Palantir’s stock continues to outperform the general market, but can it sustain its success in the upcoming months?

Aside from Nvidia, it’s apparent that other companies haven’t reaped the same benefits from the AI boom as Palantir Technologies (PLTR). In the past three years, Palantir’s share value has skyrocketed by over 1,300%. This year alone, the stock has seen a staggering increase of 97%. In comparison, the S&P 500 and Nasdaq Composite have yet to even hit a 10% gain in 2025.

As tempting as it might be to chase these profits, savvy investors know there’s more to it than just wishful thinking.

This article will delve into the factors fueling Palantir’s remarkable growth and analyze recent trading patterns to determine if its stock can reach even greater heights.

A remarkable ascent for Palantir

When AI began emerging as a key trend in late 2022 and early 2023, investors often focused on major tech firms. Microsoft invested $10 billion in OpenAI, which created ChatGPT, while Amazon and Alphabet put significant funds into the competing Anthropic. Tesla showcased advancements in self-driving technology and humanoid robots. You get the idea—AI developments have primarily been spotlighted through the actions of tech giants.

Yet, behind the scenes, Palantir was quietly advancing. In April 2023, the firm introduced its fourth major software suite, the Palantir Artificial Intelligence Platform (AIP).

The graph indicates that before AIP, Palantir was considered a slow-growing company with high cash burn. However, since the launch of AIP over two years ago, revenue growth has significantly accelerated. Furthermore, Palantir has shifted to positive net profits, generating billions in free cash flow.

At the close of 2022, Palantir had 367 customers. By the end of the first quarter of this year, that number had doubled to 769. Notably, the count of commercial customers (non-government) has surged over the years.

For me, AIP is a pivotal tool for Palantir to broaden its influence beyond military contracts, which it’s most recognized for. This shift marks a transformative move from being a defense contractor to a more universal software provider, similar to Salesforce or SAP.

As an optimistic Palantir supporter, I’ve been impressed by management’s consistent ability to surpass growth expectations. However, I can’t help but question if the current stock performance is sustainable.

What’s Wall Street saying?

Investors can enrich their analysis by paying attention to insights from Wall Street analysts and observing the trading decisions of notable investors. Utilizing Form 13F, investors have access to detailed information on hedge fund transactions each quarter.

In the first quarter, well-known investor Stanley Druckenmiller fully exited his Palantir position, and Kathy Wood also reduced her stake in her Ark portfolio.

On the other hand, billionaires Ken Griffin and another Israeli investor have both increased their holdings in Palantir during the same period. With these mixed signals, it can be tricky to gauge Wall Street’s true sentiment toward the stock.

There are nuances here worth noting. Both Druckenmiller and Wood have fluctuated in and out of Palantir before; this isn’t their first time adjusting their stakes in this analytics firm.

Moreover, I think we should view Griffin and the other investor’s actions cautiously. Their firms engage in complex trading strategies, and there’s a chance that part of this buying activity relates to market-making.

It might look bullish that Palantir is part of Griffin’s Citadel and the UK’s Millennium Management portfolio, but I’m not completely convinced. These funds aren’t typically known for holding positions long-term.

Additionally, considering the volatile nature of growth stocks like Palantir, multi-strategy funds like Citadel and Millennium likely employ more intricate hedging strategies.

Where might Palantir shares end up by late 2025?

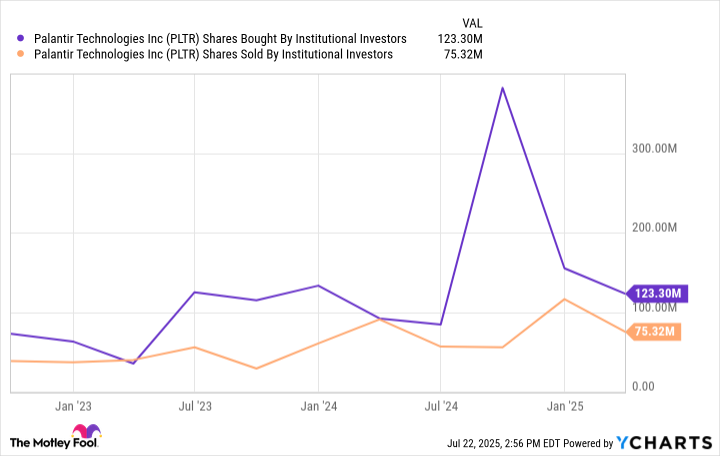

The chart below showcases trends in institutional purchasing and selling of Palantir shares over recent years.

As seen, buying activity (represented by the purple line) is on the rise, while sales (shown by the orange line) are relatively stable, implying Palantir remains a popular choice among institutional investors. That said, not every hedge fund or money manager has the same game plan—some of these purchases may be part of broader, more intricate trading strategies rather than a commitment to long-term investment.

In recent months, Palantir stocks have grown quite expensive, trading at levels exceeding those during the peak of the dot-com and COVID-19 booms.

It’s hard to predict exactly where Palantir shares will stand by year-end, but investors recognize that nothing can rise indefinitely.

The upcoming second-quarter revenue report should provide a clearer picture of investor sentiment. It’s worth remembering that after the stellar first-quarter report, the stock initially took a hit. With rising expectations after each report, it wouldn’t be surprising to see some selling pressure on Palantir stock again.

Given the current mix of buying and selling by institutions and Palantir’s heightened valuation, I feel the need to be cautious right now. A valuation correction seems likely sooner rather than later, and by year-end, the stock might be trading at a more reasonable price.