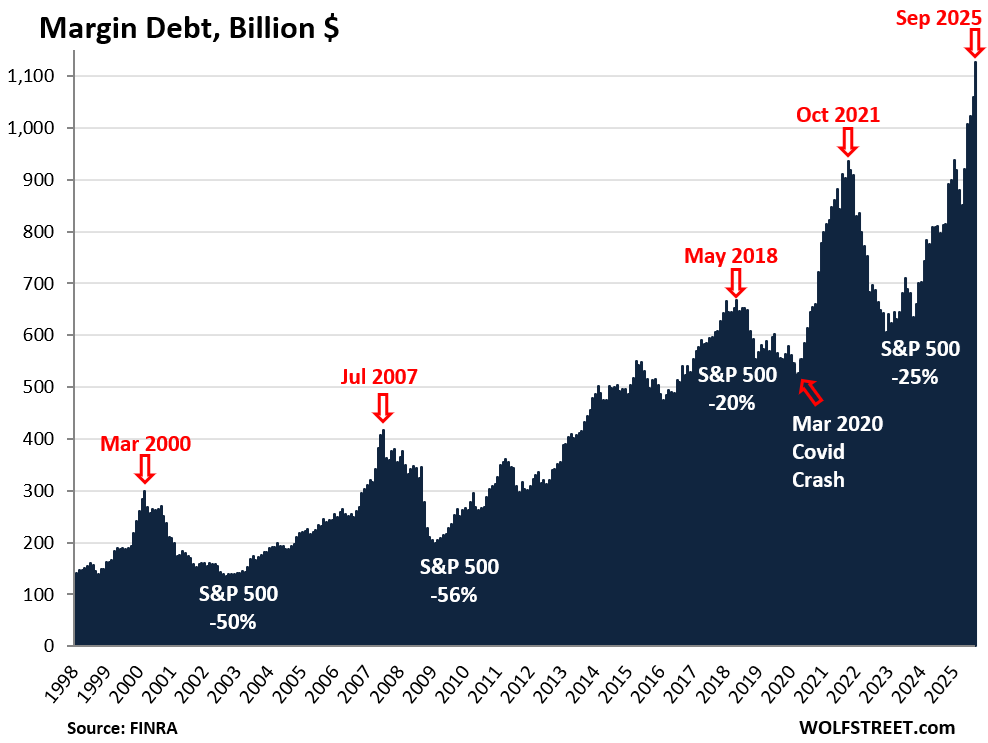

Since April, leverage in the stock market has seen a notable increase. In September, margin debt—the money investors borrow from brokers—rose by 6.3%, or about $67 billion, to an all-time high of $1.13 trillion.

During this same period, margin debt has jumped 39%, marking the most significant five-month increase since October 2021. After reaching its peak, stock prices began to decline in early November 2021, with the S&P 500 eventually dropping by 25%.

Additional leverage, meaning more borrowed money being funneled into the stock market, tends to drive prices up. It’s a double-edged sword, though—it can amplify gains, but it can also exacerbate losses. The rapid rise in margin debt over several months, hitting new highs frequently, points to heightened speculation and risk, which usually precede sharp downturns.

There’s been a lot of chatter about the AI bubble, with opinions swirling both ways. But what’s it like from the standpoint of leverage? The current spike in risk and speculation is generating considerable vulnerabilities, underscored by the sustained peak in margin debt.

When examining margin debt historically, it’s not just the total figures that stand out but rather the abrupt increases from record high to record high over short spans of time.

Annotations in the chart:

March 2000: This marked the onset of the dot-com crash, with the S&P 500 losing 50% and the Nasdaq dropping 78%.

July 2007: This period preceded the stock market’s alignment with the beginning of the financial crisis, during which the S&P 500 fell by 56%.

May 2018: By late 2018, the S&P 500 saw a 20% decline.

October 2021: This initiated a subsequent 25% drop in the S&P 500.

March 2020: Investors’ reactions to the pandemic caused a crash. Interestingly, leverage was relatively low and falling at that time, providing some protection to the market. If leverage had surged significantly in the months leading up to the pandemic, the decline might have been even harsher.