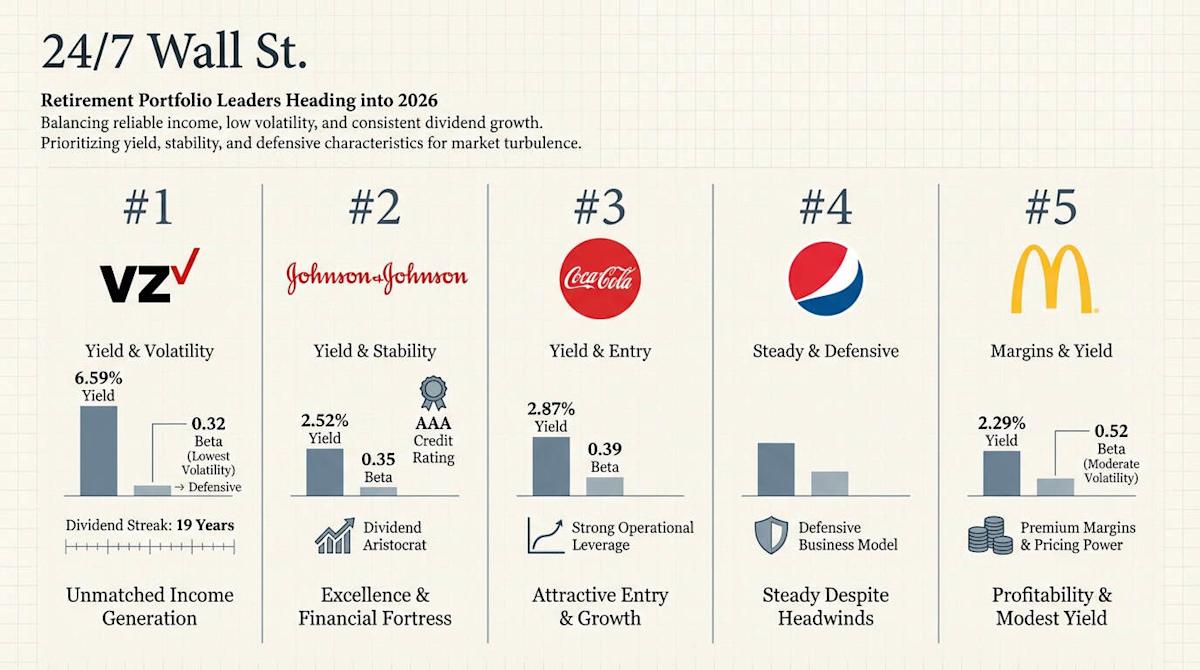

Dividend Stocks to Consider for Retirement

Verizon stands out with a notable yield of 6.59%, coupled with a beta of 0.32, and has consistently increased its dividend for 19 years. That’s quite impressive, I’d say.

McDonald’s, on the other hand, has an operating profit margin sitting at 46.90%. However, it experienced a decrease in book value by $3.04 per share due to share repurchases.

Meanwhile, Johnson & Johnson has raised its quarterly dividend by 4.8% to $1.30, and it also increased its revenue forecast for fiscal 2026 to $93.7 billion. Quite an optimistic outlook, if you ask me.

If retirement is on the horizon—for yourself or someone close—there are three simple questions to consider that could help many realize they might retire sooner than they think. It takes a few minutes to think this through.

For those getting close to retirement, having a stock portfolio that balances dependable income, low volatility, and consistent dividend growth is essential. Among six noteworthy dividend stocks, five shine in terms of financial stability, income generation, and defensive traits, which are crucial for weathering market downturns.

The assessment focused on several factors such as dividend yield, continued growth of those dividends, earnings stability, volatility (measured by beta), and strong cash flow. Additional details like profit margins, debt levels, and market positioning also played a part. So, let’s see how the top five retirement stocks rank going into 2026.

McDonald’s comes in fifth place, showcasing a dividend yield of 2.29% with an annual dividend of $7.08 per share. With a beta of 0.52, its volatility is moderate—making it somewhat less defensive than some rivals but still suitable for conservative investors.

