Understanding Alpha and Beta in Investing

Many in the investment world tend to think that alpha, or the ability to outperform the market, is the Holy Grail for investors. It makes sense, right? Generally speaking, more alpha is better than less.

But alpha doesn’t always equate to better investment outcomes. Why? Well, because alpha is, in a way, always relative. The state of the market matters, and if it’s not performing well, having alpha might not be enough. Let’s consider an example to illustrate this point.

Picture two investors: Alex and Pat. Alex is exceptionally skilled and consistently beats the market by a margin of 5% annually. Pat, unfortunately, tends to have pretty bad investment results. Now, if the market grows by 5% each year, Alex will be ahead of Pat by 10% every time they invest together.

But what happens if Pat starts investing after Alex? Could there actually be a scenario where Pat outshines Alex despite the latter’s expertise?

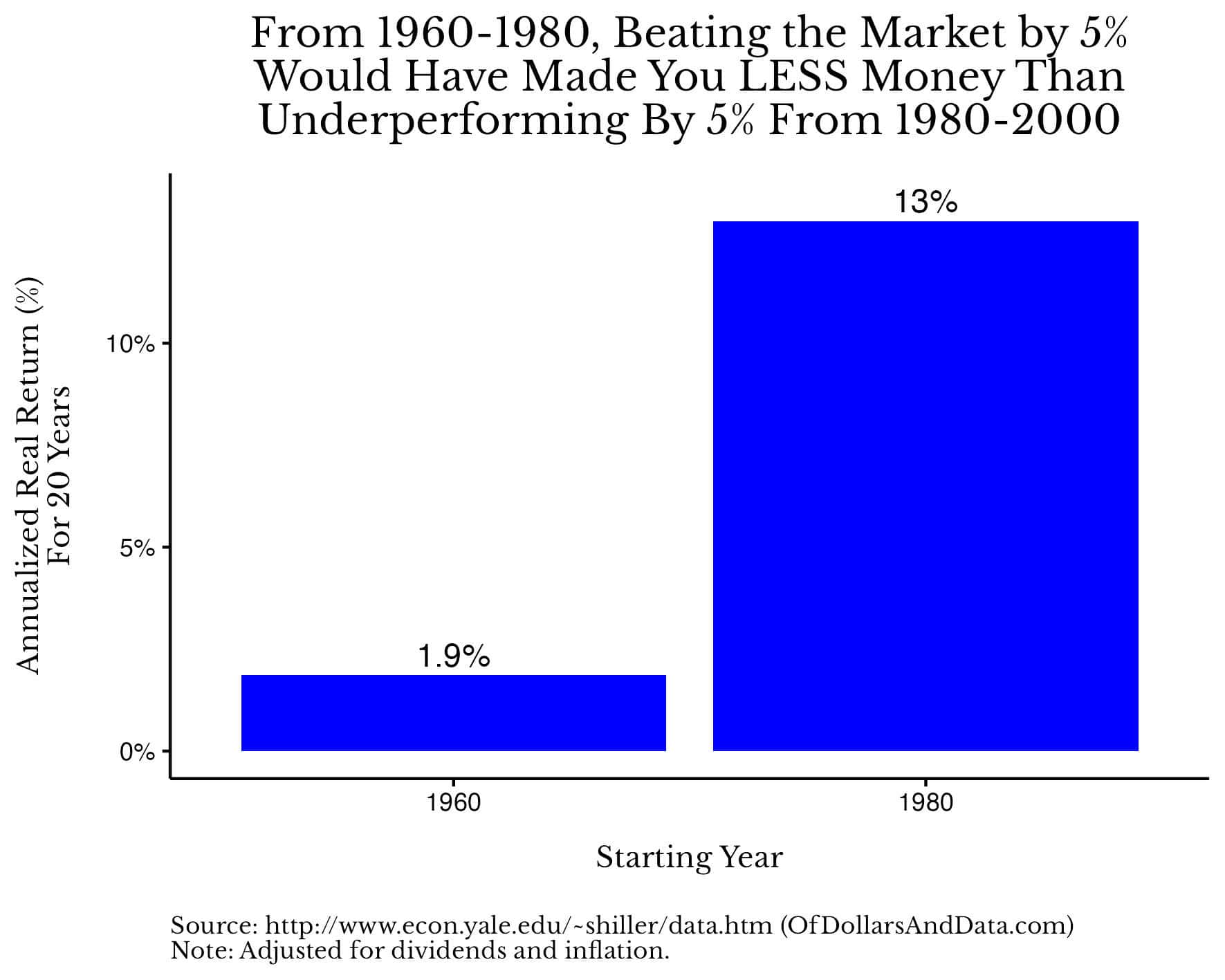

Surprisingly, yes! If we imagine that Alex invests in U.S. stocks from 1960 to 1980 and Pat jumps in from 1980 to 2000, it turns out that Pat could outperform Alex two decades later. This is shown in a previous graph that compares the 20-year real annualized returns of U.S. stocks during those periods.

In this scenario, Alex sees a return of about 6.9% (which is Alex’s 5% alpha plus the market’s performance), whereas Pat’s return from the later period is around 8% after adjusting for inflation, despite being the weaker investor. Somehow, Pat’s performance still manages to outstrip Alex’s.

Now, let’s think about a more genuine competitor for Alex. Until now, we’ve been discussing investors who are trailing behind by 5% annually. However, the reality is that Alex would typically be competing against index investors, who tend to match the market returns.

Under these circumstances, while Alex might outperform the market by 10% in one period, he could fall behind an index investor in another. This might seem like a bit of an outlier example, but it highlights how often alpha can lead to lesser performance compared to historical norms. A related chart depicts how frequently index investors underperformed over 20 years from 1871 to 2025, hinting at the degree of alpha involved.

Looking at the data, when there’s no alpha (0%), your chances of lagging behind the index are roughly 50%. Yet, as your alpha increases, the odds of underperforming drop, although not as dramatically as you might think. Even with a 3% annualized alpha over 20 years, there’s still a 25% chance of falling short of the index.

Some folks might argue that only relative performance matters—I get it—but I see things differently. After all, would you rather gain from the market’s ups and downs during stable times or just aim to have some positive alpha through turbulent times like the Great Depression? You’d likely prefer the solid market returns, right?

