Chipmakers Drive S&P 500 Gains, but Concerns Arise

Chipmakers are becoming significant players in the S&P 500 index, pushing stock values to new heights, yet this surge has raised questions about how sustainable these gains really are.

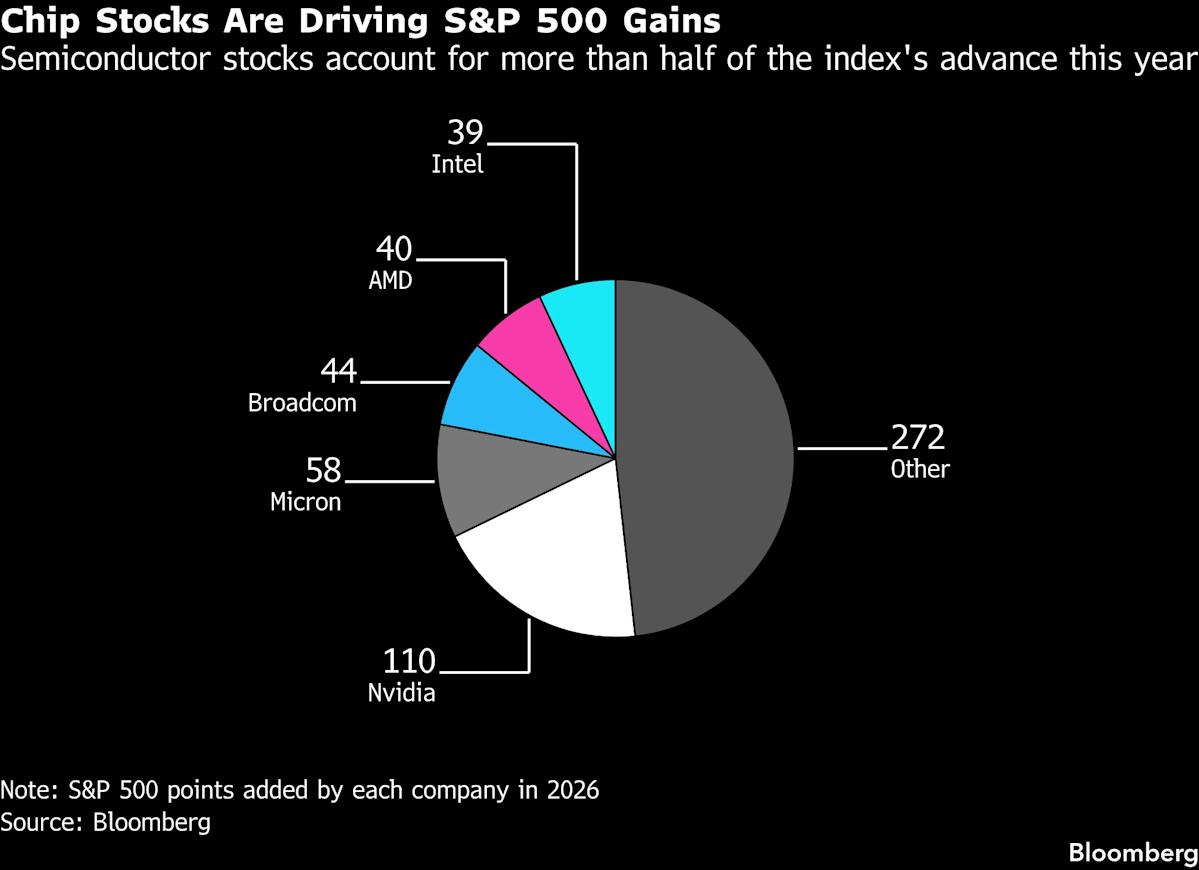

On Friday, a market selloff highlighted these worries, with the S&P 500 dropping 1.2%—its steepest decline since March—while the chipmaker index saw a 4% drop. For most of 2026, the performance of major semiconductor companies has contributed significantly, with a few firms helping secure more than half of the S&P 500’s 8% increase this year. Notably, Nvidia remains a standout in the bull market, alongside SanDisk, whose stock has sky-rocketed by nearly 500% this year, and Micron Technology, which has more than doubled its share price.

This rally has been powered by a soaring demand for chips, especially for artificial intelligence applications, even amid geopolitical tensions and increasing oil prices. Currently, semiconductor stocks represent 18% of the S&P 500, the highest in over two decades. Such concentration might heighten the risk of a broader market downturn if momentum shifts or if chip demand decreases—something that often happens in this industry, known for its ups and downs.

“When returns become this concentrated, it makes the market more vulnerable to sudden shifts,” said Keith Lerner, an investment chief at Turist Advisory Services. “Nothing can keep climbing in a straight line eternally, even if the fundamentals are there.”

As it stands, there seems to be little indication that the robust spending that has fueled this rally will taper off anytime soon. Major tech companies like Amazon, Microsoft, Alphabet, and Meta Platforms are looking to spend close to $700 billion on capital investments this year alone, with estimates putting capital expenditures near $5 trillion over the next five years.

For now, profits in the tech sector remain strong, with first-quarter earnings projections for S&P 500 companies showing an expected 84% increase compared to last year. In particular, Micron, the biggest memory chip maker in the U.S., is anticipated to see its profits skyrocket by 670% to reach $65.8 billion in 2026.

“As long as earnings maintain this upward trend, I’m not overly worried,” said Jeffrey Blazek, co-chief investment officer at Neuberger Berman Group. “Revenues are increasing alongside these gains, and there’s no indication of slowing down.”

Many investors share the belief that the rise of AI across the economy could potentially stabilize this boom-bust cycle, as consistent growth in computing demand presumably keeps chip sales steady.

“We might have underestimated the computing power needed for AI, but we aren’t there yet. The demand is immense,” noted Anna Rathbun, founder and CEO of Grenadilla Advisory. “This perspective gives us confidence in our revenue growth, especially in the infrastructure field.”

Still, semiconductor companies tend to be more affected by economic cycles compared to larger tech companies like Alphabet and Apple, which have diverse operations and strong market positions. Typically, a surge in semiconductor demand is followed by a downturn, leading to decreased pricing power and profit margins.

Timing such market transitions can be challenging for investors, often ending in sudden drops. In fact, during the 2022 tech bear market, the Philadelphia Semiconductor Index plummeted nearly 50%, with Nvidia seeing a nearly 70% decline. Comparatively, the Nasdaq 100 Index dropped around 36%, although some major tech firms fared better.

Despite current uncertainties, the market remains unpredictable. Recently, investor Michael Varley, known from “The Big Short,” suggested cutting back on tech stock investments, comparing the market to a “bloody car crash moments before it occurs.”

Similarly, Jonathan Krinsky, chief market technologist at BTIG, noted that he anticipates a more than 20% drop in the semiconductor index after its rapid rise.

Even those bullish on the sector acknowledge its cyclical nature, yet many, including Neuberger’s Blazek, believe there still may be room for growth. “Hyperscalers have been steadily increasing their capital expenditures, but there will likely come a time when we see a stabilization or a reversal,” he said. “That’s typically when we experience a marked correction in the chip industry.”