The war is over: not the war in Ukraine or Gaza – I mean the war with inflation.

Naturally, shoppers are still shaking around grocery aisles, and recently egg prices. Meanwhile, economists, politicians and critics continue to sweat what is called the “sticky” category of rising goods, services and wages, especially after the accelerated consumer price index in January.

They are all fighting the final war. How about you and your stock portfolio?

Yes, inflation has been attacking families since 2021, and it was horrifying. The CPI surpassed January 23.4% by December 2019. This puts the experience of many shoppers, including you, perhaps. It is also true that the end of a military war does not mean that destruction will be reversed in any way.

Unfortunately, the latter is also the case for inflation. price and inflation different. Inflation is the speed at which prices rise. Now it's 3% based on CPI a year ago. Prices do not fall overall. The selected category can drop significantly, but it will drop significantly (aka DEFL) Well, developed countries don't do that. why?

True deep deflation means depression – even more deadly war. Reversing the post-pandemic rise in CPI means it is close to the deflation of 1929-1933 or the recession after World War I in the early 1920s. Is that really what you want? I didn't think so. To win the war of inflation was not to lower prices, but to slow their progress.

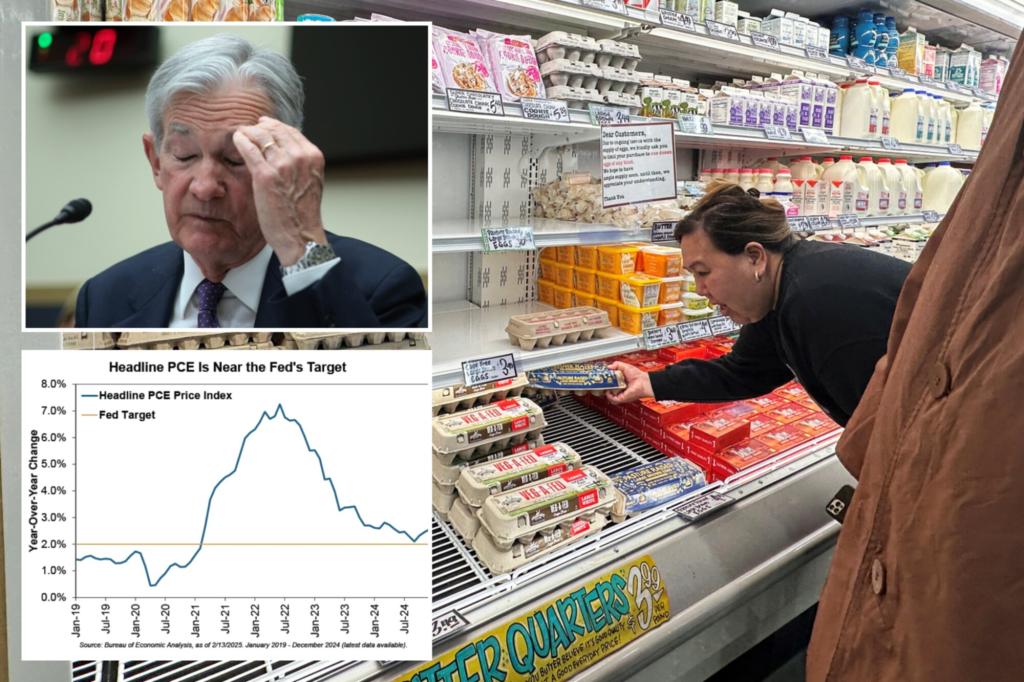

Last November, he detailed why the Federal Reserve wants a 2% year-on-year inflation. Since peaking at 9.1% in June 2022, CPI has cooled irregularly to 3.0% in January. Despite all the yucking about acceleration, it is 0.1% ahead of December. Statistical blips. Anyway, these measurements aren't that accurate.

Meanwhile, the December “Personal Consumption Expense Price Index” was 2.6% more than the year before, a broader measurement the Fed actually targeted. Critics cried it was “stuck” more than the 2% target, promoting all the worrying shaking. However, there is no evidence that the Fed can tweak anything exactly – none, zero, zip -.

Oddly, “stubborn shelter” inflates the CPI. However, this is mainly from fictitious “owner equivalent rent” calculations. It is a guess that Goofball government statisticians will pay to rent a home. No one pays for this.

Excluding the shelter, the December CPI was 1.9% compared to last year –include Eggs spun like birds. The Fed doesn't want it to be much lower. So don't expect that. However, the “war” is over.

Inflation is simply a case of too much money chasing too little goods or services. It comes with a time lag caused by the Fed – the growth rate of money supply beyond GDP growth rate.

During the Covid chaos of the 2020s, the Fed silly burned its strangely bulging money supply. The widest gauge, the M4, rose 30.9% year-on-year in June 2020. M2, narrow, reached 26.6% in February 2021. After that, the price was galloped.

The Fed has slowed, growing money supply at 3.4% and 3.9%, respectively, for most years and under since the 1980s. Attracting approximately 2% annual GDP growth, we see inflation of less than 2%.

Are you worried about wage growth? Last August, I explained in detail why it's not inflation and why it can't be done. I don't rehash it now – it was a long column, you can look it up. But it seems that economists, politicians and critics never learn.

What about President Trump's tariffs? Again, the key here is that tariffs do not affect money supply. Tariffs can raise some prices, but they are much smaller than most people think. Mainly, tariffs raise some prices while enforcing others. Customs channel demand, creating winners and losers.

Yes, tariffs are poor economic policy. But inflation is not a reason. Think about all the inflation that Trump's first term tariffs didn't get.

So, what is the unundervalued, non-inflated truth for investors? I hate bursting some bubbles here, but market forecasts require you to see something big that others aren't. It's not helpful to huff and breathe about inflation along with an army of “experts.”

The war of inflation is over, a complete halt. Be strong.

Ken Fisher is the founder and executive chairman of Fisher Investments, a four-time New York Times bestselling author and an official columnist from 21 countries around the world.