One of the major pitfalls faced by new retirees is the sequence of risk of return. This is the risk that losses early in the retirement year will put their ability to save to maintain their spending until the end of the year. The concept is that it is an informed job that was done as part of a popular “retirement income status” study written recently by colleagues Amy Arnott, Christine Benz, Tao Guo and Jason Keffert.

One question asked by research readers was when the sequencing risk decreases. Are there any points that the retirees can exhale as they are far enough along the journey to ensure that the risk of the sequence is safely behind them?

Visualizes sequence risk

To address this, I asked Tao Guo, one of the authors of the study, to extract data from the scenarios that are most filled with the risk of returns. When a retiree invests fully in stocks. Stocks are more volatile than bonds, so if retirees invest in stocks alone, the risk of early retirement losses is even more severe.

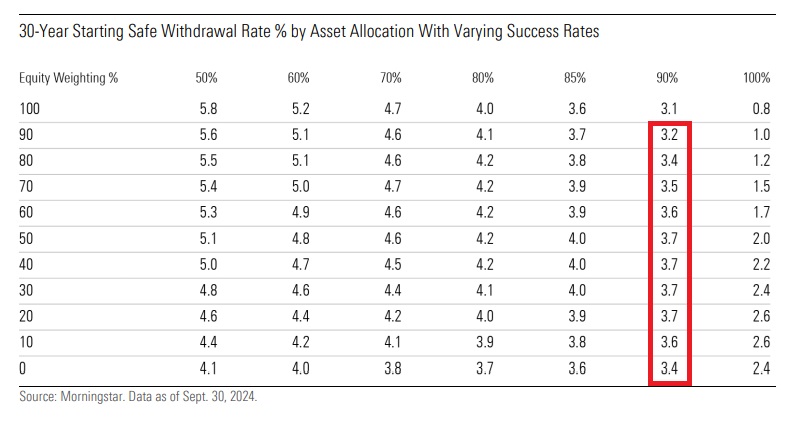

In this study, TAO and his co-authors found that this all-capital portfolio could support a 3.1% starting spending rate for retirees who make actual withdrawals fixed annually from the investment portfolio (assuming that the funds remain at the end of the expected 30-year retirement period).

We focused on 10% of simulated random trials in which retirees ran out of savings before the end of their retirement, and saw whether a number of those “failures” were involved in early investment losses in retirement. It turns out that nearly 70% of these “failures” are related to trials where retiree investments have lost value by the end of five years of retirement.

We also looked at it the opposite way by ranking trials based on simulated returns for the first five years of retirement and seeing how failure rates change. For example, we assigned 20% of the lowest return tests to the “bottom” quintile, recording the number of failed tests, etc. When returns were insufficient in the first five years, the risk of exhausting retirement savings was much higher.

When is the coast clear?

It establishes that the first five years of retirement are crucial to success or failure, but does that mean if you escape the first five years that are clear, unharmed? There is not at all. After all, if 70% of the failures were related to exams incurring losses in the first five years, by definition, the other 30% would have acquired the investment in the early years, but subsequent spending and losses in investment depleted the retirement savings earlier.

So the question is, how did early retirement allowances make way for later losses? Has this, combined with ongoing spending, dried up retirement savings? The good news is that it's pretty unlikely. After the first five years of retirement with the return on investment, there was only about one in 25 chance of draining savings before reaching the end of retirement. Even after a year of retirement, profits reduced the risk of failure by half.

Was there a point of retirement when the sequence risk was completely in the rearview mirror? It depends on how you define the sequence risk. Defining failure as a loss due to a loss in the first five years of retirement and focusing on trials that avoided losses at any point in the first five years, the risk of failure will be reduced to about 1% by the tenth year of retirement.

It did not completely eliminate the risk of failure. Losses over the next few years could, after all, prove to be as deadly as the first five losses, depending on their depth and duration, but less common about losses other than retirements in the first five years of the plan.

Investor takeout

It is clear that the first year of retirement is important to ensure that retirement savings can go far. Our research shows that if a retiree emerges from the first five years of unharmed retirement due to loss, he significantly reduces the chances of exhausting his savings early.

Given this, we recommend that retirees diversify their portfolios to mitigate the risk of early retirement losses that could threaten their savings ability to maintain their spending over the expected 30-year horizon.

This is clear from the retirement income survey itself. This found that diversifying from stocks away from bonds led to more income from retirement savings funds. This is because bonds act as shock absorbers, reducing the risk of volatility and losses in previous years, and promoting increased spending.

Most new retirees are probably sitting in the profits of their investments now and are given an upward trend market, but that is clearly not true forever. In the future, new retirees whose investments have been sold may be at a higher risk of running out of savings depending on the spending rate. In such a scenario, it makes sense to reclaim spending, if only for a while, while using one of the flexible withdrawal approaches the author explores in his research.

It's turned on

Here are things I write about, read, hear, and see.

- Amy Arnott, whose stocks have mostly destroyed shareholder value, and Christine Benz on how to narrow down retirement incomes more than 3.7% after inflation

- Ben Carlson: “I have my hero.”

- “Blame Game”: When Adam Grossman will know Passive Investment Too big

- McKinsey & Co. on The looming shortage of financial advisors

- Berkshire Hathaway Shareholder letter

- Slow horse

- Karen O and Dangerous Mouse: “Super Bracelet”

Don't be a stranger

I love contacting you. Do you have feedback? The angle of the article? Email me at jeffrey.ptak@morningstar.com. If you're so leaning you can also follow me on Twitter/X @syouth1and I write some odds and ends on a substance called cold Basic indicators.