The US economic calendar was light with only the preliminary S&P Global PMI figure being released.

The September 2024 S&P Global PMI data showed mixed performance across sectors.

- The U.S. services PMI came in at 55.4, slightly above the 55.2 expected but down from the previous month's two-year high of 55.7.

- However, the manufacturing PMI fell to 47.0, below the expected 48.5 and down from the previous 47.9, signalling a contraction in the sector.

- The composite PMI was 54.4, slightly down from the previous reading of 54.6.

Prices for goods and services continued to rise at the fastest pace since March, with selling price inflation in both manufacturing and services reaching its highest level in six months and above pre-pandemic averages. In the services sector, cost inflation hit its highest level in a year, mainly due to rising employee wages.. but, Manufacturing input cost growth slows to six-month lowBusiness optimism about future production worsened significantly, with the future production index falling to its lowest level since October 2022. Employment fell for the second straight month in September and has fallen in four of the past six months.

Meanwhile, Fed officials have become more vocal about their views after the central bank began lowering interest rates with a 50 basis point cut last Wednesday.

- Minneapolis Fed President Neel Kashkari defended the recent 50 basis points (bps) rate cut, emphasizing that it was the right decision given the evolution of inflation and the softening labor market. He expects the Fed to end the year at around 4.4% and to fall to 3.4% by the end of 2025, which is in line with the median projections of Fed policymakers. Kashkari cautioned that while he believes the de-inflation process is well underway, it is too early to declare victory over inflation. Fed policy remains tight, but the exact extent of the tightening is unclear. Future rate decisions will be data-dependent, especially as signs are mixed for the economy, with resilient consumer spending but no clear signs of an imminent recession or an inflation spike. Kashkari also expects the Fed to take modest steps in the future and emphasized the need to keep the labor market strong. Kashkari acknowledged uncertainty about the neutral level of interest rates, but emphasized that the labor market is not a reliable predictor of inflation. Kashkari also envisions an additional 50 basis points of easing in 2024.

- Fed President Austin Goolsby suggested that interest rates will likely see “many more rate cuts” over the next year, as interest rates need to be cut substantially. Goolsby is pleased with the recent 50 basis point rate cut, which he sees as a signal that the Fed is focusing on employment risks in addition to inflation. Goolsby noted that inflation is well below its peak and the labor market is at full employment, suggesting that keeping interest rates at their decade-high levels is not consistent with maintaining economic stability. To achieve a soft landing, the Fed needs to avoid being on the back foot. Goolsby emphasized that inflation fell last year but did not induce a recession, and that businesses are not overly concerned about inflation, but rather value stability. He is also keeping a close eye on vacancy rates in office buildings, making sure banks are well prepared for potential losses in commercial real estate. Goolsby's dovish stance emphasizes that while inflation is falling, Fed policy has been trending tighter until the recent rate cuts. He believes that under current circumstances, the Fed could potentially cut rates several times over the next year to bring rates closer to neutral.

- Atlanta Fed President Raphael Bostic supported the recent 50 basis point rate cut as a compromise between inflation uncertainty and growing risks to the labor market. He believes the economy is normalizing faster than expected and policy should be adjusted accordingly. Recent data shows the U.S. economy is on a sustainable path to price stability. However, Bostic stressed that the half-point cut does not signal a set pattern for future rate cuts. He noted that risks to the labor market are growing and more broad-based weakness is likely than a year ago, but the labor market is not yet weak. Price growth has become concentrated in housing, and companies are cautious about hiring but are not considering layoffs. He also said that while there is a debate about the neutral interest rate, it is not very important because interest rates are currently so high. Bostic sees inflation indicators trending favorably as companies are losing pricing power. The Fed is currently facing two balanced risks: inflation and a softening labor market.

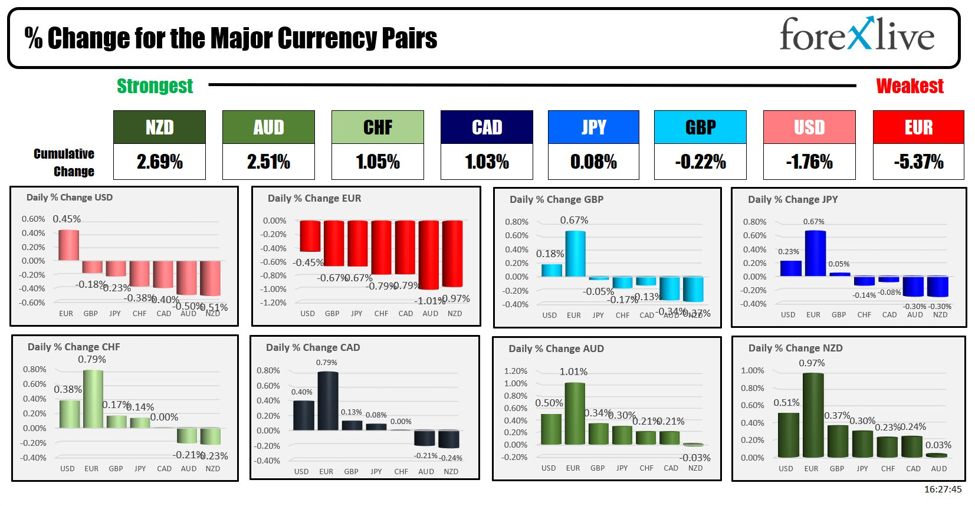

As the day draws to a close, the NZD is finishing the day the strongest of the major currencies. The EUR is the weakest. The USD is mostly down but up against the EUR (0.45%). The USD is down -0.51% against the NZD and -0.50% against the AUD.

US stocks were little changed today, with some gains, with the Dow and S&P both closing at all-time highs. The Nasdaq was up, but only by 0.14%.

US yields are rising. The 10-year yield is 14 basis points above last week's low (Monday before the Fed cut rates by 50 basis points). The 2-year yield is just 4 basis points above last week's low.

Oil is down -$0.36 despite rising geopolitical tensions in the Middle East between Israel and Beirut, with Iran also expressing its displeasure.

Gold rose $6.25 to a new record level.