Rising Premiums for Obamacare Plans in 2026

This week, information regarding health insurance prices for the next year under the Affordable Care Act, commonly known as Obamacare, was released. Many are experiencing significant hikes in their premiums across the United States, and we now have clearer data on these increases.

It’s worth noting that most individuals purchasing their insurance don’t actually pay the full price; tax credits established by the Affordable Care Act help offset those costs. However, the new rates indicate what many will face if the additional tax subsidies, which were initially approved in 2021 and extended in 2022, fade away at the end of this year.

Extending these subsidies would cost the federal government an estimated $23 billion next year, and around $350 billion over the next ten years, according to the Congressional Budget Office. The lapse of these subsidies could mean that numerous Americans encounter substantially higher expenses before the approaching midterm elections, with some possibly paying over a thousand dollars more each month.

The extent of these changes is contingent on various factors: where individuals reside, their age, and their income. This information is quite crucial moving forward.

The battle over funding is a central issue in Congress, contributing to a government shutdown that has persisted for almost a month. Democrats are insisting on an extension as a requirement for their support of a government funding initiative, while Republicans are holding out for a government reopening before even considering an extension.

The data illustrated in our charts derive from the KFF research group and reflect the insurance prices available on healthcare.gov and other state websites, which let users explore options before marketplaces open. The article previously included estimates for the next year’s premiums, but now we can present real figures affecting Americans currently.

There’s still a chance for Congress to act and modify the funding framework, but it’s unlikely to happen before individuals begin selecting their health plans this week.

Impact on Low-Income Individuals

For those with the lowest earnings, the potential expiration of subsidies could lead to the loss of free and generous insurance. Currently, Americans who earn less than $24,000 annually are not required to pay premiums due to these additional subsidies, though they still have some co-payments and deductibles when using their insurance.

For example, a single person making $22,000 might end up paying $66 monthly for a typical insurance plan after the subsidies expire. Approximately half of the people enrolled in the Affordable Care Act marketplaces will see similar increases, transitioning from no premium to payments ranging between $27 and $82 a month. This change primarily affects those close to the poverty line in states not expanding their Medicaid programs, where their insurance remains substantially subsidized, only at the original rates set by the initial Affordable Care Act.

Interestingly, although the numerical difference may seem minor, it can have significant impacts for individuals earning under $2,000 a month. Enrollment numbers in this income bracket have soared since the enhanced subsidies were put in place— especially in Texas, Florida, and Georgia. Critics of these subsidies express concerns over potential fraud with such high enrollment figures.

People earning a bit more, say $35,000, are facing standard price increases too. Their monthly cost for a common plan is set to climb from $86 to $218 without those enhanced subsidies.

Effects for Higher-Income Individuals

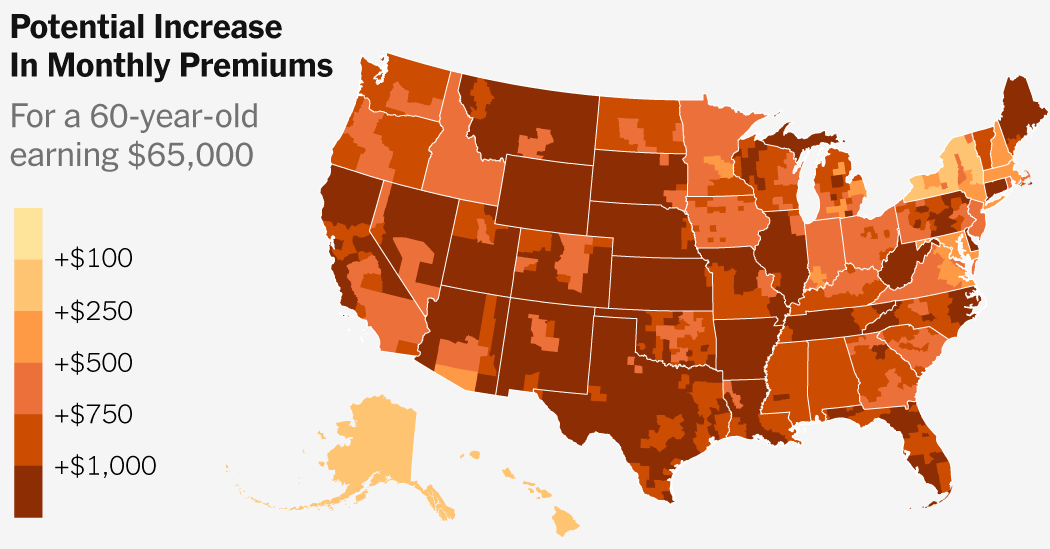

Older individuals in the $65,000 income range are likely to see steep increases in premiums—potentially hundreds of dollars more monthly, or exceeding $1,000. In many areas, enhanced subsidies previously capped how much people over $63,000 had to pay. Without these, they’ll be subject to whatever insurers in their market charge, often affecting those who are self-employed or working for small businesses.

The ability for insurers to charge older individuals more than their younger counterparts makes these subsidies particularly crucial for those nearing retirement. The average increase in insurance premiums—around 26 percent—coupled with the loss of subsidies compounds these hurdles.

Location also plays a significant role in premium pricing. In rural areas, rates tend to be higher, especially in states like Wyoming and West Virginia. For some living in the priciest markets, increases can be staggering. A 60-year-old in southern Illinois might face premium jumps from $460 monthly to $2,800 without subsidies.

Fewer than 10 percent of individuals enrolled in Obamacare fall into the $65,000-plus income bracket, further illustrating the disproportionate impact.

High Earners and the Age Factor

Those with even higher incomes could still be financially burdened by Obamacare premiums, regardless of subsidies. Younger people in this category often find little benefit from extra aid since assistance kicks in only when insurance costs exceed 8.5 percent of their income, a threshold primarily met in expensive markets.

On the other hand, older high earners do benefit from these subsidies; without them, their insurance costs will rise even more. This segment is also grappling with increasing premiums, and while they didn’t see the benefits of enhanced subsidies this year, their current premiums are still lower than the projected rates being offered for next year.

Overall, our analyses center on how subsidies influence individuals purchasing insurance, though the calculations are a bit more complex for families. Generally, families with lower incomes would see more consistent increases, while those with higher incomes would experience varying price changes based on location and the ages of family members.

To gauge potential costs for your household, you can use this online calculator provided by KFF to assess figures with and without subsidies.