Health Insurance Dispute Leaves Family in a Bind

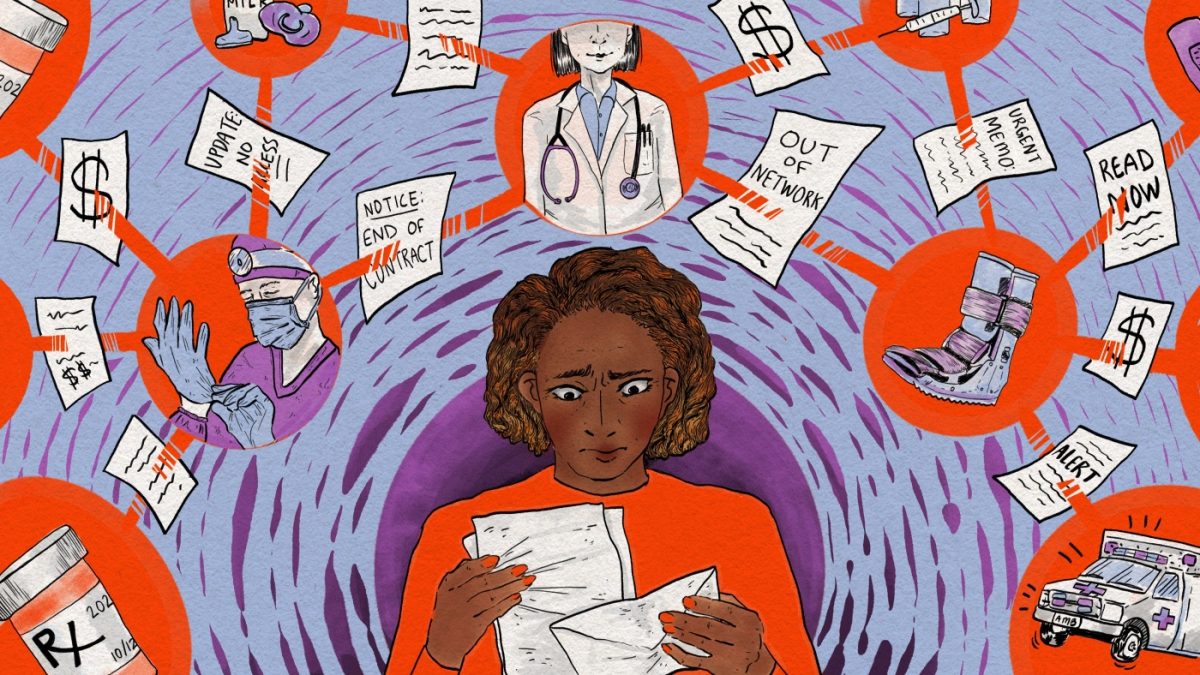

When her mother’s health insurance provider in Missouri failed to come to terms with local hospitals, Amber Wingler found herself in a tight spot with numerous physicians suddenly considered out of network. As a mother of five, she was left pondering, “Where do I even start?”

Amber Wingler, 42, from Columbia, Missouri

Last winter, Wingler started receiving urgent notifications from her local hospital about potential disruptions to her family’s health care. The hospital, MU Healthcare, which employs most of her family’s doctors, was stuck in a contract standoff with Anthem, her insurance company. The existing agreement was nearing its end.

On March 31, she was notified via email that the hospital would be removed from Anthem’s network. This news caught her off guard and distressed her.

“I get that they’re always negotiating, but this felt like red tape that didn’t involve us. I’ve never been this out of the loop with the network before,” she said.

The timing couldn’t have been worse; Wingler’s 8-year-old daughter, Cora, was struggling with a mysterious intestinal disorder. The wait times to see specialists ranged from several weeks to over a year.

Although MU Healthcare stated they were working to see urgent cases, Cora’s specialist visit turned out to be out of network. With each appointment costing a few hundred dollars, the financial burden quickly added up. The only other pediatric specialists available who were in network were over 190 miles away in St. Louis and Kansas City.

This forced Wingler to postpone Cora’s appointment for months as she tried to figure out the next steps.

Contract disputes between hospitals and insurance companies have become commonplace, with over 650 hospitals embroiled in public disagreements since 2021. Issues have arisen as hospitals brace for budgetary cuts in federal health spending.

If you’re caught up in a similar situation, it’s crucial to know your options to protect your finances. “There’s a saying that when elephants clash, the grass suffers, and unfortunately, that’s often the patient,” said Caitlin Donovan from the Patient Advocacy Foundation.

1. Know That “Out of Network” Will Likely Cost More

Insurance companies negotiate rates with hospitals to determine costs for various services, thereby creating their network. Most patients prefer in-network providers since they are often covered, but out-of-network services could leave them with hefty bills.

If you stick with your regular physician, even if it’s someone you don’t know well, ask about cash discounts or financial aid programs through the hospital.

2. Disputes Often Get Resolved

Research shows that approximately 18% of non-federal hospitals reported public disputes with insurers from June 2021 to May 2025. Interestingly, many of these negotiations wrap up within a month or two, meaning doctors often return to the network.

3. Look for Exceptions to Reduce Costs

If you have a serious condition, you may be eligible for continuity of care, which allows in-network coverage extensions. Contact your insurance for more information, but be prepared for it to take some time.

Wingler spent countless hours making calls, completing forms, and sending faxes for Cora’s care. Meanwhile, her son was in physical therapy, which added to the chaos. “I just can’t take on another fight,” she shared. “Just keep up with what you’re doing for now.” In emergencies, patients can’t be charged more than in-network rates.

4. Switching Insurers Is Not Quick

If you’re thinking of switching to an insurance company that accommodates your preferred doctor, tread carefully. Many people find themselves locked into their health plan for a year after enrollment, and the timing often doesn’t align with hospital contracts.

Common life events, like marriage or job loss, can help you switch outside the standard enrollment period, but a doctor leaving your network doesn’t qualify.

5. Finding a New Doctor Takes Time

If the issue seems ongoing, you might consider seeking out a new doctor within your insurance network. Start by using your insurance’s online tools to look for in-network providers, knowing that establishing care with a new doctor can take time and involve significant travel.

6. Save Those Receipts

Even if there’s no active contract at the moment, keep documentation of out-of-pocket expenses. If insurers and hospitals come to a new agreement later, they might retroactively cover costs for appointments you paid out of pocket.

After three months, Wingler learned that the two parties had reached a new agreement. She joined many others in rescheduling appointments that had been postponed.

Jim Turner from Anthem’s parent company stated that they aim for fairness and transparency in negotiations. MU Healthcare acknowledged the need for families to have timely access to specialized care and expressed regret over scheduling frustrations following the recent contract resolution.

Wingler expressed her relief at being able to access her healthcare providers again, but she also felt determined to avoid similar situations in the future. “I’ll likely be more proactive in checking insurance details,” she concluded.