The U.S. economy hasn’t performed as well as it appeared so far this year and into early 2023, according to revised data released by the Federal Reserve.

The U.S. labor market added 818,000 fewer jobs in the 12 months ending in March, the Bureau of Labor Statistics said Wednesday, marking the biggest preliminary downward revision to U.S. employment data since 2009.

That means the reported job gains during that period (2.9 million nonfarm payrolls, or 242,000 per month), were probably about 30% lower, or 174,000 per month, according to new data compiled from state unemployment tax records.

The big cut falls short of the 1 million downward revision that some economists had feared, but it is well above a more optimistic forecast of 300,000, reinforcing worries that the Federal Reserve may have waited too long to start cutting interest rates.

“While this doesn’t dispute the idea that the expansion is continuing, it does suggest that we should expect slower monthly job gains, putting further pressure on the Fed to cut rates,” Robert Frick, corporate economist at Navy Federal Credit Union, said in a note.

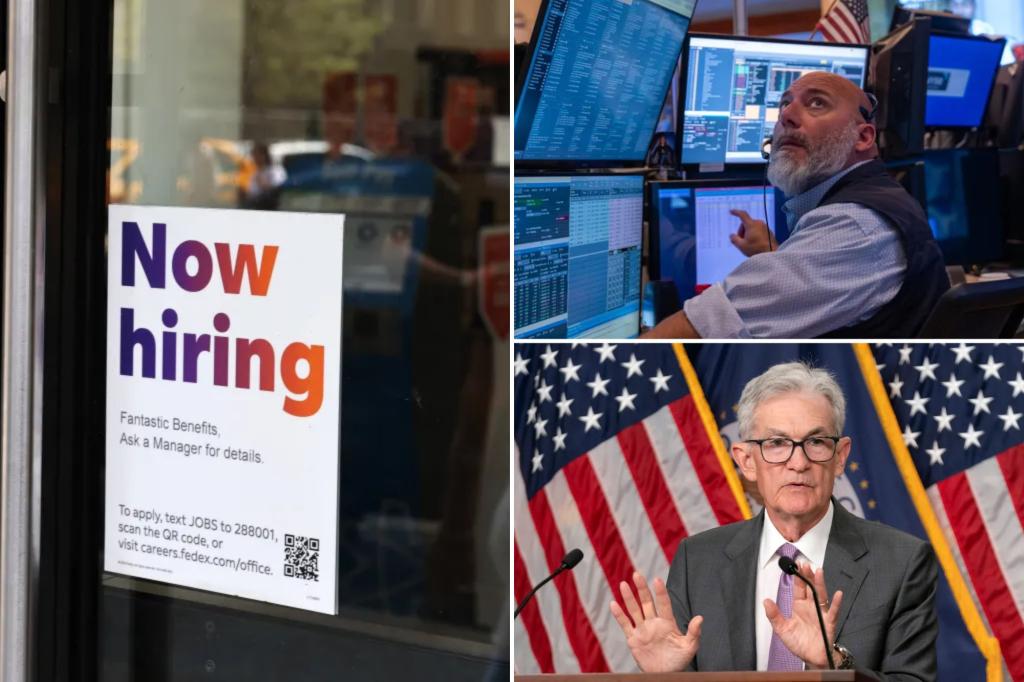

Federal Reserve Chairman Jerome Powell is expected to give further hints about the central bank’s interest rate cutting plans in a highly-anticipated speech in Jackson Hole, Wyoming, on Friday.

Investors are now betting on a quarter-point cut when the Fed meets in September. Traders now see a 20% chance of a half-point cut.

The jobs report has become a political hotbed of contention as the 2024 presidential campaign enters its final stages.

Former President Donald Trump reacted to the downgrade on his Truth social account on Wednesday, calling it a “huge scandal.”

Earlier this month, weak July employment data sparked concerns that the nation’s labor market may not be as healthy as economists thought.

Meanwhile, the unemployment rate has risen for four consecutive months.

Wednesday’s report is part of the Labor Department’s annual process of updating its monthly employer survey with more comprehensive data from state unemployment tax records.

This update is provisional, with a final revision scheduled for February.

Goldman Sachs analysts had estimated the downward revision could result in a drop of as much as 1 million jobs, but noted that the figure had been revised upwards in February every one of the past four years.

Wells Fargo projected the report would see a job loss of at least 600,000.

The largest downward revision was in professional and business services, which lost 358,000 jobs.

The leisure and hospitality industry created 150,000 fewer jobs than last reported, while manufacturing jobs were revised downward by 115,000.

The trade, transport and utilities sector saw a downward revision of 104,000 jobs.

Several sectors saw upward revisions, including private education and health services (87,000), transportation and warehousing (56,400) and other services (21,000).

The BLS is revising its initial employment estimates, which typically rely on incomplete data and survey results from samples of businesses and households.

Benchmark revisions often come after officials scrutinize government documents, such as unemployment insurance tax records, which often reveal inconsistencies.

The Federal Reserve has been keeping interest rates high in hopes of taming inflation without tipping the economy into a recession, also known as a “soft landing.”