Typically, if you stick with index returns, you should end up performing decently over the long haul. The real annualized returns for U.S. stocks across decades show that—while there are fluctuations—they tend to be mostly positive. Just keep in mind that the returns for the 2020 decade only reflect numbers up until 2025.

This discussion really reinforces that investment acumen is important, but understanding market trends (or beta) is crucial. So, be mindful of beta over alpha.

Just to clarify, β (“beta”) measures how much an asset’s return is expected to fluctuate in relation to the market. For instance, if a stock has a beta of 2, that means if the market increases by 1%, the stock is projected to rise by 2% (and vice versa). For the sake of simplicity, we often refer to the market return as beta (you know, beta 1).

The good news is that even if a market doesn’t provide enough “beta” in one particular period, it may do so later. A chart depicting the 20-year annualized real returns for U.S. stocks from 1871 to 2025 illustrates this concept well.

This chart shows how returns can dramatically rebound following a period of downturns. For example, if one had invested in U.S. stocks in 1900, the real annualized return for the next 20 years would hover near 0%. Conversely, an investment made in 1910 would lead to a return closer to 7%. Interestingly, those who invested just before the market crash in 1929 saw a mere 1% annual return, while those who entered the market in mid-1932 enjoyed around 10% each year.

Such significant variations underscore the impact of overall market performance (beta) compared to individual investment talent (alpha). You might wonder, “If I can’t control the market, why does this matter?”

Well, it matters because it grants you freedom. It allows you to concentrate on what you can control instead of fretting over market fluctuations. See it as one less item to fixate on or optimize. After all, you can’t control everything.

So, what can you manage? Think about your career, the rate of your savings, your health, your family…all these factors add far more value to your life than simply trying to gain a few percentage points in your investment portfolio.

A small raise or a strategic job move could boost your lifetime earnings by six figures or more. Maintaining your health can substantially lessen future medical expenses. Being present for your family can leave a lasting impact on their future. Indeed, the benefits from such life choices often outweigh what most investors could hope for in returns.

Trust me on this. In 2026, let’s focus on the right things and hope for beta, not just alpha.

Thanks for taking the time to read this.