The company’s profitability is evident. It posted operating margins of 46.90% and profit margins of 32% in its latest quarter, showing quite a bit of pricing power, which is rare in the restaurant sector. For context, revenue in the third quarter of 2025 hit $7.08 billion—a 3% year-over-year increase—while profits rose by 1.60%.

McDonald’s has shown resilience, particularly in recovering from the pandemic. Revenue rose significantly from $19.208 billion in 2020 to $25.92 billion in 2024, with net income nearly doubling. With a market cap of $221.78 billion and a consensus target price of $331.20, Wall Street expresses confidence in McDonald’s stability. Still, aggressive buybacks have led to a book value drop of $3.04 per share, which investors should keep an eye on.

Fourth on the list is PepsiCo, though it’s facing concerns that growth investors might find troubling. In Q3 2025, it reported sales of $23.94 billion—slightly above expectations—and earnings per share came in at $2.29, which was also a bit better than anticipated. Despite this, net profits fell by 11.16% compared to the previous year, the biggest revenue drop among these stocks.

What makes PepsiCo compelling for retirees is its steady business model and commitment to dividends. The company disbursed $7.6 billion in dividends in 2025, maintaining payments despite profit decreases. Recent sentiment from Reddit’s dividend-focused investing community seems quite positive.

Looking ahead, PepsiCo anticipates low single-digit growth in organic revenue in 2025, a realistic forecast considering challenges in consumer spending. Its diverse portfolio consistently generates cash flow, regardless of economic shifts.

Coca-Cola holds third place, displaying a dividend yield of 2.87% and paying out $2.015 per share annually. The company’s beta of 0.39 ranks as one of the lowest, indicating limited volatility relative to the market.

For Q3 2025, Coca-Cola exceeded expectations with revenue of $12.41 billion and earnings of $0.86 per share. Year-over-year sales grew by 5.07%, and net income jumped by roughly 29.78%. Management anticipates full-year organic revenue growth between 5% and 6%.

Technical indicators suggest it might be a good time to buy, with Coca-Cola’s Relative Strength Index currently at 48.91. It recovered from a previously oversold condition, which is a good sign.

Johnson & Johnson comes in second as a true dividend aristocrat, offering a yield of 2.52% with an annual dividend of $5.08. The company’s beta of 0.35 ensures robust stability, and its AAA credit rating further reflects strong financial health.

Recent sales results bolster confidence, as third-quarter 2025 revenue reached $23.99 billion, surpassing expectations. Earnings were equally impressive, with a significant year-over-year net income surge.

The company’s dividend history is stellar, having raised its quarterly dividend by 4.8% from $1.24 to $1.30. Over the last five years, dividends have increased at a compound annual rate of 6.5%, outpacing inflation comfortably.

Verizon occupies the top position for retirement investors seeking consistent income, with an annual dividend of $2.723 per share and a robust yield of 6.59%. Its beta remains the lowest among these six stocks, underscoring its stability.

Verizon’s dividend track record is commendable, having raised it for 19 consecutive years. The company just increased its quarterly dividend to $0.69—a 1.9% hike. Although the five-year annual growth rate is around 3.4%, which is below the inflation rate, the initial yield compensates significantly.

For Q3 2025, Verizon reported revenue of $33.82 billion, just shy of expectations, although net income surged 50% year-over-year. Future revenue growth for wireless services is projected between 2% and 2.8%.

However, the major concern lies in Verizon’s hefty debt of $170.45 billion, which certainly needs careful management. That said, the company’s essential services provide predictable cash flows, allowing it to maintain dividend payments through various economic conditions. For retirees focused on immediate income rather than growth, Verizon’s high yield combined with low volatility makes it a standout in the realm of dividend stocks.

It’s easy to think that retirement planning is merely about choosing the right stocks and ETFs, but there’s more to it. Distinguishing between accumulation and distribution is essential, and it can really change the game.

The good news is that, by asking a few simple questions, many people have assessed their portfolios and discovered they could potentially retire sooner than they originally thought. If you’re contemplating retirement—whether for yourself or a loved one—perhaps spend a moment reflecting on this. It might just lead to some surprising insights.