Common Investment Mistakes and Alternatives for Retirement

Many investors unknowingly make significant mistakes that can jeopardize their financial security. One common misstep is relying too heavily on generalized “rules of thumb.” While they may provide a basic framework, these guidelines are often too broad and can be misleading when applied to individual situations.

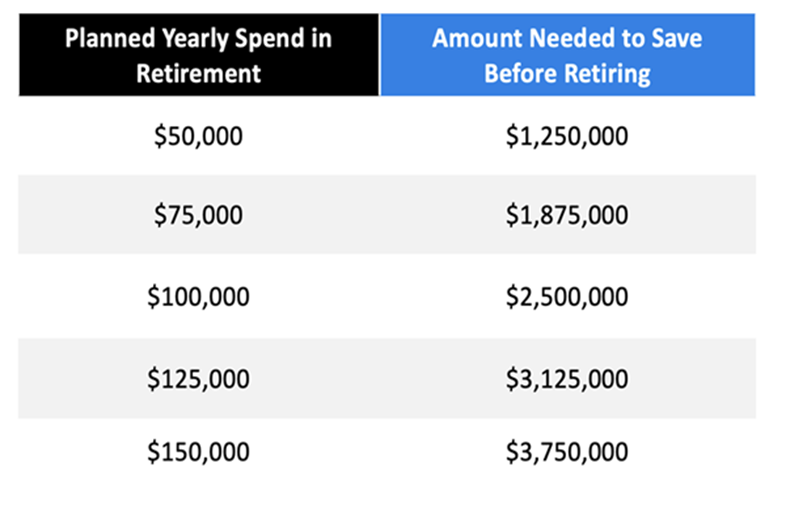

Take, for example, the “Rule of 25.” It suggests that individuals should save 25 times their expected annual spending in retirement. Sounds straightforward, right? But the implications can be daunting. If we look at the typical expenses retirees face—without even factoring in inflation—it becomes clear that preparing for retirement under this rule alone is a tall order.

Let’s consider a hypothetical investor making $100,000 annually and managing to save 20% for retirement, which is quite ambitious compared to most. Assuming an average return of 8.5% from stocks—a rate based on historical performance—it would take over 29 years for this individual to feel ready for retirement.

This may seem like a long time for younger folks, but for those approaching retirement, it might feel extremely rushed. Yet, this anxiety stems from a flawed understanding, especially since the rule has been called into question by its very creator. William Bengen, who established the “safe withdrawal rate of 4%” in 1994, argued that to avoid risking financial instability late in life, one should indeed save up to 25 times their retirement withdrawals.

But then Bengen reassessed this guideline in 2022, updating his withdrawal rate to 4.7% based on new data. So, we might now be looking at something closer to a rule of 21.27 times in savings. It’s a tad comforting, I suppose, but it still carries a lot of assumptions that may not hold for everyone.

Fortunately, there are more favorable options available.

Investing in Closed-End Funds (CEFs)

Certain closed-end funds (CEFs) are specifically designed to turn the typical long-term stock market returns of about 8.5% into income that retirees can live on. For instance, the Liberty All-Star Equity Fund (USA) holds a variety of strong stocks including companies like Microsoft, Visa, and Amazon. Interestingly, this fund currently provides a yield of 10.6%.

This means that with just under $944,000 saved, an investor could potentially replace the lengthy 29-year saving span mandated by the “Rule of 25.” That’s significantly quicker for someone making the same $100,000 salary and saving a similar percentage.

Of course, critics of CEFs often caution against their perceived unsustainable high dividends, and it’s true that the dividends can fluctuate in line with the fund’s net asset value. But let’s look back in time. Over its 39-year history, the USA fund has averaged dividends of approximately 82.4 cents per share annually. That translates to around 11.6% of its initial stock price from 1987, and its structure allows for flexibility in trading during varying market conditions.

The recent downturn in market prices might raise some eyebrows. But USA has historically provided enough passive income to enable retirees to navigate economic downturns like the dot-com crash and even the Great Recession.

The crucial takeaway here is evident when examining what could have transpired if investors had reinvested their dividends back into the fund, resulting in an astonishing 1,840% return over several decades. This comes down to choosing whether to take profits as cash or funneling them back into investments.

Finding Income with More CEFs

I think it’s safe to say that many would prefer not to sell shares just to cover everyday expenses, as that could diminish both income and profits. This is why CEFs, like the USA fund, are appealing. They often come with yields of 9% or higher, ensuring dividends can cover bills regardless of market fluctuations.

The top CEFs for 2026 are strategic picks designed to provide solid income while holding quality stocks, bonds, and real estate investment trusts. Collectively, these options yield a generous 9.2%, making them attractive as the new year approaches.

For anyone interested in solid income and growth, there are specialized reports available detailing these picks, including their names and ticker symbols.