Millions of Americans might see sharp increases in health insurance premiums next year as the enhanced premium tax credits from the Affordable Care Act (ACA) are set to end.

Why Is It Important

The expanded subsidies that make health insurance more affordable for individuals across various income levels are expiring at the year’s end, which could lead to significant premium hikes unless Congress steps in.

The ACA Marketplace, launched in 2010, offers health insurance to those who don’t qualify for Medicaid and lack employer-sponsored coverage. During 2020, in response to the COVID-19 pandemic, Congress introduced improved premium tax credits to help reduce costs. These subsidies have drastically lowered monthly premiums, with some low-income individuals even facing premiums as low as $0.

If these subsidies lapse, many enrollees could see their premiums more than double next year, potentially pushing around 2 million additional people into the ranks of the uninsured, according to projections from the Congressional Budget Office.

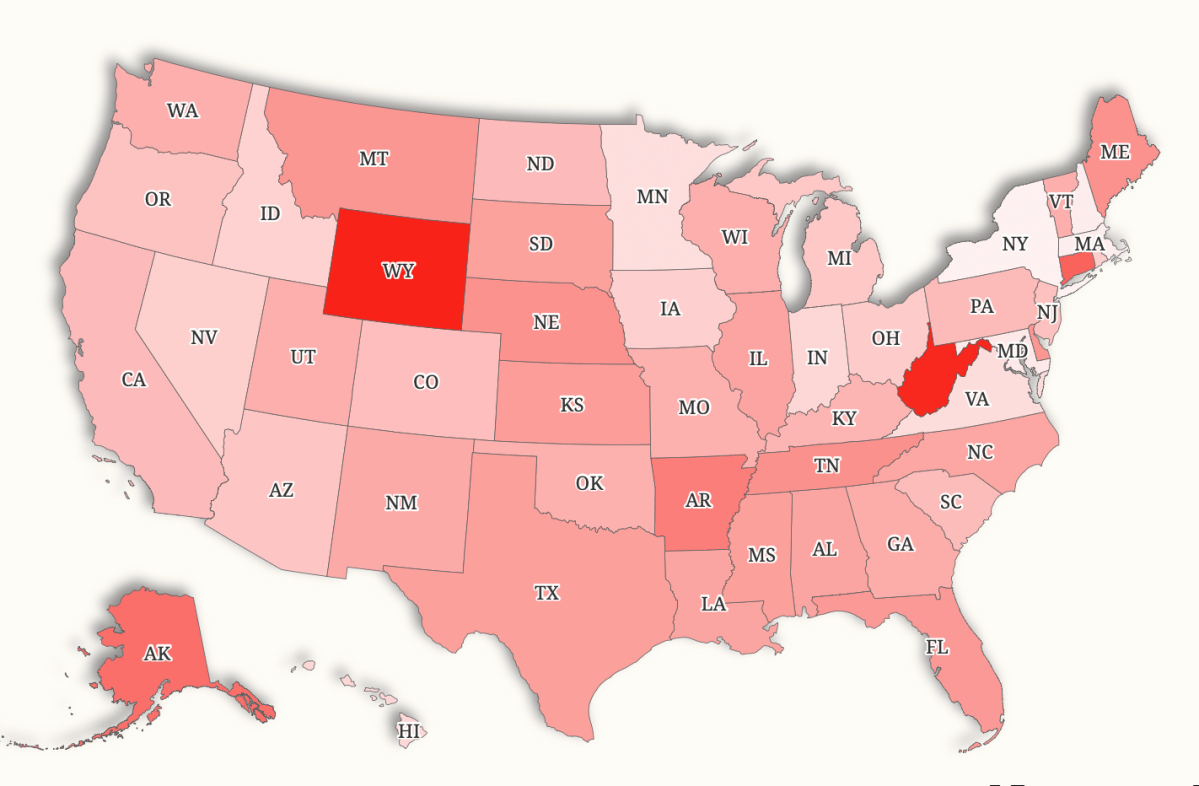

States Facing Highest Increases

Analysis from KFF Health suggests that middle-income seniors will feel the most financial strain, particularly those just above the previous subsidy eligibility thresholds. The current enhanced credit is particularly beneficial for those earning about 401 percent of the federal poverty level, which translates to roughly $62,757 for individuals in the continental U.S. (with higher limits in Alaska and Hawaii).

For a 60-year-old at that income level, the end of the enhanced credit would likely cause the average annual premium for benchmark silver plans in 46 states and Washington, D.C., to at least double. In 19 of those states, premiums could triple or more, making health insurance take up over a quarter of their yearly income.

The biggest jumps in premiums are expected in:

- Wyoming: +$22,452 per year

- West Virginia: +$22,006

- Alaska: +$19,636

Professor Stacey B. Lee from Johns Hopkins University remarked that limited competition, aging populations, high provider prices, and geographic challenges drive up healthcare costs in these states. For some markets, the total cost of premiums before subsidies can exceed $30,000 a year for a 60-year-old. These credit enhancements are crucial; without them, many middle-income residents would struggle to afford coverage.

States with the Lowest Growth Rate

Even the smallest increases remain notable.

- New York: +$4,469

- Massachusetts: +$4,728

- New Hampshire: +$4,877

Lee noted that states like New York, Massachusetts, and New Hampshire adopted ACA with well-established regulations that maintained their market stability, such as community ratings and guaranteed issuance. These stronger foundations allowed for deeper risk pools and more predictable pricing, making the reduced costs manageable even before federal funding arrived.

As income rises, the number of states where premiums double decreases. For example, at around 501 percent of poverty (about $78,407 for individuals in most states), premiums would double for a 60-year-old in 37 states, but this drops to 19 states at 601 percent. In a few states, it would take an income of 701 percent for the same effect. In general, premium increases for 40-year-olds are described as less steep across all income brackets.

What Happens Next

President Donald Trump stated that he does not intend to extend the expiring ACA subsidies, which would result in significant premium increases for enrollees next year.

“I don’t want to do that,” he told reporters during a flight to Florida when asked about continuing the funding. He also pointed out that the Affordable Care Act is such a mess that extensions might be necessary for some further action.

The Trump administration is reportedly working to mitigate the impending premium increases as the expiration of ACA subsidies approaches.