Ohioans Grapple with Rising Insurance Premiums

CINCINNATI – As open enrollment kicks off, many residents in Ohio are confronting substantial hikes in their health insurance premiums. For some enrolled in the Affordable Care Act, there’s a real concern their costs could nearly double.

It’s quite alarming; some folks are watching their monthly bills spike by hundreds of dollars.

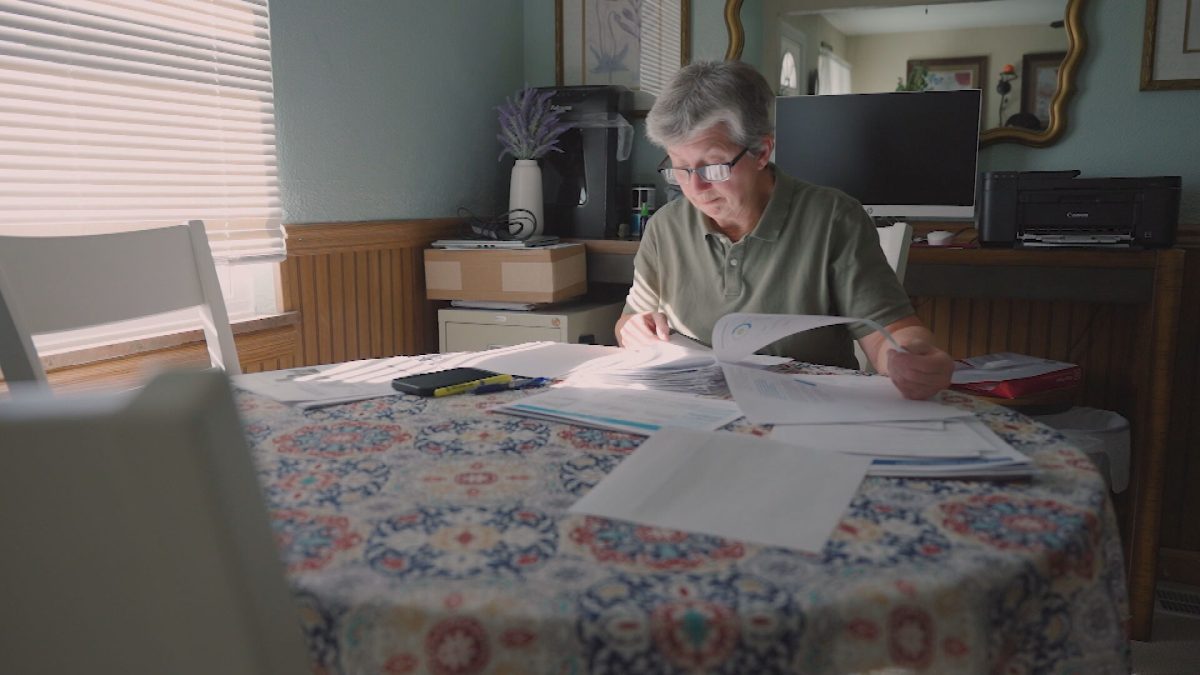

Take Barbara Campbell, a former sheriff’s deputy in Hamilton County. She’s caught in a dilemma about which plan to select this year. The network of doctors who have cared for her is critical to her choice.

“I’ve battled cancer several times, personally,” Campbell shared, highlighting her ongoing health considerations.

She also mentioned rising costs in other areas of healthcare. “Even getting new glasses has become a lot more expensive. And the price of contacts is up too,” she added.

Now retired, Campbell said the premiums through the Ohio Public Employees Retirement System have become daunting. “Prices have nearly doubled,” she expressed, adding, “I might have to look for another job just to cope with these hikes.”

Mark Pauley, a health economist at the Wharton School, pointed out that older individuals using ACA exchanges are particularly at risk.

“The most vulnerable I observe are seniors buying insurance on the exchanges, because premiums rise as you age,” Pauley explained.

This demographic might see their premiums soar by thousands, impacting around 20 million people. Conversely, individuals with employer-sponsored insurance may face a more modest increase of about 5%, provided their wages remain stable—though that often isn’t the case.

Pauley attributes these increases to multiple factors, including higher-than-anticipated insurance claims and uncertainty over whether federal subsidies for ACA plans will be extended. He also noted the ongoing repercussions of the coronavirus pandemic and the rising usage of costly weight-loss medications.

“They market insurance like Liberty Mutual that covers only what you choose, but health insurance is different,” Pauley remarked. “People end up paying for what they need.”

He advised anyone seeking more economical insurance options not to risk going without coverage. A bronze plan on the ACA exchanges or options with higher deductibles and copays might yield lower premiums, though he warned that medical savings accounts could become a gamble if faced with significant medical expenses.

As the Dec. 13 deadline approaches, Campbell is hopeful to find a solution that won’t force her back into the workforce. “It took me hours to realize these plans often don’t cover doctor costs,” she expressed. “I’m planning to meet with them one-on-one to see if they can help me uncover better options.”