Rising Health Care Costs: A Growing Concern

Health care costs are increasingly on the minds of many. It appears that lawmakers are keen to find ways to make healthcare more affordable, especially regarding hospitals. Hospital spending is significant—it encompasses both the prices charged for services and the level of care provided. These two factors are crucial as they influence overall affordability and spending patterns. Private insurers generally pay more than Medicare for hospital services; previous studies suggest these payments can be nearly double Medicare rates, with regional and hospital differences adding to the complexity. Such rising costs put additional strain on household budgets through higher insurance premiums and cost-sharing, not to mention the squeeze on wages for those with employer-sponsored insurance.

There’s been an ongoing debate about various policies intended to limit hospital pricing at both national and state levels. These policies aim to enhance competition and counteract the trend of provider consolidation in the market. A growing body of evidence indicates that consolidating hospitals leads to higher prices, yet it remains uncertain how this impacts the quality of care. Some strategies directly target price restraints, such as imposing caps on what providers can charge. Recently, Indiana has enacted legislation that sets limits on prices for nonprofit hospitals and private insurance in the state. Furthermore, in Oregon, caps have been put in place for state employee plans, which can reach 200% of traditional Medicare rates starting in 2019.

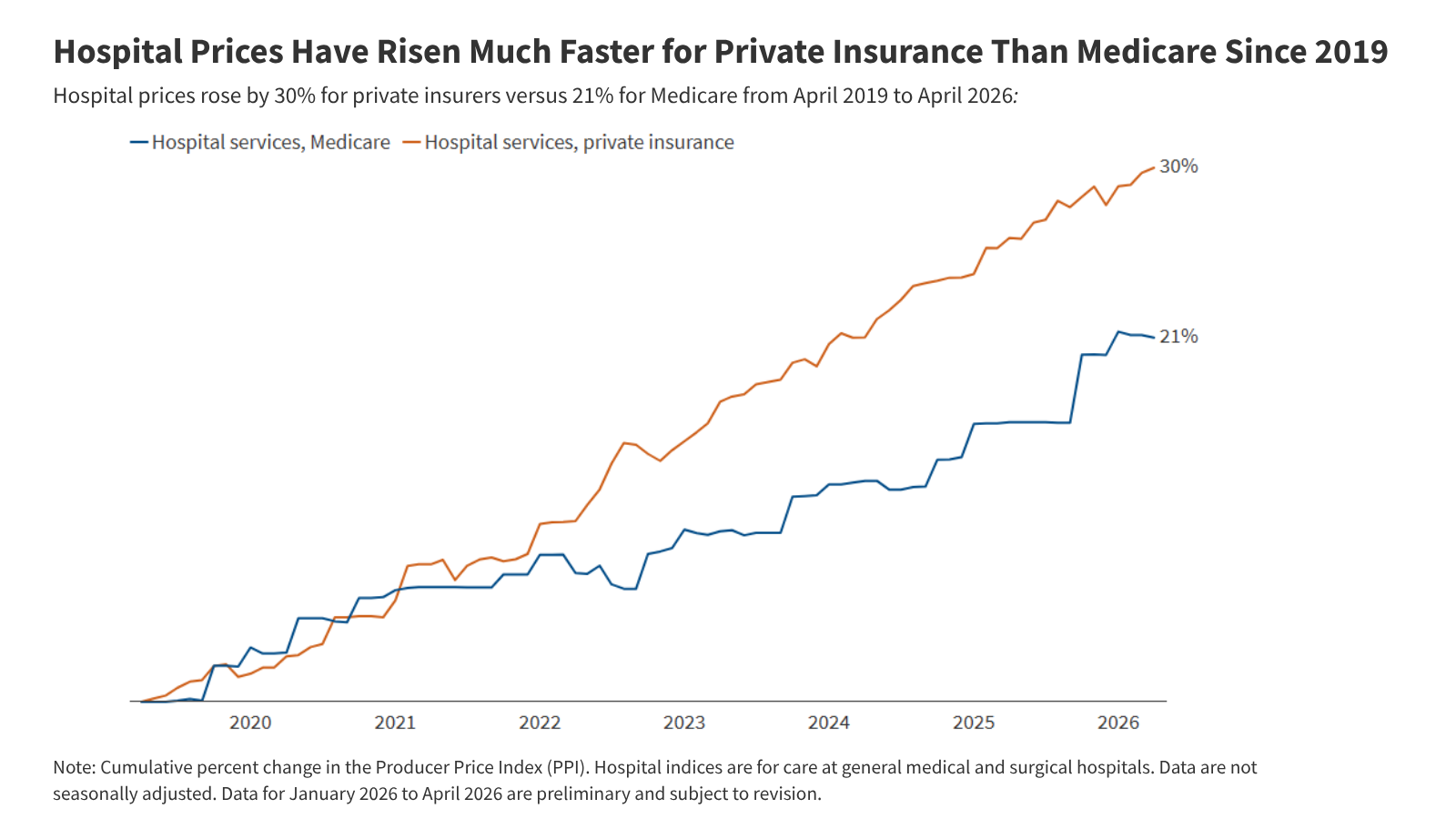

To guide discussions about hospital pricing and potential regulations, a recent brief utilized data from the Bureau of Labor Statistics. It compares the growth rates of prices paid by private insurers for hospital care and Medicare payment rates from April 2019 to April 2026. This analysis was originally started in 2019 to better understand pricing trends during the pandemic.

Price Comparisons: Private Insurance vs. Medicare

Since April 2019, the cost of hospital care under private insurance has jumped by 30% compared to a 21% increase for Medicare during the same period. This means that over these seven years, private insurance costs have grown 47% faster than those covered by Medicare. Initially, from April 2019 to April 2020, private insurance prices rose at a pace similar to Medicare, but starting in April 2020, they began to outpace Medicare costs annually, tapering off somewhat between April 2025 and 2026. These trends echo findings from earlier research suggesting that private insurance rates tend to rise quicker than Medicare’s over time.

Prices for inpatient care under private insurance are shaped by negotiations between hospitals and insurers. Over time, the increases in private insurance rates may reflect various factors, including the rising costs of care provision and the bargaining leverage hospitals have against insurers. The hospital sector is increasingly becoming more consolidated, with a few health systems dominating the majority of inpatient care markets in several metropolitan areas, leading to elevated prices. Rising labor and supply costs during the pandemic have likely compelled hospitals to negotiate higher rates, especially in the context of broader economic inflation, which peaked in mid-2021.

