China’s Automation Dominance in Manufacturing

China has emerged as a leading force in manufacturing automation, boasting nearly ten times more factory robots than the United States, according to recent data.

Last year, over 500,000 industrial robots were operational in factories worldwide, and a striking 54% of those were based in China.

The International Federation of Robotics reports that China holds almost one-third of global manufacturing capacity and has installed a record 295,000 industrial robots in the past year.

In contrast, the US utilized only 34,200 robots, a 9% drop from the previous year, as noted in the World Robotics 2025 report.

This marks a notable shift, as Chinese manufacturers now account for 57% of the domestic robot market, surpassing foreign competitors for the first time.

China’s total stock of industrial robots surpasses 2 million units, with expectations of continued growth at about 10% annually through 2028.

Japan follows with 44,500 robots, with the US, South Korea, and Germany further behind.

In Europe, there has been an overall decline of 8%, while the Americas have seen a 10% drop.

Despite geopolitical and economic challenges, the IFR anticipates a 6% increase in the global demand for robots by 2025, reaching 575,000 units, and exceeding 700,000 by 2028.

China’s rapid adoption of robots is fueled by an impressive $1.9 trillion in state-led industrial lending. This shift in focus from real estate to manufacturing has led to a surge in both new factories and modernized older plants.

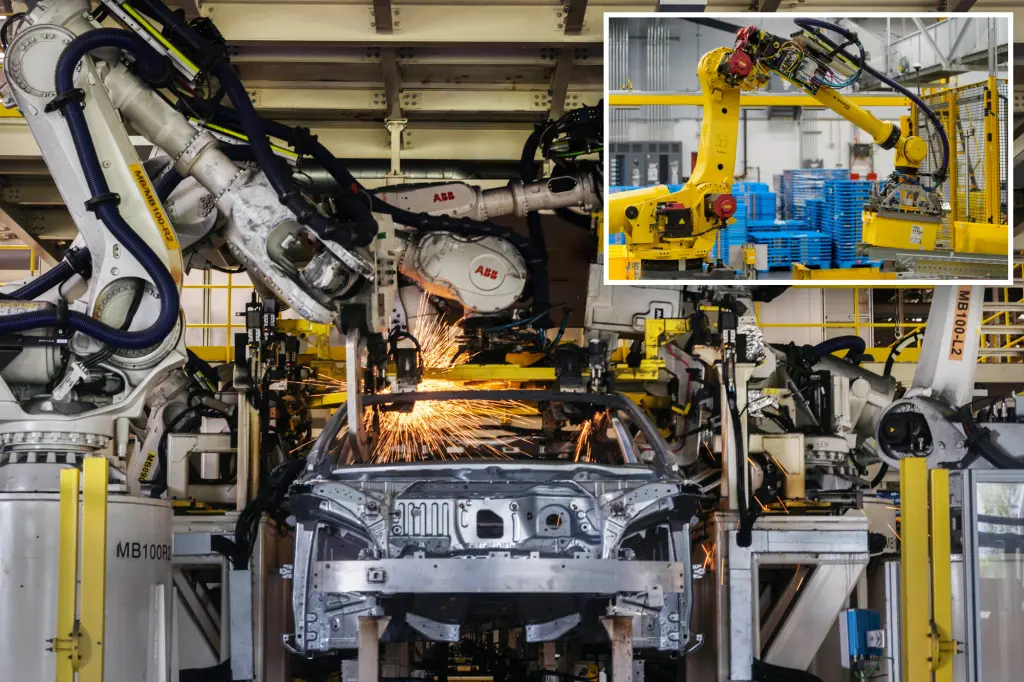

For example, the Zeekr electric car factory in Ningbo saw its robot count rise from 500 to 820 in just four years.

These upgrades across various sectors have contributed to a 13.3% increase in exports in 2023 and a further 17.3% jump in 2024.

Companies like Huawei are pushing this technological agenda, exemplified by their Shanghai Research Center employing 35,000 engineers.

Former US trade representative Katherine Tai has raised concerns that this might lead to significant disruptions globally, warning of “tsunamis” as Chinese exports increasingly penetrate markets, potentially causing factory closures and job losses around the world.

Analysts suggest that this robot-driven surge could pose risks not only to US jobs but also to industries in Europe, Latin America, and Asia.

China’s expansive industrial financing and automated production capabilities provide a significant competitive edge, prompting global policymakers to respond with tariffs and new trade barriers aimed at shielding their industries.

In a bid to counteract China’s export growth—which vastly outpaces that of other trading partners—President Trump’s administration has sought to raise tariffs significantly, aiming for obligations as high as 125% by 2025.

These tariffs on products tied to China’s automation boom are intended to drive up prices in the US, protect local industries, and challenge what officials label as “unfair trade practices” from Beijing, which has retaliated with its own tariffs and escalated trade tensions.