US Bitcoin ETF Sees Significant Inflows

On May 19th, Exchange-Traded Funds (ETFs) related to Bitcoin experienced a substantial inflow, amounting to $667.4 million, marking the largest daily total since May 2nd. The notable data comes from investments into the iShares Bitcoin Trust (IBIT), which alone accounted for nearly half of these inflows, totaling $306 million, thus contributing to a net inflow of $45.9 billion.

This renewed demand—evident from Bitcoin’s impressive price movement—has restored market confidence, as Bitcoin traded above $100,000 for an impressive eleven consecutive days.

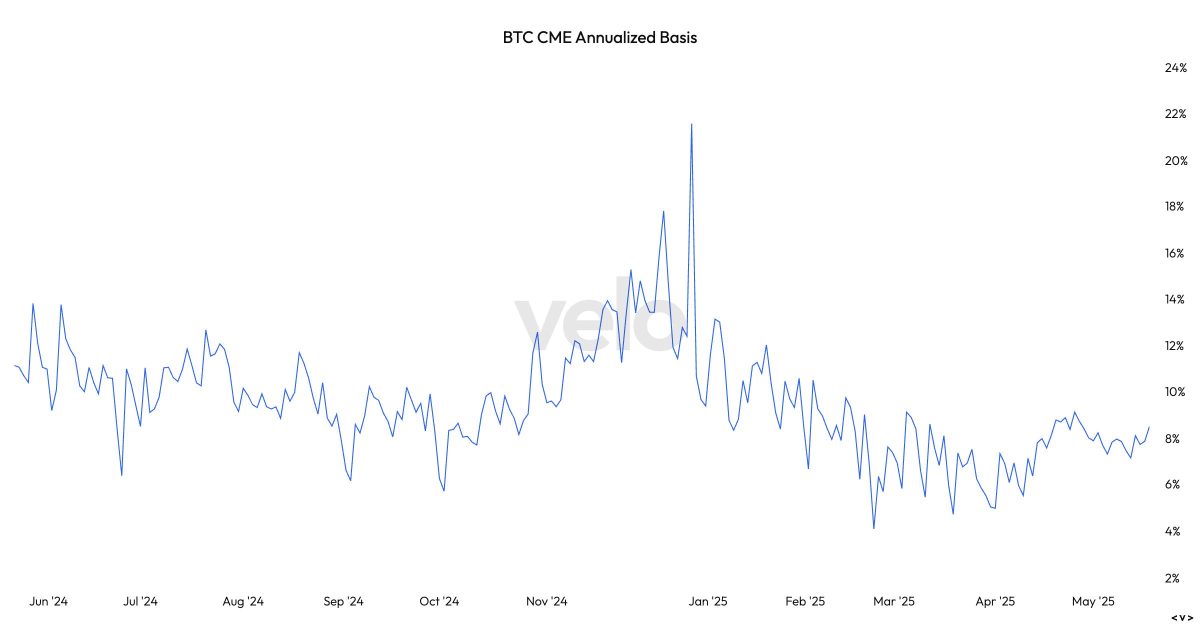

Moreover, annual trading strategies have evolved, making investors more inclined to stay with spot ETFs while simultaneously reducing their positions in Bitcoin futures contracts offered through CME. In fact, this approach has become increasingly appealing, showing a near doubling in what was observed back in April, approaching 9%.

According to VELO data, this uptrend has led to a slight uptick in underlying trading activities. Specifically, CME futures reached $8.4 billion on Monday, translating to about 80,000 BTC—the highest mark since April 23rd. Additionally, open profits registered at 158,000 BTC, increasing over 30,000 from the low seen in April, which emphasizes the growing interest in leveraging and arbitrage strategies.

Nevertheless, it’s still a far cry from the heights reached when Bitcoin peaked at $109,000 in January. This suggests that there remains considerable room for growth ahead.

The rising base indicates that a recovery might already be underway. It appears to be luring back some players who had exited the market earlier this year when the base dipped below 5%.

In an interesting development, a recent filing indicated that the Wisconsin Pension Commission opted out of its ETF position in the first quarter. This was likely in reaction to that favorable trading environment at the time. Given the subsequent data lag, where the basis spread expanded from 5% to nearly 10%, re-entering the market in Q2 to capitalize on improved arbitrage opportunities does seem plausible.