However, contracts between hospitals and insurers are typically renegotiated only periodically, meaning that the full impact of these rising costs may take time to translate into higher prices. On the other hand, traditional Medicare prices are adjusted annually by the Centers for Medicare and Medicaid Services based on specific formulas and regulations. These Medicare adjustments consider projections of input costs, influenced by overall inflation trends. Interestingly, there is evidence that rates for Medicare Advantage plans generally align closely with those for traditional Medicare. Any price increases for Medicare Advantage might reflect similar changes in traditional Medicare rates.

One reason Medicare’s price growth has been relatively slow could be due to an underestimation of inflation when future rates were set. For instance, 2022 saw inflation rates that were unexpectedly high compared to earlier projections for hospitalization costs. Additional factors that might have stifled Medicare price increases include productivity adjustments enacted through the Affordable Care Act, which aim to encourage efficiency among hospitals in patient care. Remarkably, certain automatic payment reductions set under budget rules were paused during the early pandemic and have since been reintroduced, potentially affecting Medicare’s price trends.

Methodology Overview

This analysis relied on the Producer Price Index (PPI) to evaluate hospital pricing trends and general inflation over the timeframe from April 2019 through April 2026. The PPI focuses on prices from the viewpoint of producers—hospitals, in this instance. It has been deemed more useful than the Consumer Price Index (CPI) for analyzing hospital price increases categorized by payer, such as private insurance versus Medicare. The private insurance PPI does not incorporate private Medicaid and Medicare plans, while the Medicare index encompasses both traditional Medicare and Medicare Advantage schemes, which are projected to represent a sizable portion of the Medicare population by 2025.

Interestingly, the overall growth rate for hospital prices, as indicated by the PPI, fell short compared to CPI growth for hospitals during this period. This discrepancy can be attributed to both conceptual differences and the methodologies employed. For example, the CPI gauges prices from the consumer’s perspective. Most of the price increases captured by Medicare’s PPI occur primarily in October and January—likely correlating with the schedule of Medicare’s updates for inpatient and outpatient reimbursements.

Currently, attention is focused on the CMS’s anticipated 2026 IPPS rules. The CMS has noted that its long-term forecasts for hospital market basket approximations generally align well with actual inflation trends. Various adjustments for forecast inaccuracies are made; however, these adjustments might not apply uniformly across all payment structures. The nuances of these pricing mechanisms underline the complexities inherent in hospital pricing today.