Dutch Brothers (New York Stock Exchange: Brothers) The stock is rapidly approaching a 52-week high following a strong first-quarter financial report. Tuesday’s update to investors showed the coffee chain beat consensus revenue estimates for the fifth consecutive quarter. After growing 12% in 2023, mid-cap Starbucks (NASDAQ:SBUX) Challenger is up another 13.8% year-to-date.

Headquartered in Oregon, Dutch Brothers operates and franchises drive-thru beverage shops with a focus on quality, speed and service. The company sells its signature coffee and Rebel energy drinks in 876 stores in 17 states.

Dutch Bros. encouraged investors by announcing same-store sales for the first quarter of 2024 rose 10% year-over-year due to higher customer counts and increased ticket sizes. This performance built on his strong fourth quarter of 2023, where same-store sales increased his 5%.

I’m bullish on Dutch Bros. as a long-term growth story for the restaurant industry. According to recent research, technomic ignite Dutch Bros. has revealed itself as America’s third most popular restaurant chain thanks to its unique menu and customer service. Starbucks’ strong start to 2024 is especially impressive after the company reported a 2% sales decline in its most recent quarter and warned of slowing demand in the U.S. and China.

The market’s caffeinated reaction to Dutch Brothers’ first quarter releases couldn’t have come at a better time. As you can see in the chart below, Dutch Brothers stock had been declining for seven consecutive weeks before its recent rally. Is this the beginning of a long reversal?

Let’s take a closer look at first-quarter numbers, management’s full-year outlook, and the latest predictions from Wall Street.

Dutch Bros. opens record number of stores in first quarter

First-quarter revenue increased 39% to $275 million, driven by a record number of new locations. Dutch Brothers opened 45 of his stores during this period, most of which were fast-growing company-operated stores. This was the 11th time, matching the previous record.th At least 30 new stores have opened in consecutive quarters.

Dutch Brothers backed up its top-line numbers with strong profit metrics. The gross profit margin of in-house operations expanded by a whopping 520 basis points. Furthermore, while other companies in the industry are struggling with rising labor costs, SG&A expenses were relatively flat compared to the same period last year. As a result, Dutch Brothers achieved adjusted net income per share of $0.09, beating the consensus estimate of $0.02.

CEO Christine Barone commented that customer trends were “particularly encouraging” after traffic improved in each of the past two quarters. This is likely a result of the brand’s strong association with Gen Z consumers, who have embraced the chain’s trendy drinks. After bringing back its popular Chocolate Crunch Cold Brew last year, Dutch Bros. launched protein milk coffee and several poppin’ boba coffees, teas and energy drinks this year.

Dutch Bros. also benefits from increased brand loyalty. 66% of his transactions in the first quarter came from members of the Dutch Rewards loyalty program, an all-time high. For restaurant chains, increasing brand awareness and loyalty is usually a winning formula.

Management strengthens outlook for 2024

Dutch Brothers doesn’t appear to be putting the brakes on its aggressive expansion strategy. The company plans to open 150 to 165 stores this year, bringing the total to more than 1,000 stores. Additionally, sales in 2024 are expected to be between $1.2 billion and $1.215 billion. Management had previously expected full-year sales of $1.19 trillion to $1.25 billion.

The company also raised its 2024 adjusted EBITDA forecast to $195 million to $205 million. Wall Street analysts expect this to translate to EPS of $0.36 for him. As a result, the P/E ratio of Dutch Brothers stock in 2024 will be approximately 100 times. There’s no question that this is a high valuation, but it’s one the market is willing to give the company at given its strong growth prospects and potential to take market share away from Starbucks.

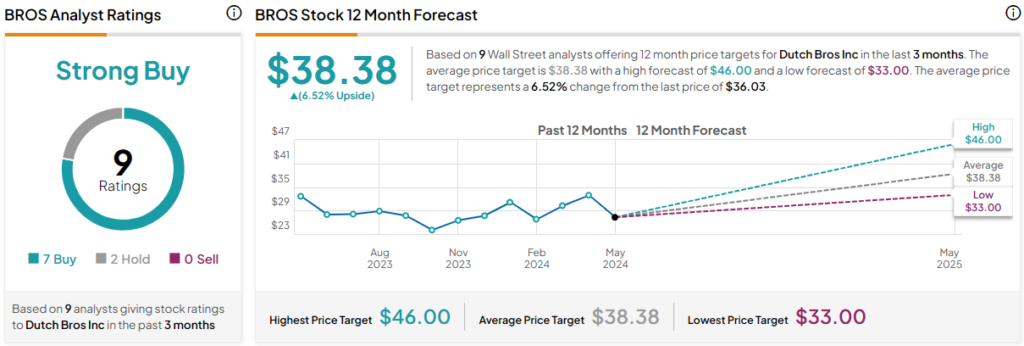

What is the consensus price target for BROS stock?

Dutch Brothers has a consensus rating of “Strong Buy” and an average price target of $38.38 for BROS. Given the post-earnings share price rally, this suggests limited upside from here (6.5%). However, as we saw on Friday, analysts’ price targets may be trending higher this summer ahead of the company’s second-quarter earnings release.

On Friday, TD Cowen five-star analyst Andrew Charles upgraded BROS from Hold to Buy. Charles set a price target for the stock at $46.00, which is currently the highest price on the market and represents a potential upside of nearly 30% over the next 12 months.

It will be interesting to see if a similar price target increase takes place, pushing the consensus target above $40.00. If not, a meaningful exit could be an entry point for BROS bulls.

BROS stock conclusion

Dutch Brothers posted strong growth in the first quarter, driven by healthy customer traffic and order trends. As a result, the stock has seen a correspondingly large rally, although it remains well off its 2021 IPO highs. Management’s continued aggressive expansion strategy could attract even more investors to this Gen Z favorite, which makes me bullish long-term.

disclosure