A small but growing number of employers are handing over the decision of health insurance directly to their employees. Rather than offering traditional insurance plans, these companies provide funds for workers to purchase their own coverage. This method is referred to as individual coverage health reimbursement arrangements (ICHRAs).

Proponents argue that this approach can be particularly beneficial for small businesses that don’t have their own insurance plans. It aligns with conservative goals by easing the financial burden on employers while empowering employees to choose what best suits their needs.

However, there’s a notable downside. Employers might find it challenging to ensure their workers are compensated fairly, as this model requires employees to shop for their own insurance, a task many are not fond of.

“It’s not a perfect solution, but it addresses a real issue for many,” noted an expert studying healthcare trends.

Typically, U.S. employers offer health insurance through group plans, where they cover a large portion of the premium costs. In contrast, ICHRAs allow employees to select their own insurance plans, with employers contributing a fixed amount toward coverage. This model, which was introduced during the Trump administration, has recently gained traction.

So why is ICHRA significant? It allows business owners to predict their costs and eliminates the need to make insurance decisions on behalf of their employees. For small businesses, this can minimize vulnerability to volatility in annual insurance costs, especially concerning employees with costly medical needs.

The range of contributions can vary significantly based on employee demographics, sometimes exceeding $2,000 monthly.

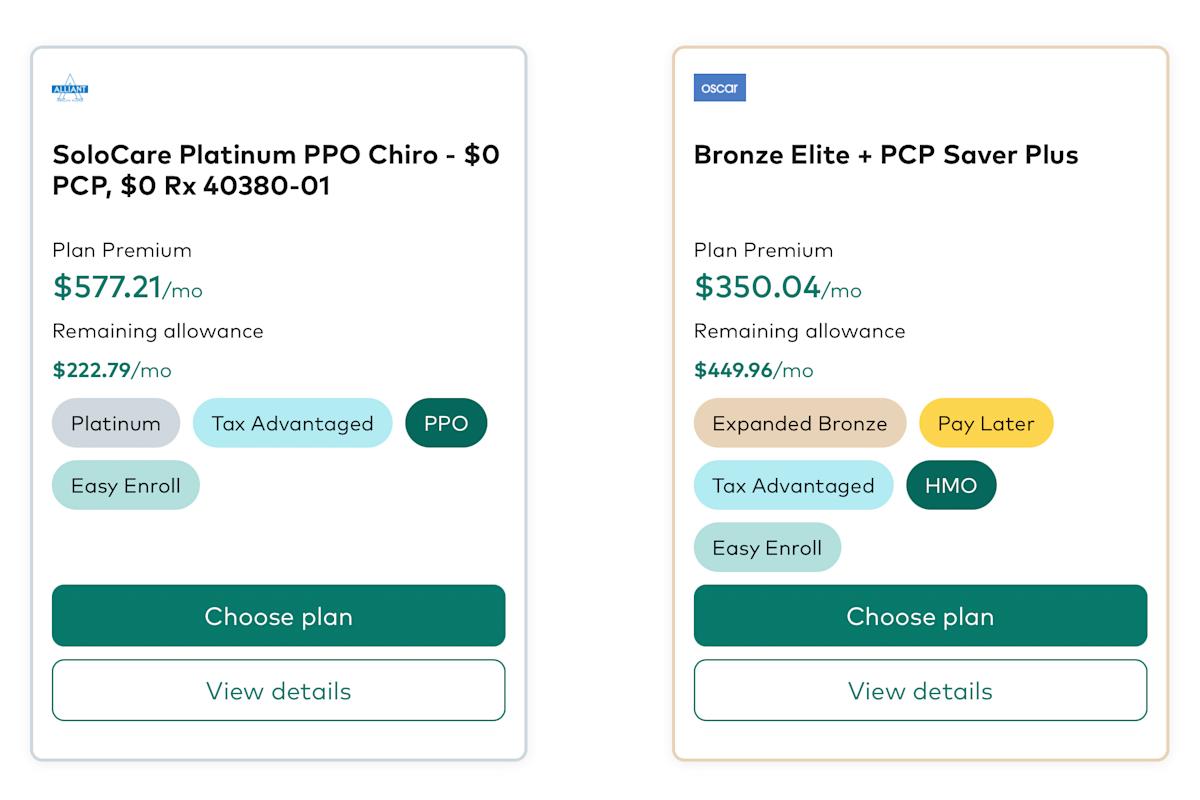

This model diverges from traditional offerings by providing access to a broader range of options in the individual insurance market, which could lead to more tailored coverage for specific needs — for instance, plans that cater to diabetes management.

Furthermore, if employees leave their jobs, they can keep their insurance coverage longer than with standard employer-sponsored plans. They may need to cover the full premiums, but they retain continuity in treatment with their existing doctors.

The CEO of Oscar Health mentioned that many people switch jobs frequently. “Insurance tends to be most effective when it stays with the individual,” he remarked, highlighting the advantages of ICHRAs.

Yet, there are challenges. Individual health insurance plans often have narrower networks compared to group plans, which can create difficulties for those needing to see multiple specialists.

Individuals navigating their own insurance options may encounter overwhelming complexities, making it essential for employers to assist in guiding their choices.

While there’s no clear national statistic on enrollment with ICHRAs among small businesses, there has been notable growth in this sector. An industry council promoting ICHRAs reports that around 450,000 individuals have been enrolled this year, reflecting a significant rise since 2024. However, this still represents a fraction of the total employer-sponsored health insurance market in the U.S.

The future of ICHRAs might depend on several factors. As healthcare costs continue to escalate, more businesses may look to limit their financial exposure. There are ongoing discussions about possible tax incentives related to such arrangements.

Additionally, if government subsidies that assist with purchasing insurance in individual markets expire, more individuals could qualify for ICHRAs. However, those already benefiting from subsidies will not be eligible for these arrangements.